Small-cap value has been one of the loudest asset classes in the market over the past year, and the tax bill on that ride depends entirely on which account holds it. Avantis U.S. Small Cap Value ETF (NYSEARCA:AVUV) is up 20.5% year to date and 30.7% over the past year, closing at $123.97 on July 13, 2026. Held in a taxable brokerage, every one of those gains is a future tax liability. Held in a Roth IRA, none of it is.

Why AVUV Belongs in a Roth

AVUV is an actively managed small-cap value fund with 775 positions and roughly $29.2 billion in net assets. Three features push it toward the Roth column:

- Factor volatility. Small-cap value swings hard. Sheltering multi-decade appreciation tax-free is the headline case.

- Active turnover. The portfolio includes larger positions such as Viasat, Lear, and Matson alongside micro-cap holdings that each represent under 0.001% of assets. Frequent rebalancing means capital gains distributions are possible in a taxable wrapper.

- Non-qualified dividends. A meaningful share of AVUV’s distributions is taxed at ordinary income rates rather than the preferred 15% or 20% qualified dividend rate, which magnifies the tax drag in a taxable account versus a Roth.

The Tax Delta: Roth vs. Taxable

AVUV pays quarterly distributions. The trailing 12-month payout is $1.5612 per share, and the annualized forward estimate is $1.7716 per share based on the $0.4429 dividend paid June 11, 2026. That is roughly a 1.4% forward distribution rate at current prices, with a portion treated as ordinary income.

For a $250,000 position, using the forward rate and treating distributions as ordinary income at the 24% bracket (single filers with taxable income above $105,700 in 2026):

| Scenario | Gross Distribution | Tax | Net Income |

|---|---|---|---|

| Taxable brokerage | $3,500 | $840 | $2,660 |

| Roth IRA | $3,500 | $0 | $3,500 |

The dividend delta is roughly $840 annually. Reinvested at the same forward yield, that compounds to roughly $9,000 over 10 years, before accounting for price appreciation.

The Bracket Multiplier

The same $250,000 AVUV position, same distribution stream, at each major 2026 federal bracket:

| Bracket | Annual Tax in Taxable | Annual Roth Advantage |

|---|---|---|

| 22% | $770 | $770 |

| 24% | $840 | $840 |

| 32% | $1,120 | $1,120 |

| 37% | $1,295 | $1,295 |

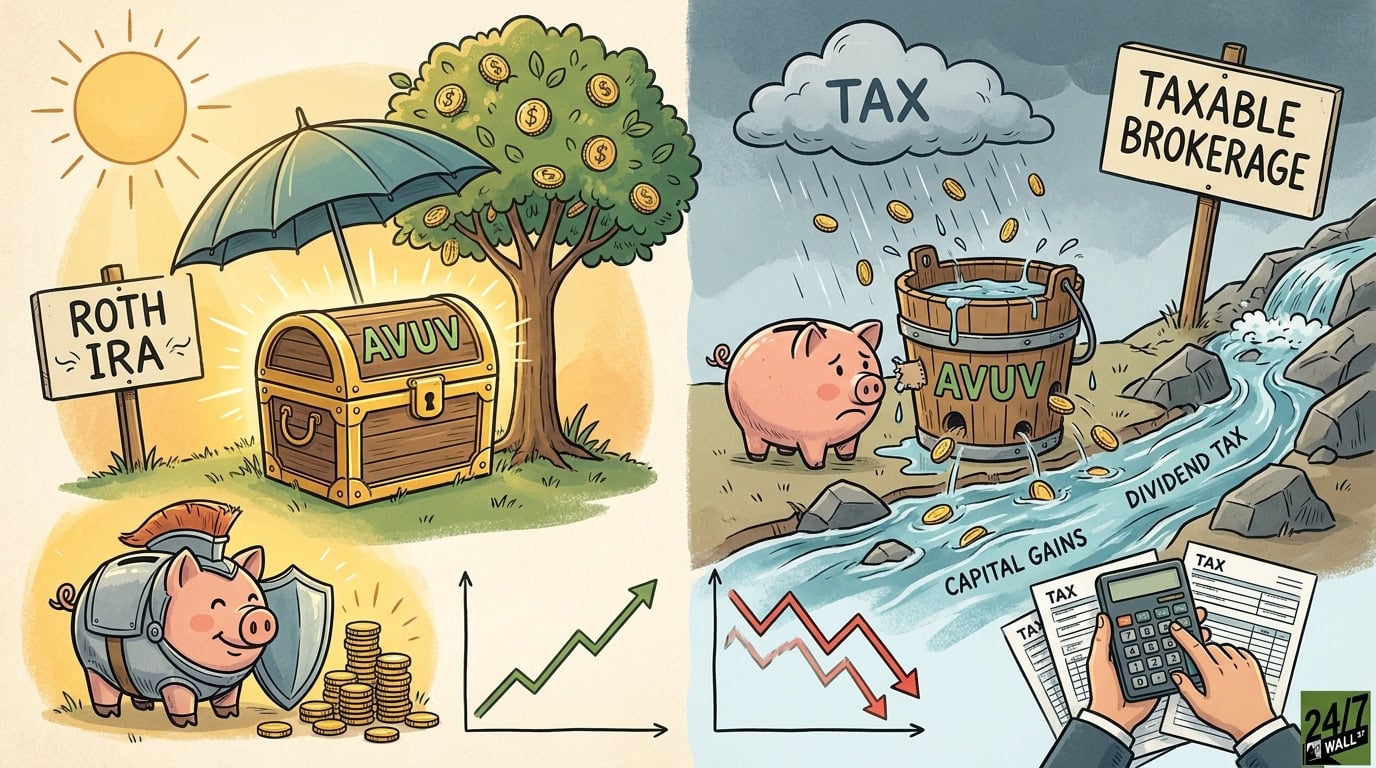

The Insight Most Readers Miss: Tax-Free Rebalancing

The dividend delta is the small story. The larger story is that AVUV’s active managers rebalance across hundreds of holdings inside highly volatile sectors, including energy names such as California Resources and CNX Resources and cyclicals such as Alaska Air and Dana. In a Roth, every trim, every add, every capital gains distribution is tax-free.

Layer on appreciation. Since inception in September 2019, AVUV is up 147.0%, and it has returned 67.3% over the past five years versus 39.3% for the Russell 2000 (IWM) over the same window. That factor premium, if realized inside a taxable account, would eventually produce a large long-term capital gains tax bill upon sale. Inside a Roth, the entire gain is withdrawable tax-free after age 59.5 and the five-year rule.

What to Do

- If AVUV currently sits in a taxable account, review the fund’s most recent 1099-DIV and check the breakdown between qualified and non-qualified income before your next tax filing.

- Calculate the Roth conversion cost for AVUV specifically before assuming that the upfront tax outweighs decades of tax-free small-cap value compounding.

- If you are still contributing, prioritize AVUV inside the Roth wrapper and hold lower-turnover, qualified-dividend holdings in the taxable account.

Contact [email protected] for any questions or corrections.