When a $7,300 bonus lands in your account, the choice between building stability and chasing dreams reveals whether you’re building wealth or just earning well. For Jimmy from Salt Lake City, that moment arrived in January 2026 with three competing options: fund an emergency account that would “last till about Tuesday of next week,” finally take his wife on the honeymoon promised over a decade ago, or buy into the SpaceX IPO.

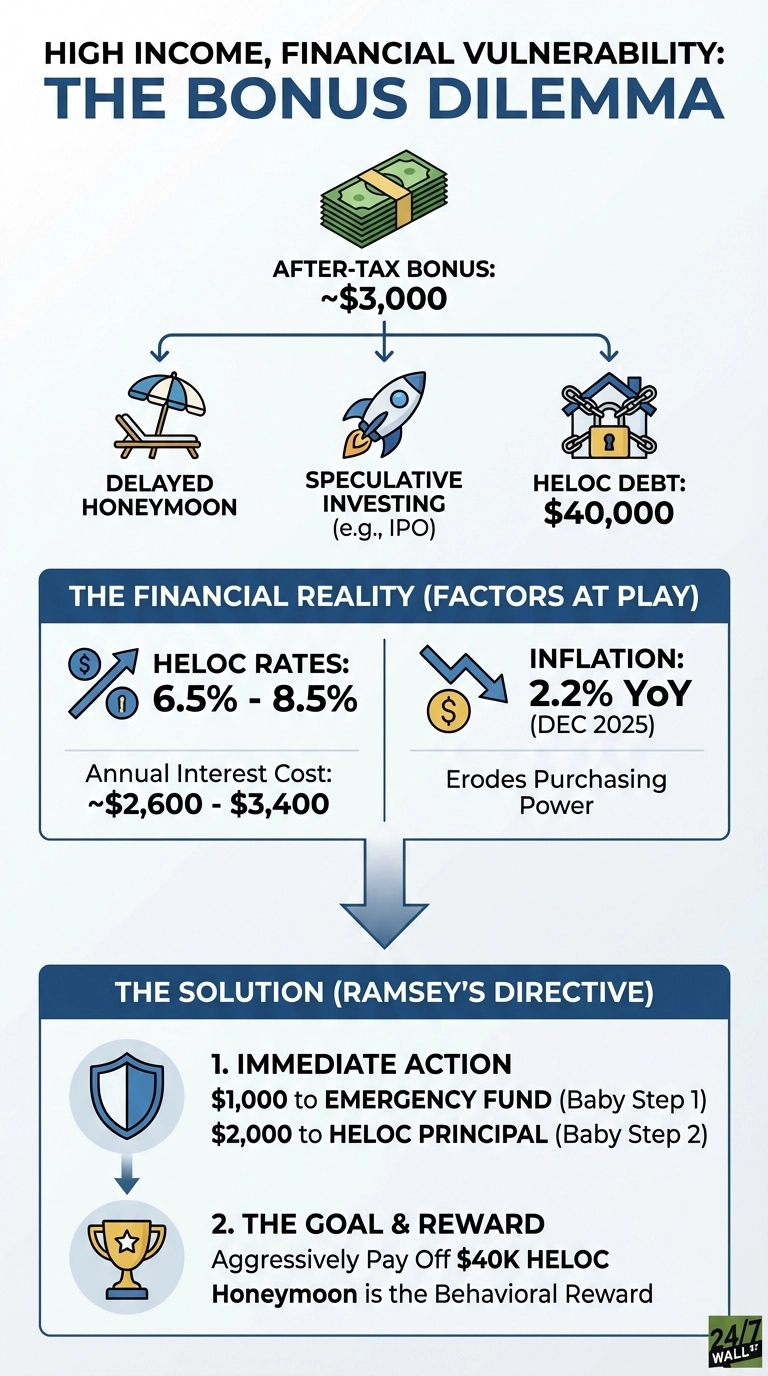

On The Dave Ramsey Show, Jimmy and his wife presented their situation: $180,000 in combined income, a $40,000 HELOC, a $220,000 mortgage, and approximately $3,000 in after-tax bonus money. Ramsey’s directive was immediate: allocate $1,000 to emergency savings and apply the remaining $2,000 to the HELOC. The vacation would wait.

The Financial Reality High Earners Ignore

Jimmy’s scenario illustrates a pattern common among high-income households: substantial earnings masking fundamental financial vulnerability. A Reddit user facing a similar decision with a $50,000 bonus and $50,000 in credit card debt at 25-30% interest debated between debt elimination and emergency fund building, ultimately choosing to pay off $44,000 of debt immediately. The relief was tangible: “Definitely feels like a weight has been lifted off my shoulder.”

With HELOC rates currently at 6.5-8.5% in the current 3.75% Fed Funds Rate environment, Jimmy’s $40,000 balance costs roughly $2,600-3,400 annually in interest alone. That’s money diverted from wealth-building to service debt representing less than half their annual income. In Ramsey’s Baby Steps framework, this debt belongs in Step 2 (debt elimination), not Step 6 (paying off the mortgage early). Without cash reserves, any unexpected expense forces the couple back into debt.

Why the Honeymoon Becomes the Motivator

Ramsey recommended using the delayed honeymoon as motivation to eliminate the entire $40,000 HELOC. At their income level, aggressive focus could clear the balance in roughly 10 months. This transforms a decade of unfulfilled promises into a meaningful financial milestone, where the vacation becomes a reward for behavioral correction rather than another expense layered onto existing debt.

The SpaceX IPO temptation represents the most dangerous option: speculative investing while lacking basic financial foundations. Consumer sentiment stood at 52.9 in December 2025, down 26% from the previous January, reflecting broad economic anxiety. Inflation at 2.2% means their $180,000 income loses approximately $3,960 in purchasing power annually, making emergency fund adequacy critical.

What to Do When the Bonus Arrives

Split the after-tax bonus: $1,000 to emergency savings (Baby Step 1), remainder to highest-interest debt. Calculate how many months of aggressive payments would eliminate the debt entirely, then use a meaningful reward as the finish line. Avoid speculative investments until foundational steps are complete. The behavioral pattern that left a high-income household financially stressed won’t fix itself through earnings alone. Build the foundation first, then enjoy luxuries guilt-free.

This article provides general financial education and is not personalized advice. Your specific situation may require different strategies.

Contact [email protected] for any questions or corrections.