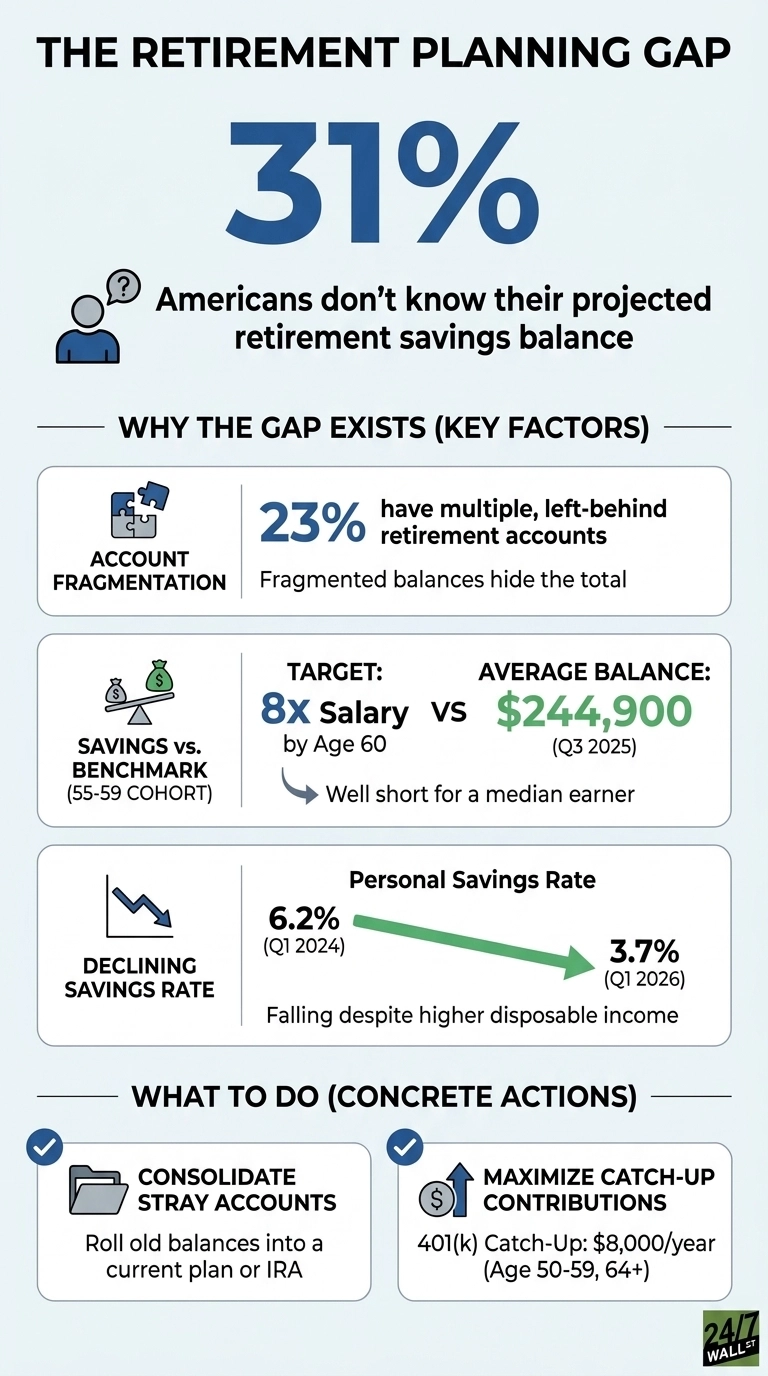

Fidelity’s 2026 retirement study landed with an optimistic surface read, as 74% of Americans say they have a retirement plan in place. The quieter finding sits underneath: 31% of Americans don’t know how much they’ll have saved by the time they retire. Nearly 1-in-3 people with what they describe as a plan cannot answer the most basic question that a plan is supposed to answer.

That gap sits between having an account and having clarity. A 401(k) deduction running quietly in the background is a savings mechanism. A plan is a number, a timeline, and a path between them. Fidelity’s data show that people with an actual plan are more than twice as likely to feel confident about retirement, and 81% of retirees with a plan say they have enough money to last their lifetimes, compared with only 45% of retirees without one. The same career, income, and account balance can produce two different retirements depending on whether the saver knew where they were going.

What “Having a Plan” Actually Requires

Fidelity’s benchmarks give the destination. A worker is supposed to have 1x salary saved by age 30, 3x by 40, 6x by 50, 8x by 60, and 10x by 67. Those multiples assume a 15% savings rate and retirement at 67, with savings replacing 45% of pre-retirement income on top of Social Security. Without those anchors, a balance is just a number on a statement.

Current balances show how far ahead the benchmarks sit. Fidelity’s latest data puts the average Baby Boomer 401(k) balance at $269,100, Gen X at $215,600, Millennials at $82,600, and Gen Z at $18,000. By age band, the 55-59 cohort averaged $244,900 and the 60-64 cohort $246,500, well short of the 8x salary target for a median earner. Averages hide the lower half. The typical balance is materially smaller than the mean.

Account Literacy Is the Hidden Drag

The second piece of the planning gap is account hygiene, with 66% of Americans understanding that IRAs and 401(k)s serve different roles, while roughly a third do not. Separately, 23% of Americans with retirement accounts maintain multiple accounts left behind from past or current jobs, fragmenting balances across recordkeepers, fee schedules, and forgotten allocations. Each stranded 401(k) is a small leak in the compounding engine.

Contribution rules changed for 2026, and the planning-versus-saving distinction shows up here, too. The standard 401(k) employee limit is $24,500, the age 50-59 and 64+ catch-up is $8,000, and the age 60-63 super catch-up is $11,250. IRA limits are $7,500, with a $1,100 catch-up. Savers who know these numbers route money accordingly, those who do not leave room on the table.

Why the Planning Gap Is Widening

Competing-priorities data explains why many savers default to autopilot. Fidelity found the top forces pulling against retirement contributions are rising cost of living (50%), saving for major purchases (44%), and building emergency savings (32%). The macro backdrop is consistent with that pressure. The personal savings rate fell from 6.2% in the first quarter of 2024 to 3.7% in the first quarter of 2026, even as per capita disposable income rose to $68,359. University of Michigan consumer sentiment registered 49.8 in April 2026, down from 61.7 in July 2025.

The Checklist Underneath the Headline

The Fidelity finding points to items that convert an account into a plan:

- Name the number. Pick a target balance at retirement age using the salary-multiple framework (10x by 67 for a maintained lifestyle) to measure progress.

- Consolidate stray accounts. The 23% with multiple legacy 401(k)s can roll over old balances into a current plan or an IRA to simplify allocations and fees.

- Match the contribution to the rule. Workers over 50 can add the $8,000 catch-up, and those age 60-63 can use the $11,250 super catch-up on top of the $24,500 base limit.

- Re-check the plan annually. Inflation, wage changes, and shifting retirement age all move the target. Core PCE rose from 126.121 in June 2025 to 129.63 in April 2026, a reminder that the dollar amount needed at 67 is not static. The 31% who cannot estimate their retirement balance need this annual recalibration most.

Many of the 31% who cannot estimate their retirement balance contribute every pay period. They have not done the second step, which is translating those contributions into a projected outcome. In the Fidelity data, that step correlates with retirees reporting they have enough money to last their lifetime.

Contact [email protected] for any questions or corrections.