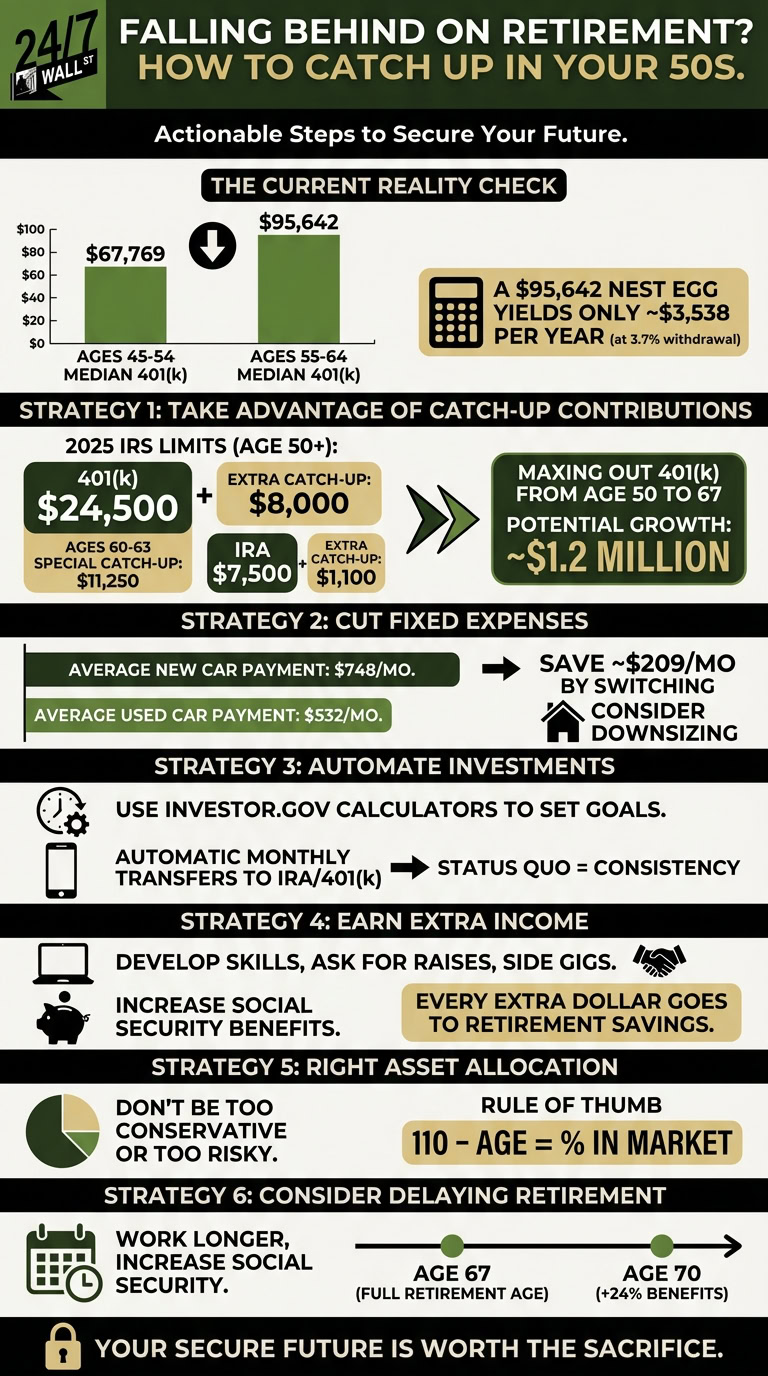

For Americans ages 45 to 54, the median 401(k) balance is just $78,730 according to Vanguard’s How America Saves 2026 Report. This is far less than most people need to be ready to retire. Things don’t get much better for those ages 55 to 64, either, with the median balance rising to just $107,269. A nest egg of only $107,269 would generate roughly $3,969 per year at a safe 3.7% withdrawal rate. By comparison, Northwestern Mutual’s 2026 Planning and Progress Study finds that Americans believe they need $1.46 million to retire comfortably, meaning the typical worker in their late 50s is barely a fraction of the way there.

