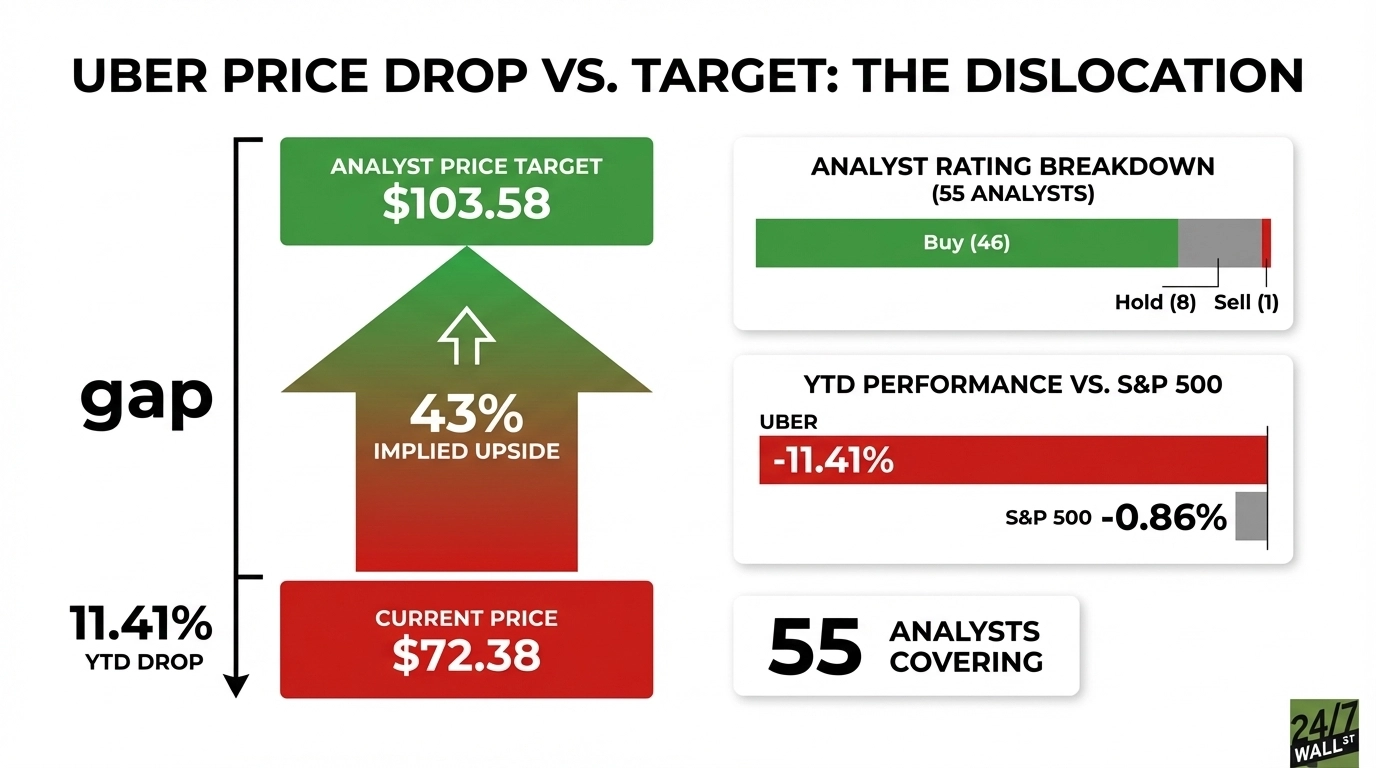

Uber Technologies (NYSE:UBER | UBER Price Prediction) currently trades at $72.38, while the Wall Street consensus price target sits at $103.58. That gap represents roughly 43% implied upside, which seems promising for a high-quality business like Uber.

Uber operates a global platform spanning ride-hailing, food delivery, and freight logistics, with 202 million monthly active platform consumers and more than 40 million trips per day.

