Best Buy (NYSE:BBY | BBY Price Prediction) and Visa (NYSE:V) have both flashed a golden cross this month. That is, their 50-day moving averages have pushed above their 200-day moving averages. Best Buy posted a beat-and-raise quarter for its electronics business, while Visa delivered mid-teens revenue growth from its global payments network. Two different companies, one shared technical signal, and a fair question about which is the better buy now.

How the Quarter Landed for Each Business

Best Buy’s Q1 FY27 showed enterprise comparable sales up 2.0%, with adjusted EPS of $1.28 on revenue of $8.94 billion. Gaming, computing, and mobile phones drove results, with entertainment comps up 38.1% domestically. CEO Corie Barry highlighted “strong performance in our Best Buy Ads and Marketplace initiatives” as evidence the retailer is building profit streams beyond the box. Jason Bonfig takes over on November 1, 2026.

Visa’s Q1 FY26 results looked cleaner. Net revenue climbed 14.6% to $10.90 billion, processed transactions hit 69.4 billion, and cross-border volume rose 12% on a constant-dollar basis. CEO Ryan McInerney credited “resilient consumer spending and a strong holiday season.” A $708 million interchange litigation provision continues to hit GAAP results, a recurring pattern that investors have learned to weather.

Premium Toll Road Meets Discount Big Box

The businesses differ fundamentally. Visa runs a payments network with a trailing operating margin of 67.3% and profit margins above 51%. Best Buy operates big-box stores, with an operating margin around 4% and net margins under 3%. That gap explains why one trades like a compounder and the other like a cyclical.

| Lens | Best Buy | Visa |

| Forward P/E | 12x | 24x |

| Dividend Yield | 4.5% | 0.8% |

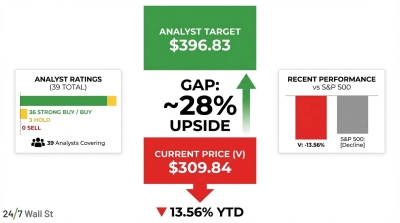

| Analyst Target | $79.15 | $401.47 |

| Key Risk | Tariffs, appliances | Interchange litigation |

Remember that the golden cross is a lagging signal. Best Buy stock has risen 27.6% year to date to $85.37, already trading above the average analyst price target. Visa trades at $355.14, up 1.3% year to date, with room to run to the consensus price target.

The Next Test Is Durability

For Best Buy, watch whether Marketplace and Best Buy Ads can scale enough to offset softness in appliances and the 1.8% decline in domestic consumer electronics comparable sales. FY27 guidance calls for comps between −1.0% and +1.0%, with the CEO transition as a real variable.

For Visa, monitor data processing revenue, which rose 17% last quarter, plus stablecoin and tokenization initiatives that McInerney continues to highlight.

The Verdict

Best Buy offers a 4.5% dividend and a cheap multiple, but it just ran past its mean analyst target and faces a CEO change and tariff exposure. Visa looks like the more durable holding. Investors pay a premium but receive 67% operating margins, a durable network moat, and consistent buybacks against a $21.1 billion authorization. Best Buy may become more attractive to revisit on a pullback closer to its 200-day moving average.

Contact [email protected] for any questions or corrections.