Ford (NYSE:F | F Price Prediction) is trading at $14.20, and a $2,500 stake today buys into a legacy automaker in the middle of a transformation: leaner Model e losses, a Ford Pro software business scaling into the hundreds of thousands of subscribers, and management pushing toward an 8% adjusted EBIT margin by 2029. The question for a five-year holder is simple: what could that $2,500 actually be worth by 2031?

The Headline Answer

Under the base case, a $2,500 investment in Ford could grow to about $3,557.75 by 2031, a total return of 42.31%. That maps to a modeled five-year price of $20.20 per share, or an annualized return of 7.31%. The model carries a confidence score of 0.9 (High), reflecting stable analyst coverage, positive year-over-year earnings growth, and Ford’s large-cap profile.

Scenario Table: Where the $2,500 Could Land by 2031

| Scenario | 2031 Share Price | Total Return | Value of $2,500 |

|---|---|---|---|

| Bull | $22.27 | 56.9% | $3,922.50 |

| Base | $20.20 | 42.31% | $3,557.75 |

| Bear | $15.17 | 6.84% | $2,671.00 |

Sell-side analysts sit close to today’s price, with an average target of $14.95 and a rating breakdown of 2 Strong Buys, 3 Buys, 15 Holds, and 1 Sell. Sentiment leans 71% Neutral, so the bull thesis largely rests on Ford executing its own plan rather than on Wall Street chasing the stock higher.

The Why Behind the Target

Three drivers underpin the base-case path to $20.20.

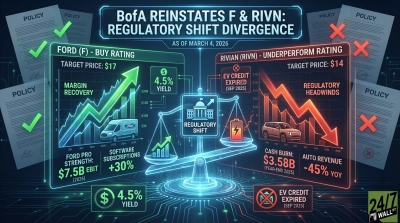

1. Ford Pro is the profit engine. The commercial arm posted $1.69 billion of Q1 2026 EBIT and expanded margins to 11.4%. Paid software subscriptions reached 879,000, up 30% year over year, a high-margin recurring-revenue layer that traditional automakers rarely get credit for. Management guides Ford Pro EBIT of $6.5 billion to $7.5 billion for the year.

2. Earnings power is rebuilding. Ford raised full-year 2026 guidance to adjusted EBIT of $8.5 billion to $10.5 billion and adjusted free cash flow of $5.0 billion to $6.0 billion. Q1 2026 delivered EPS of $0.66 on revenue of $43.25 billion, up 6% year over year. Forward EPS of $1.69 against a stock near $14 translates to an implied P/E of about 9, cheap if the margin plan holds.

3. Cash returns cushion the ride. Ford pays a $0.15 quarterly dividend and has issued two elevated payments in the past two years ($0.33 in February 2024 and $0.30 in February 2025). A dividend yield near 5% compounds meaningfully over five years, especially if reinvested. Ford also repurchased $311 million of stock in Q1 2026. Readers looking at income-focused strategies may find our research on building a portfolio you never touch the principal on useful context for how a 5%-yielding cyclical fits alongside more defensive payers.

What Could Sink the Projection

The bear case at $15.17 assumes execution slips. The biggest overhangs are concrete and near-term. Ford flagged roughly $2.0 billion in commodity headwinds (led by aluminum) and about $1.0 billion of tariff impact outside the one-time IEEPA benefit. The Model e segment is still bleeding, with a Q1 2026 loss of $777 million and full-year losses guided at $4.0 billion to $4.5 billion. FY2025 also carried a GAAP net loss of $8.16 billion after $10.7 billion of Model e impairments. Volatility is real too, with a beta of 1.83, meaning any recession or credit tightening would hit Ford harder than the market.

The Bottom Line

A $2,500 stake in Ford maps to a five-year range of roughly $2,671 in the bear case, $3,557.75 in the base case, and $3,922.50 in the bull case, before counting dividends reinvested along the way. The math is only as good as Ford’s execution on Pro software, Model e loss reduction, and the 8% EBIT margin target. This is a projection, not investment advice, and analyst targets are not guarantees. But for investors weighing a cyclical name with a real dividend and a credible transformation plan, the risk-reward through 2031 skews constructive rather than punitive.

Contact [email protected] for any questions or corrections.