Abbott’s CEO Excited About Momentum into 2026

Live Blog Update #7 Published

← Back to Full Coverage: Live: Abbott Labs (NYSE: ABT) Sinks 6% After Releasing Q2 Earnings

One note, Abbott CEO Robert Ford specifically cited momentum into 2026 in his commentary.

“Halfway through the year, we delivered high single-digit organic sales growth, double-digit EPS growth, significantly expanded our margin profiles, and continued to advance key programs through our new product pipeline. We see this momentum carrying into 2026.”

While shares are currently down 3.8%, if management issues bullish commentary on long-term momentum in their conference call, it could help blunt the immediate losses shares have seen after the earnings release.

Contact [email protected] for any questions or corrections.

All Updates from Live Coverage

We’re approaching the end of the trading day and Abbott remains down 8%. At the end of the day, the company narrowing forward guidance appears to be Wall Street’s focus. After earnings Abbott trades for a P/E of about 15.6X, which is attractive for a company with its current earnings growth.

As of midday, shares of Abbott continue to trend lower. The company’s shares are down about 8%. While Abbott’s shares have plummeted today, they are still up about 7% year-to-date.

Here’s a look at Abbott’s growth rates:

| Metric | Q2 25 | Q2 2024 | YoY Change |

|---|---|---|---|

| revenue | $11.14B | $10.38B | 7.37% |

| gross profit | $5.87B | $5.81B | 1.05% |

| operating income | $2.05B | $1.72B | 19.09% |

| net income | $1.78B | $1.30B | 36.64% |

While shares are down today, the company is posting impressive for a stock now trading at 16X earnings.

Q&A highlights:

- 2026 Outlook: Ford: “High single-digits sales, double-digit EPS reasonable… headwinds lap, launches accelerate.” Comfortable with consensus.

- M&A: Selective in Diagnostics/Devices; strong organic pipeline allows focus on ROIC.

- Litigation: Ford: “Stand behind [infant formula] safety… supported by medical/regulatory community; small revenue impact.”

- Libre/EP Trends: U.S. Libre +26% (basal/non-insulin growth); EP double-digits, Volt feedback “excellent.”

Breaking down segments: Medical Devices led with 12% growth (Diabetes Care +19.5%, Heart Failure +14%, Structural Heart +12%). Nutrition +3.5% (Adult +6.5% on Ensure/Glucerna). EPD +8% (Key 15 markets hit $1B first time). Diagnostics -1.5% (COVID/China drag; ex-China Core Lab +8%). Ford: “Diversified model resilient… Devices momentum from pipeline.”

|

Segment

|

Q2 Growth

|

Key Drivers

|

|

|

Medical Devices

|

+12%

|

Libre $1.9B (+19.5%), EP/Structural Heart double-digits

|

|

|

Nutrition

|

+3.5%

|

Adult +6.5% (protein/diabetes demand)

|

|

|

EPD

|

+8%

|

Branded generics in emerging markets

|

|

|

Diagnostics

|

-1.5%

|

|

CEO Ford addressed Q2 beats but highlighted ~$1B+ headwinds dragging Diagnostics: COVID sales drop, China VBP delays (volume recovery pushed to Q4), and HIV testing funding cuts.

Ex these, organic growth ~8.5%. Guidance narrowed: FY organic ex-COVID 7.5-8% (was 7-9%), EPS $5.10-$5.20 (high end down $0.05). Q3 EPS $1.28-$1.32.

Ford: “Derisked for transitory items… momentum into 2026 with launches.” Tariffs: $200M impact absorbed.

The current price target for ABT is $142.55, which after the sell-off this morning, is a 13.75% premium. Of the 26 Wall Street analysts covering ABT, the consensus opinion is an “Outperform” rating.

Abbott Labs conference call still about an hour away, meanwhile the stock continues to slide in pre-market trading, now down 4.85% as of 8 AM EDT.

