In the world of Reddit finance, the question “Can I retire next year?” seems to pop up all the time. However, one Reddit post highlighted an unusual part of retirement: what do you do afterward?

The couple posting initially brought a solid financial foundation to the table, with over $2.7 million in their portfolio when they first shared their dilemma. Given the massive market run-up that has driven the S&P 500 near the 7,400 mark, an adjusted “where are they now” tracking projection suggests their nest egg could realistically sit closer to $3.1 million to $3.3 million. This surge fundamentally re-baselines their safe withdrawal rate (SWR), dropping their projected lifestyle math into a highly sustainable sub-3.5% range.

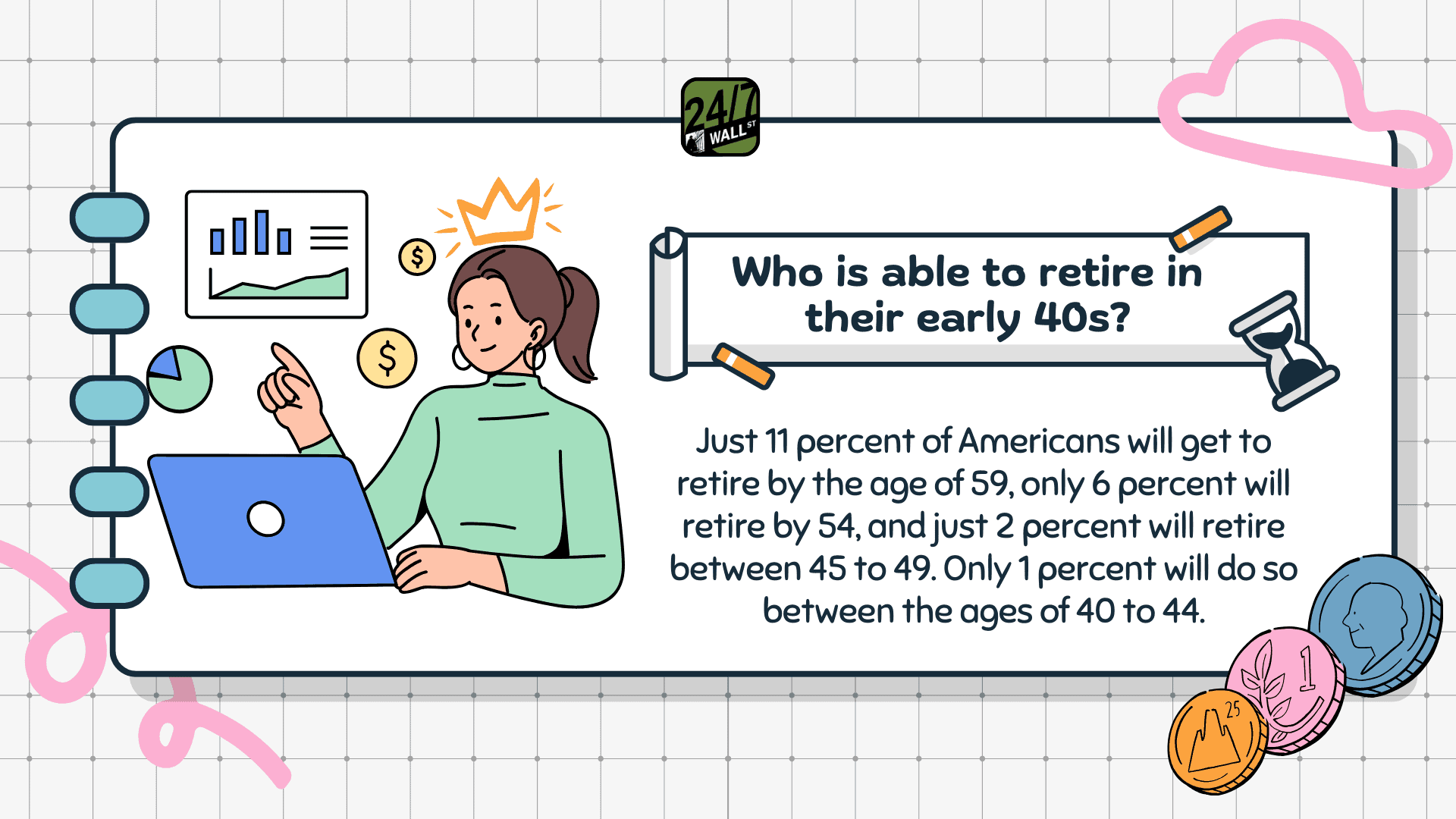

The couple consists of a 42-year-old husband and a 40-year-old wife. They live in a high-cost-of-living area and have significant assets, including a home valued at $1.3 million and a mortgage under 3%. Their current expenses total about $120,000 annually, supported by a high household income that fluctuates between $350,000 and $450,000.

While their math works out to retire, they’re working out what life would look like afterward – a problem that’s very common among retirees.

Retiring is just as mental as it is financial. Below, we look at how to navigate the complex world of after retirement using current financial frameworks. Remember, this is just an educational analysis and does not constitute formal tax or investment advice.

