Uber Technologies (NYSE:UBER): Did They Overrun 1st Quarter Earnings?

Live Updates

Uber Membership Quietly Hits 30 Million Users

Uber’s membership program now boasts 30 million users, with penetration above 60% in delivery and even higher in some markets. Members spend 3x more than non-members and enjoy benefits like $0 delivery fees and exclusive deals. Dara highlighted this as a core part of Uber’s affordability strategy—and it’s a flywheel most observers overlook. It’s a subscription machine that helps anchor frequency, loyalty, and value perception.

Suburban commute trip racking up profits for Uber

Prashanth Mahendra-Rajah revealed that sparser markets now account for 20% of mobility trips and are growing faster than core urban areas. While frequency in suburbs may be lower due to higher car ownership, pricing and margin mix are actually better, especially with services like Uber Reserve gaining traction. This expansion into lower-density geographies isn’t just white space—it’s margin-accretive and helping to prolong Uber’s topline growth arc.

Uber ads and scale keeping rider cost down

Uber’s delivery segment posted 70bps of margin expansion YoY, reaching 3.7% of gross bookings. The driver? Not pricing hikes, but advertising leverage and scale efficiencies. The company now sees grocery and retail (which hit breakeven in Q4) turning contribution positive in Q1. With 9% incremental margins on delivery in Q1, Uber is quietly building a structurally profitable delivery business—something few peers have achieved.

Year-over-year view

| Metric | Previous | Current |

|---|---|---|

| Gross Profit | $4,725,000,000 (Q4 2024) | $4,596,000,000 |

| Total Revenue | $11,959,000,000 (Q4 2024) | $11,533,000,000 |

| Net Income | $6,883,000,000 (Q4 2024) | $1,776,000,000 |

| EBIT | $1,026,000,000 (Q4 2024) | $1,228,000,000 |

Waymo in Austin Is Outperforming Human Drivers

Uber’s autonomous vehicle deployment with Waymo in Austin is exceeding expectations—not just in adoption, but in operational intensity. Dara Khosrowshahi noted that the average Waymo vehicle is now “busier than 99% of Austin drivers,” in terms of trips per vehicle per day.

This stat signals not only high consumer acceptance but operational readiness for scaling AV fleets. It’s a meaningful benchmark that speaks to a key inflection point in AV viability—one of the industry’s most-watched themes.

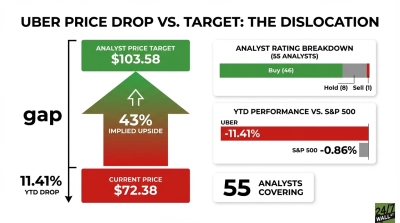

America’s best-known ride-share company, Uber Technologies (NYSE:UBER | UBER Price Prediction), took its investors on a scary trip early Wednesday morning. That’s because UBER stock tumbled after Uber released its first-quarter 2025 financial data.

Were Uber Technologies’ results really all that bad, though? Instead of obsessing about the crowd’s reaction, investors should join me as I embark on a fact-finding mission. Then, you might consider building generational wealth with a few shares of UBER.

Why Did UBER Stock Slump?

Soon after the opening bell on Wednesday, Uber Technologies stock tumbled to around $80. This happened even though the major stock market indexes were up.

After that, UBER stock recovered somewhat but remained in the red. Clearly, the trading community was in a sour mood as they reacted to Uber’s just-released Q1 2025 results.

Generally, I view it as a wealth-building opportunity when the market overreacts to news that’s not really all that bad. In this case, Uber Technologies posted a mild top-line miss.

Specifically, Uber generated revenue of $11.533 billion in this year’s first quarter. That’s below Wall Street’s consensus estimate of $11.6 billion, so technically speaking, it’s a revenue miss for Uber Technologies.

I looked far and wide, and couldn’t find any other problem with Uber’s quarterly results. It was a very slight revenue miss, which really ought to be called an in-line result rather than a miss.