If you find yourself among the many people in their 50s who are falling short of where you need to be, there are techniques that can help you invest for your future. Here’s what you should do to get back on track.

Take advantage of catch-up contributions

One of the single best ways to get caught up is to take advantage of accounts that provide tax breaks for retirement. Accounts like a 401(k) and IRA allow you to reduce your taxable income based on the amount of contributions you make during the year. For each $1,000 you invest, you can save up to $220 on your taxes if you are in the 22% tax bracket, with larger savings for those in higher brackets.

These accounts have annual contribution limits, but you are allowed to invest more once you reach age 50. For the 2026 tax year, the maximum base 401(k) contribution is $24,500, while the maximum base contribution for traditional and Roth IRA accounts is $7,500. Once you are 50 or over, you become eligible for extra catch-up contributions.

- You can make an additional $8,000 catch-up contribution to your 401(k) after age 50, bringing your total contribution limit to $32,500. If you are 60, 61, 62, or 63, a special “super catch-up” provision allows you to contribute an extra $11,250 instead, for a total of $35,750.

- You can make an extra $1,100 catch-up contribution to your IRA after age 50, bringing your total annual limit to $8,600. This is the first increase to the IRA catch-up amount since 2006, reflecting a new inflation-adjustment rule under SECURE 2.0.

If you can max out these accounts, including catch-up contributions, you will build a secure future far faster than you might expect. Investing $32,500 in a 401(k) from age 50 to age 67 can net you over $1.2 million. Since contribution limits are indexed for inflation and you would be eligible for the larger super catch-up amounts from ages 60 to 63, your final balance could be even higher. An employer match on top of your own contributions accelerates that growth further.

Navigate the Roth catch-up rules for high earners

If you are a high-earning professional trying to make up for lost time, a major regulatory change under SECURE 2.0 affects how your retirement accounts work starting in 2026. Anyone whose prior-year wages from their current employer exceeded $150,000 must direct all age-50-plus catch-up contributions into after-tax Roth accounts rather than traditional pre-tax accounts. If your earnings place you over this threshold, confirm with your HR department that your employer’s plan supports Roth catch-up contributions. If the plan lacks a Roth option, high earners are legally barred from making any catch-up contributions until the employer adds that infrastructure.

Maximize self-employed retirement structures

If you are boosting your late-stage savings through independent consulting, freelancing, or other self-employment, you are not bound by standard corporate employee limits. A Solo 401(k) or a Simplified Employee Pension (SEP) IRA can let you contribute far more aggressively than a typical workplace plan. As a self-employed individual using a Solo 401(k), your combined employee and employer contributions can reach up to $72,000 in 2026, plus an additional $8,000 catch-up contribution if you are 50 or older, for a total of $80,000. Those ages 60 to 63 can push that figure to $83,250 using the super catch-up. A SEP IRA similarly allows employer contributions up to $72,000, though it does not offer a catch-up contribution at any age. Either structure can dramatically accelerate your wealth accumulation compared to a standard workplace plan cap.

Cut fixed expenses

It may seem impossible to invest $32,500 or anything close to that amount. But you can steadily increase your contributions by reducing fixed expenses. Cutting a single large monthly bill is far more sustainable than trying to maintain dozens of small discretionary sacrifices over years.

Take your car payment as one example. According to Experian’s State of the Automotive Finance Market report for Q1 2026, the average monthly payment for a new car is $770 and the average payment for a used car is $531. Choosing a cheaper used vehicle instead of a new one frees up roughly $239 per month. Better yet, buy a modest used car, pay off the loan as quickly as possible, and drive it until it has no value left, so you have no car loan and an extra $531 to $770 per month flowing directly into retirement savings.