A Stock That Keeps Selling Off on Good News

Uber posted Q4 2025 earnings with non-GAAP EPS of $0.71, missing the $0.78 consensus estimate, falling short of expectations. The miss stemmed from a $1.60 billion pre-tax headwind from equity investment revaluations, a non-cash item unrelated to operational performance. The quarter was operationally strong with trips growing 22% year-over-year to 3.8 billion, and free cash flow hitting a record $2.81 billion, up 65% year-over-year.

However, the market has punished Uber for headline EPS noise, compounded by the broader 2026 growth-stock selloff. Uber is down 11.41% year-to-date, sitting near its 52-week low of $68.34.

Why 55 Analysts Still See a Path Back Above $100

Of the analysts covering Uber, 46 rate it a Buy, 8 rate it a Hold, and just 1 rates it a Sell. That lopsided consensus reflects that most analysts think the stock is undervalued.

The next leg of the story comes down to new growth drivers, particularly autonomous vehicle monetization and Delivery acceleration. Uber committed over $100 million to build AV charging infrastructure and has more than 20 autonomous partners globally. CEO Dara Khosrowshahi stated the company has a “clear path to becoming the largest facilitator of AV trips in the world.” If Uber converts platform scale into AV trip facilitation fees, unit economics improve without proportional cost increases. Delivery already demonstrates this leverage, with adjusted EBITDA up 40% year-over-year in Q4 2025 on revenue growth of 30%.

Near-term guidance also supports the bull case. For Q1 2026, Uber guided to Gross Bookings of $52.0 billion to $53.5 billion and non-GAAP EPS of $0.65 to $0.72, implying 37% year-over-year growth at the midpoint. The company has a track record of guiding conservatively. In Q4 2025, Gross Bookings came in at $54.14 billion, above the high end of its own range, which has led some investors to treat guidance more as a baseline than a ceiling.

Insider activity adds another layer to the story. Uber’s CFO recently made an open-market purchase of 22,400 shares at $71.25, a discretionary buy at current levels. That kind of purchase tends to carry more weight than standard equity compensation and suggests management sees value in the stock at these prices.

The Stock is Down, But the Fundamentals Tell a Different Story

Uber trades at $72.38, well below the analyst consensus target of $103.58, which implies about 43% upside. The valuation does not look demanding. The stock trades at 15x trailing earnings and 22x forward earnings, even as revenue continues to grow around 20% year over year. Shares are also down roughly 29% from the 52-week high of $101.99, showing how much sentiment has pulled back. At the same time, 55 analysts still lean bullish, which suggests this is not just a speculative setup.

Recent performance highlights the disconnect. Uber is down 11.41% year to date in 2026, compared to just a 0.86% decline for the S&P 500. That is a meaningful gap for a company that is still reporting strong growth and record cash flow. The stock is also trading below both its 50-day moving average of $74.56 and its 200-day moving average of $86.86, which points to continued selling pressure without a clear bottom yet forming.

Worth Buying Here If the Cash Flow Story Wins Out

The bull case comes down to whether the market starts valuing Uber on free cash flow instead of noisy EPS. A business generating nearly $10 billion in annual free cash flow and growing that figure at more than 40% per year should command a higher multiple. On top of that, the AV opportunity adds real optionality that is not fully reflected in the stock. If even a fraction of the robotaxi opportunity materializes through Uber’s platform, upside becomes compelling well above consensus.

The bear case centers on sentiment and structural costs. Continued EPS volatility could keep weighing on investor confidence, especially if the broader growth-stock re-rating continues. Insurance reserves have climbed to $3.387 billion, and long-term debt has increased to $10.521 billion, which adds real cost pressure to the model. Regulatory risk around worker classification also remains in the background. When a stock sells off despite strong operational performance, it suggests sentiment is a bigger driver than fundamentals in the near term.

Even with the setup clearly in place, recent price action suggests the market may need a clean Q1 2026 report to reset sentiment.

Contact [email protected] for any questions or corrections.