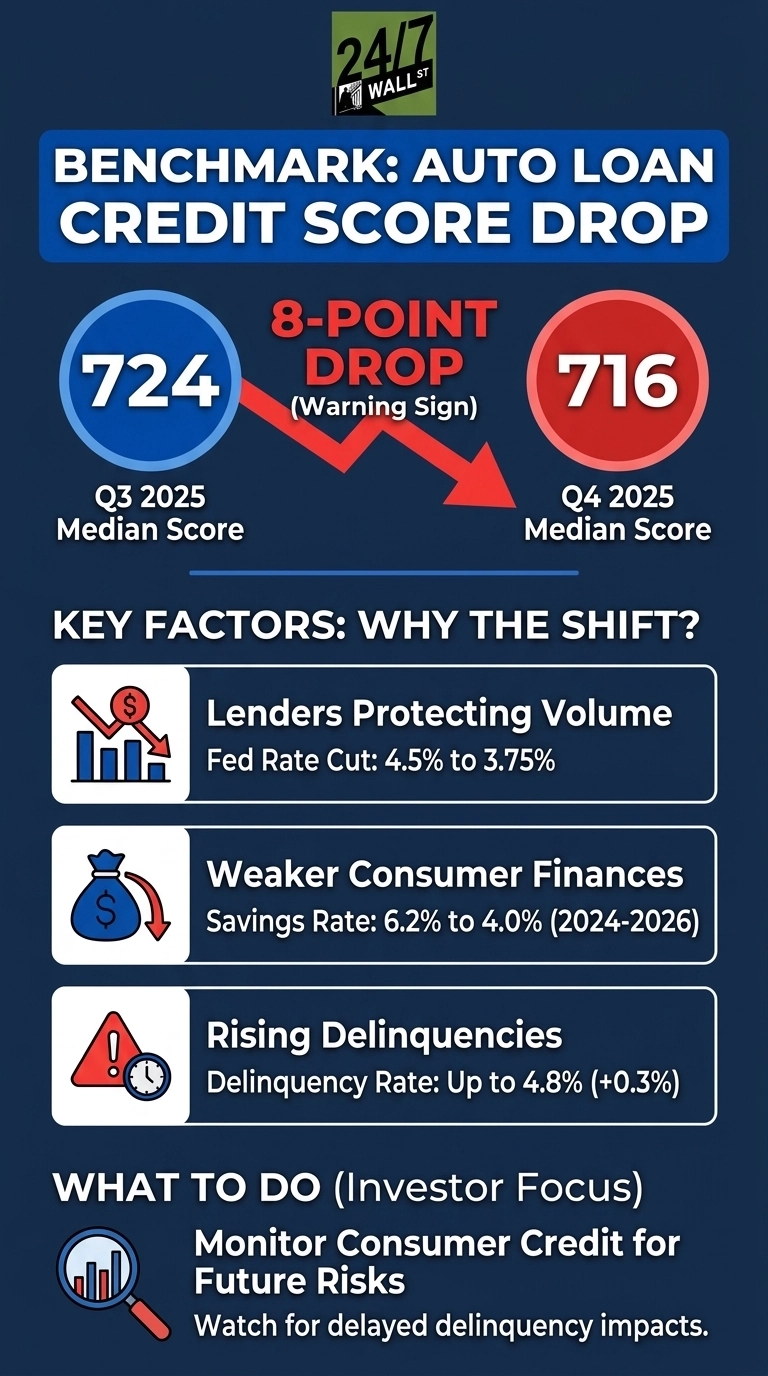

Eight points. That is the distance between where auto loan borrowers stood three months ago and where they stand today, and in the world of consumer credit, eight points is not a rounding error. It is a signal, and the New York Fed’s Q4 2025 Household Debt and Credit report is flashing it in plain sight for anyone paying attention.

This is a reminder that lenders did not get generous, they got desperate for volume and started approving borrowers they would have passed on a quarter ago, and that specific decision has a track record that nobody in consumer finance looks back on fondly.

The Number Behind the Headline

Twelve billion dollars. That is how much auto loan balances grew in a single quarter, pushing the total to $1.66 trillion on the back of $181 billion in fresh originations. Volume like that looks healthy until you realize who is getting approved to generate it. Below a 716 median score, you are talking about borrowers with almost no cushion between a normal month and a missed payment, and missed payments can quickly turn into something much worse.

Mortgage lenders held firm at a median origination score of 775, unchanged from the prior quarter. Auto lenders moved the other way. When two corners of the same credit market diverge that sharply in the same quarter, the corner that loosened is almost always where the damage shows up first.

Why Auto Credit Cracks First

Cars are not optional for most American households, and that is exactly why auto credit breaks before everything else does. The payment gets prioritized right up until the moment it physically cannot be, which means by the time delinquencies start climbing in auto, the financial damage inside those households is already deep. Aggregate delinquency hit 4.8% at the end of December, up 0.3 percentage points from the prior quarter and trending the wrong way across categories.

Rate cuts from 4.5% to 3.75% between September and December 2025 squeezed lenders’ margins so hard that widening the approval box began to look like the only way to protect volume. That is the environment that produces an eight-point drop in median origination scores in a single quarter, and it is the environment the rest of this data sits in.

The Floor Is Getting Slippery

Unemployment is still healthy, and that is precisely what makes this unsettling. Standards are not loosening because people are losing jobs. They are loosening because the financial buffer between a working household and a struggling one has quietly thinned over the past two years, leaving borrowers with less margin for error at exactly the moment lenders are deciding to approve more of them. Consumer sentiment has already priced in the stress that the employment numbers have not yet caught up to, sitting deep in pessimistic territory well below the threshold historically associated with recessionary readings.

Spending has been outrunning income long enough that the savings cushion most households thought they had has essentially disappeared, and the debt keeps piling on top of a foundation that is getting shakier by the quarter.

What the Pattern Is Really Saying

Early signals in consumer credit have a way of looking blindingly obvious in hindsight, and this one is worth taking seriously now rather than later. A 716 median origination score means today’s buyer has meaningfully less margin for error than the buyer who financed a car just three months ago, and that shift is arriving while delinquency is already climbing and sentiment is already sour. Tightening would be the textbook response to that combination. Instead, lenders are easing into it, and that gap between what the data says and what the market is doing is exactly where the next round of problems tends to start.

Contact [email protected] for any questions or corrections.