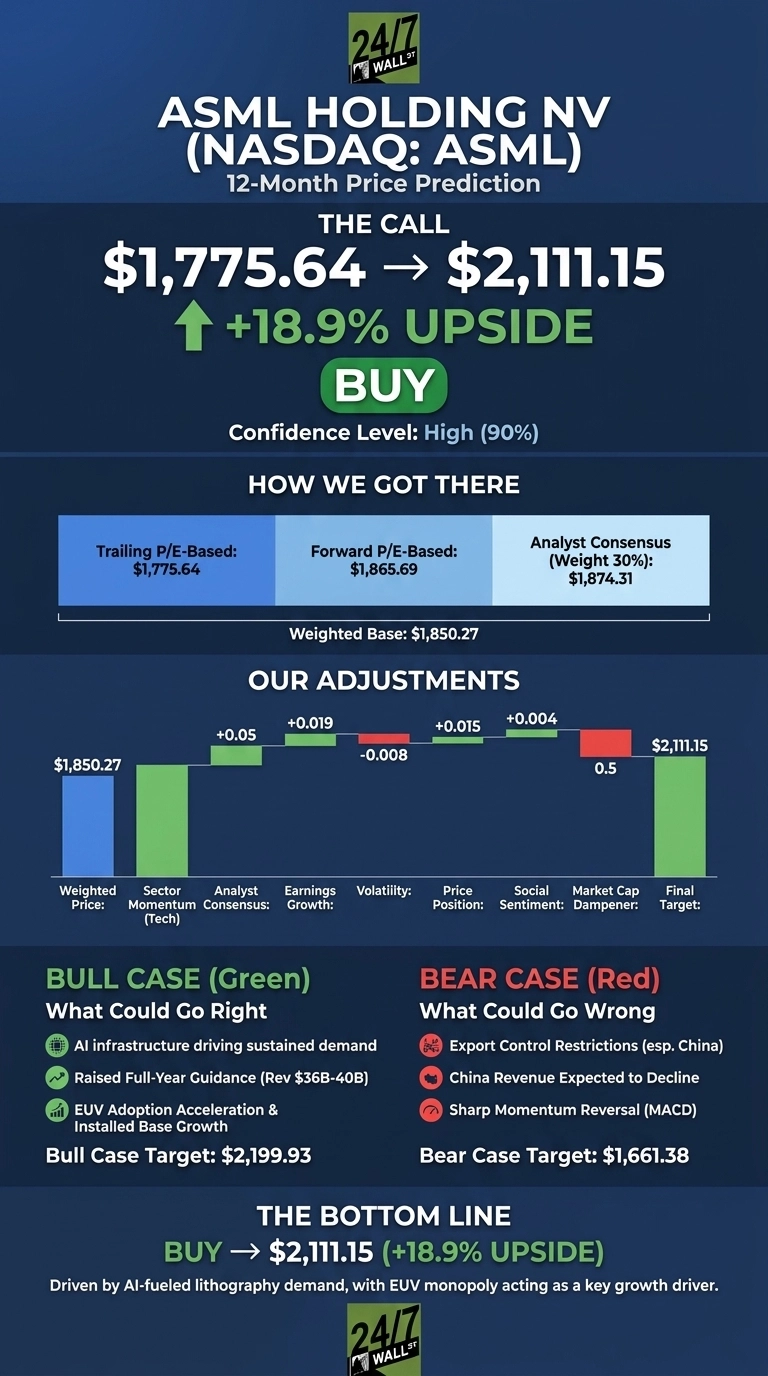

Ahead of ASML’s Q2 2026 earnings report, AI capex is pulling forward lithography demand, and the world’s only supplier of EUV systems is raising guidance again. ASML Holding (NASDAQ:ASML | ASML Price Prediction) trades at $1,775.64 as I write this, up 66.56% year to date and 121.84% over the past year.

Our 24/7 Wall St. price target for ASML is $2,111.15, implying 18.9% upside over the next 12 months. The recommendation is buy with high confidence (90%).

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $1,775.64 |

| 24/7 Wall St. Price Target | $2,111.15 |

| Upside | 18.9% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Guidance Raise on Top of a Guidance Raise

ASML reported Q2 2026 revenue of $10.65B, up 21.3% YoY and above the high end of guidance, with EPS of $8.67 marking the fourth straight beat. Free cash flow jumped 268% YoY to $1.50B, and management raised full-year 2026 revenue guidance to $49.11B to $51.40B.

Full-year 2025 delivered revenue of $37.94B and EPS of $28.70, with a year-end backlog of $45.06B. Over the last four beats, ASML has averaged a -2.55% day-of reaction, so post-earnings volatility is normal.

The Case for $2,200+

The bull case rests on litho intensity. CEO Christophe Fouquet said memory customers are “sold out for 2026 and their supply constraint will last beyond 2026,” while advanced logic customers are ramping 2nm capacity for AI products. ASML plans to add 30% to 2026 low NA EUV capacity for 2027, with another 30% under review for 2028.

Management’s 2030 revenue opportunity spans $51.9B to $70.8B at 56% to 60% gross margins. If order intake momentum from H1 2026 holds and High NA EUV wins broader design-ins, our bull case tags $2,199.93.

What Could Go Wrong

The primary risk is export controls. China revenue is expected to decline significantly in 2026, and management built guidance bandwidth to “accommodate potential outcomes of the export control discussions.”

MACD has rolled over sharply, with the histogram at -20.09 as of July 14 after peaking at +12.23 on June 22. Bulls counter that the pullback is technical noise given the FY guide was just raised and Q4 2025 net orders hit a record $15.28B. The bear case scenario lands at $1,661.38, a 6.44% drawdown.

How ASML Compares to Applied Materials and Lam Research

ASML’s implied forward multiple of roughly 56x looks rich until you see the peer set. Applied Materials (NASDAQ:AMAT) trades at a forward P/E of 38x with 11.4% quarterly revenue growth, offering broader wafer fab equipment exposure but no EUV monopoly.

Lam Research (NASDAQ:LRCX) trades at forward P/E of 42x with 23.8% revenue growth and 40.8% earnings growth, the closest growth match. ASML alone controls EUV, making its multiple reasonable despite appearing aggressive.

| Company | Forward P/E | QoQ Revenue Growth |

|---|---|---|

| ASML | ~56x | 21.3% |

| Applied Materials | 38x | 11.4% |

| Lam Research | 42x | 23.8% |

The Bull Case Rests on EUV

Our 24/7 Wall St. price target of $2,111.15 and buy rating rest on one thing: EUV is the choke point for every leading-edge AI chip on the roadmap. The thesis holds if supply-demand stays tight through 2027 and export-control impact is already priced in. The thesis weakens if China restrictions escalate into deep-UV territory. On balance, the setup favors the bulls.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $2,111 |

| 2027 | $2,380 |

| 2028 | $2,640 |

| 2029 | $2,850 |

| 2030 | $3,036 |

These projections assume ASML executes on its 30% capacity expansion, High NA EUV scales, and export controls stay contained.

Contact [email protected] for any questions or corrections.