What Type of Life After Work Do You Want?

The key to retiring confidently lies partially in the finances, but it also relies heavily on the mental and emotional aspects of retirement:

1. Motivation and Purpose

Many people take their purpose from their jobs. The poster expresses a desire to retire and focus on health and family. After years in a high-stress job, he recognizes the importance of personal fulfillment over accumulating additional wealth.

On the other hand, his wife enjoys her job and plans to work until she can secure a pension. This difference in motivation can lead to tension, especially if the wife feels annoyed by her husband’s early retirement. There is a clear mismatch of timeline goals here that requires open communication.

2. Finances & Contemporary Market Realities

Part of retiring early is accounting for shifting market cycles. With a split of pretax and post-tax environments, this poster has a solid financial cushion. However, the husband is concerned about Sequence of Returns Risk (SRR) and whether their lifestyle can be sustained long-term if a market correction occurs. His primary retirement income from the portfolio will drop down to roughly $85,000 per year while his wife continues to cover the remainder of their expenses.

Evaluating this risk requires looking at how current capital alignment stacks up against today’s macroeconomic landscape:

| Strategy | Pros | Cons | Current Macro Context |

|---|---|---|---|

| Maintain High Equity Allocation | Maximizes long-term growth; outpaces core inflation. | Highly vulnerable to a sudden late-stage market reset or correction. | S&P 500 valuations remain historically elevated with forward P/E ratios averaging near 22x. |

| Build a Cash / Short-Term Bond Tent | Mitigates Sequence of Returns Risk completely for the first 3–5 years. | Incurs opportunity cost if broader equity markets continue to climb. | The Federal Funds target range sits at 3.5%–3.75%, keeping short-term yields steady but lower than historic peaks. |

| Aggressively Pay Off the 3% Mortgage | Lowers fixed monthly cash flow needs significantly, easing psychological strain. | Sub-optimal mathematical use of capital when liquid assets outpace the low interest rate. | With 30-year fixed mortgage rates averaging near 6.50%, a legacy sub-3% fixed rate represents an irreplaceable financial asset. |

There are many future costs he needs to anticipate, too. For instance, he needs to send his children to college in a decade or so, meaning allocation strategies must remain flexible rather than entirely locked away.

3. Bridging the Pre-Medicare Healthcare Gap

Because the husband explicitly states, “I have had a high stress job all my life and I want to get healthy,” building a viable health insurance bridge to age 65 is non-negotiable. Early retirees face distinct structural hurdles that require proactive management:

- ACA Exchange Navigation: To secure Affordable Care Act premium subsidies, the household must tightly manage its Modified Adjusted Gross Income (MAGI), balancing portfolio withdrawals against strategic Roth conversions.

- Unsubsidized Realities: If household income or capital gains disqualify them from subsidies, a dedicated cash-flow line item of $1,500 to $2,000 per month must be factored into the baseline budget for premium costs.

- Health Savings Accounts (HSAs): Maximizing and deploying existing HSA funds can serve as a powerful, triple-tax-advantaged mechanism to fund out-of-pocket medical care completely separate from regular portfolio withdrawal mechanics.

4. Lifestyle Adjustments: Operationaling the “Retirement Test Drive”

One place where this couple may really benefit is a phased lifestyle adjustment. Instead of a hard, permanent career termination, the couple should look at actionable transitional models. The couple may benefit from the framework of “CoastFIRE,” where assets are left to compound untouched while part-time or flexible roles cover intermediate costs.

To avoid the psychological shock of sudden decompression, a step-by-step blueprint works best:

- The Structured Sabbatical: Executing a firm, predetermined 3-to-6-month complete break allows the husband to decompress, stabilize health metrics, and build an identity separate from a high-stress corporate environment.

- The Fractional Pivot: Transitioning specialized corporate skills into 10–15 hours of remote, fractional consulting per week can comfortably cover the active lifestyle funding gap. This protects the core principal from early drawdowns, allowing compounding to do the heavy lifting in the background.

Creating a Comprehensive Plan

Planning for retirement isn’t just about math. It’s about the mental and relationship aspects of retirement, too. It’s important to create a comprehensive approach to life after work with your spouse and whoever else is affected by your decision. Having honest discussions is how you work out a plan that contributes to everyone’s success and goals.

Working with a qualified financial planner or CPA is highly recommended to properly map out multi-decade income streams, tax bracket optimization, and portfolio preservation strategies.

Editor’s Note: This article has been comprehensively revised to incorporate current macroeconomic data, including updated asset portfolio valuations reflecting the modern S&P 500 performance, prevailing Federal Reserve target interest rates, and average fixed mortgage benchmarks. The updated text features expanded technical commentary on navigating pre-Medicare healthcare infrastructure, establishing Affordable Care Act subsidy income targets, utilizing Health Savings Accounts, and implementing a phased transition strategy utilizing structured sabbaticals and fractional advisory roles.

Contact [email protected] for any questions or corrections.