Downsizing your home or making other significant one-time lifestyle changes can deliver similar results, freeing up hundreds of dollars each month that you can redirect toward your future.

Leverage health savings accounts as part of your strategy

Late savers should prioritize a specific funding sequence to get the most out of available tax advantages. A critical and often overlooked tool is the Health Savings Account (HSA), which offers a rare triple tax benefit: contributions are tax-deductible, growth is tax-free, and withdrawals are tax-free when used for qualified medical expenses. For 2026, the HSA contribution limit is $4,400 for individuals with self-only coverage and $8,750 for those with family coverage. Individuals aged 55 and older can add a further $1,000 catch-up contribution on top of those limits.

Maxing out an HSA alongside your retirement accounts builds a dedicated pool for healthcare costs in retirement, preserving your primary portfolio for general living expenses. That separation matters because healthcare is one of the largest and most unpredictable expenses retirees face.

Automate your investments

The best way to make sure you hit your goals is to start with a realistic target. The calculators at Investor.gov account for your current savings balance, projected returns, and retirement timeline, giving you a concrete monthly savings number to aim for. Once you know that number, build it into your budget and automate your contributions.

Setting up automatic transfers to an IRA or 401(k) removes the decision from your hands each month. You are far more likely to stick with an investing plan when it runs on autopilot. When you have to manually move money into savings, it becomes easy to rationalize spending it elsewhere and fall off course.

Earn some extra income

Increasing income is one of the most direct ways to get back on track when you have fallen behind on retirement savings. There is an added bonus as well: higher earnings can lift your Social Security benefit, because the benefit calculation is based on your average wages during the 35 years in which you earned the most.

You can increase what you bring in by developing new skills, pursuing overtime, seeking a better-paying position, negotiating raises, or picking up a side gig for even a few hours per month. As you raise your earnings, direct every additional dollar toward your retirement accounts first. Since you are not counting on that extra income to cover routine expenses, you can put all of it to work building a more secure future.

Make sure you have the right asset allocation

When you are behind on savings, your money needs to work as hard as possible. That means finding the right balance between growth and risk. Investing too conservatively means your portfolio may not generate the compound returns you need. Investing too aggressively when retirement is approaching creates the risk of a severe loss at exactly the wrong time.

Working with a financial advisor is the best way to build a personalized allocation plan. If you want a starting point on your own, a common rule of thumb is to subtract your age from 110 and place that percentage of your portfolio in equities. The result gives you a rough guide to whether your current mix is appropriate for your stage of life.

Consider delaying retirement age

Working longer can help in several ways at once: it lets you continue contributing to retirement accounts, gives your existing savings more time to grow, and reduces the number of years your portfolio will need to support you. A longer career also increases your Social Security benefit if those later years rank among your 35 highest-earning years.

Aiming to work until at least age 67, the current full retirement age for Social Security, is a reasonable starting point. If you are significantly behind, a few more years of work can make a substantial difference. Delaying your Social Security claim until age 70 maximizes your monthly benefit, increasing it by as much as 24% compared to claiming at full retirement age. Taking these steps together will require real sacrifice, but each one moves the needle meaningfully toward the secure retirement you deserve.

Editor’s note: This article was updated to reflect the Vanguard How America Saves 2026 Report, which shows revised median 401(k) balances of $78,730 for workers ages 45 to 54 and $107,269 for ages 55 to 64, up from prior figures. Car payment benchmarks were refreshed to Q1 2026 Experian data ($770 for new vehicles, $531 for used). The self-employed retirement section was corrected to clarify that the $72,000 Solo 401(k) limit is a combined employee-plus-employer total, and that SEP IRAs do not offer a catch-up contribution. The HSA section was updated to include the 2026 individual contribution limit of $4,400, and context from Northwestern Mutual’s 2026 Planning and Progress Study was added to the introduction.

Contact [email protected] for any questions or corrections.