Besides, Uber Technologies’ revenue for Q1 grew 17% year over year, which is perfectly respectable. Sometimes, short-term stock traders can be irrational and their expectations can be unreasonable. Yet, that’s great news if you’ve been waiting for a good time to build a position in UBER stock.

More Users, More Trips

Before getting to the bottom-line results, we should take a deep dive into Uber Technologies’ first-quarter stats that don’t include dollar figures. If you’re going to be serious Uber investor, there are some need-to-know metrics that don’t involve dollar signs but are important nonetheless.

First of all, you should want to know whether Uber Technologies is growing its user base. The company measures its pool of users as Monthly Active Platform Consumers or MAPCs.

During the first quarter of 2025, Uber recorded 170 million MAPCs. That’s 14% greater than the company’s 149 million MAPCs from 2024’s first quarter.

Are these customers using Uber’s ride-hailing services frequently, though? The answer is definitely yes, as Uber Technologies reported an 18% year-on-year increase in trips to 3.036 billion. (Uber defines trips as the “number of completed consumer Mobility rides and Delivery orders in a given period.”)

In light of these impressive stats, Uber Technologies CEO Dara Khosrowshahi certainly earned some bragging rights. “We kicked off the year with yet another quarter of profitable growth at scale, with trips up 18% and even stronger user retention,” Khosrowshahi proclaimed.

Traders Disregard a Bottom-Line Beat

It’s funny how stock traders can disregard a slew of great data points and only focus on one result that falls short of expectations. But again, this is how buying opportunities arise sometimes.

We already touched upon Uber Technologies’ solid growth in MAPCs and trips. Knowing those data points, it makes sense that Uber’s Q1 2025 gross bookings increased 14% year over year to $42.818 billion.

That’s just the beginning, however. Next, we can look at Uber Technologies’ adjusted EBITDA, which grew 35% to $1.868 billion.

Not convinced yet? Then consider Uber’s net cash provided by operating activities, which rose 64% to $2.324 billion. On top of all that, Uber Technologies’ free cash flow (FCF) grew a whopping 66% to $2.25 billion.

The bottom line that everyone wants to see, of course, is Uber’s first-quarter 2025 income. As it turns out, the net income/loss attributable to Uber Technologies improved dramatically from a $654 million loss in Q1 2025 to income of $1.776 billion in Q1 2025.

In addition, Uber posted diluted earnings of $0.83 per share. This easily outpaced the company’s loss of $0.32 per share in the year-earlier quarter. It also beat Wall Street’s consensus call for first-quarter 2025 earnings of $0.51 per share.

What we have here is a bottom-line Street beat that short-term traders disregarded. They also ignored Uber Technologies’ growth across multiple important metrics.

In other words, Uber absolutely did overrun first-quarter earnings even though UBER stock didn’t reflect this at all. Are short-term stock traders too spoiled to appreciate Uber Technologies’ progress, or are they just worried about the future of the economy?

Rather than try to figure out what these traders are thinking, you can choose to stay calm and assess the data objectively. Uber Technologies performed well in this year’s first quarter, so don’t be too surprised if UBER stock takes forward-thinking investors on a ride to higher share prices in 2025.

Contact [email protected] for any questions or corrections.

David Moadel is financial writer specializing in stocks, ETFs, options, precious metals, and Bitcoin. David has written well over 1,000 articles for leading online publications, helping investors understand markets, income strategies, and risk.

His work has appeared in The Motley Fool, InvestorPlace, U.S. News & World Report, TipRanks, ValueWalk, Benzinga, Market Realist, TalkMarkets, Finmasters, 24/7 Wall St., and others.

With a master’s degree in education, David has taught at the elementary, high school, and college levels. That teaching background shapes his writing style: clear, educational, and practical. David has also built a loyal social-media audience by providing trustworthy financial content on YouTube, X/Twitter, and StockTwits.

© Sundry Photography / iStock Editorial via Getty Images