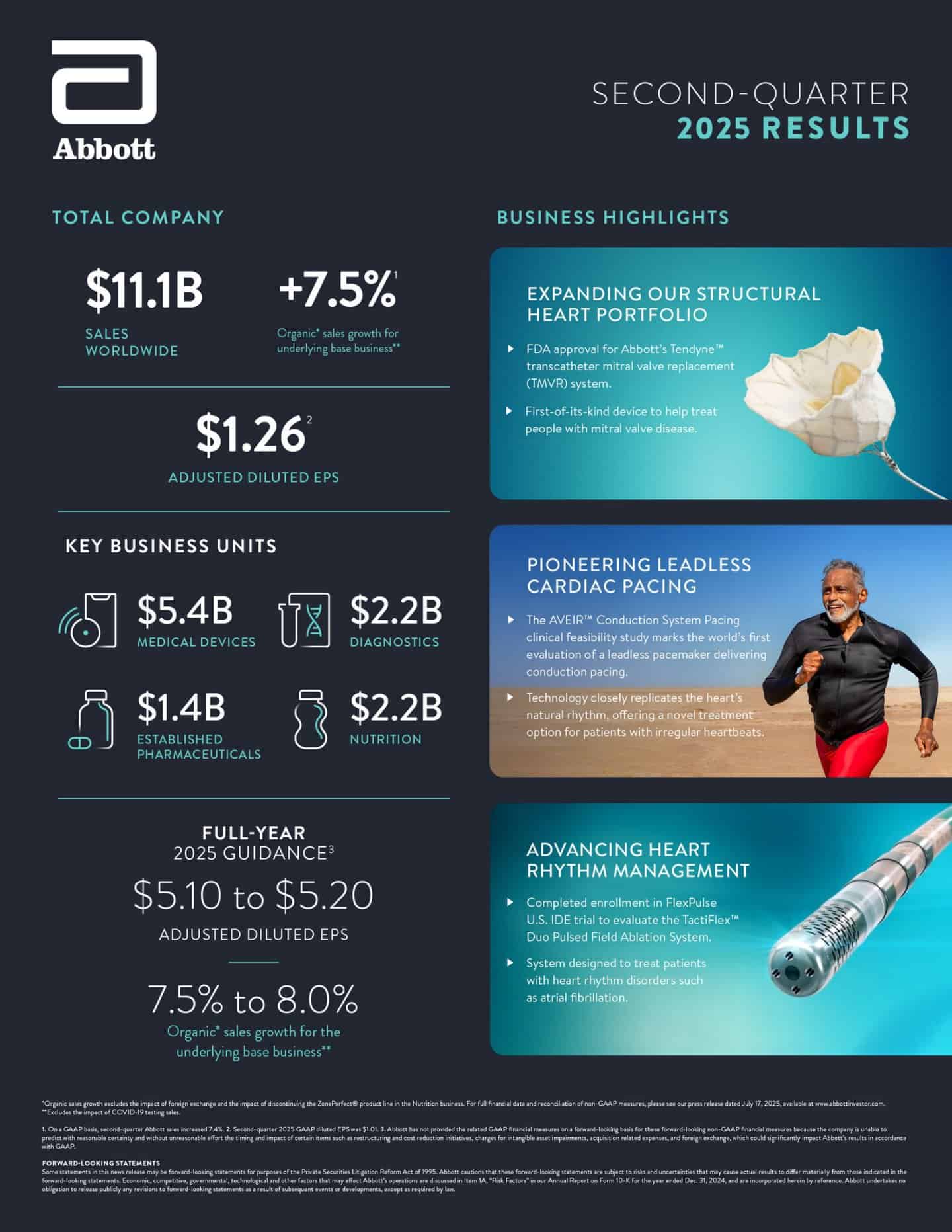

We’ve given the headline figures, but here’s a longer summary of Abbott’s Q2 earnings:

Abbott Laboratories reported strong results for the second quarter of 2025, with total sales reaching $11.142 billion, representing a 7.4% increase year-over-year.

Organic sales growth was 6.9%, or 7.5% when excluding COVID-19 testing-related sales, reflecting robust demand across most business segments.

Adjusted diluted EPS came in at $1.26, up 10.5% from the prior year and matching the Q2 2025 analyst consensus estimate of $1.26.

The company achieved significant margin expansion, with adjusted gross margin rising to 57.0% and adjusted operating margin to 22.9%.

Medical Devices led growth with a 13.4% sales increase, driven by strong performance in Diabetes Care, Heart Failure, Structural Heart, and Electrophysiology.

Diagnostics saw a slight decline due to lower COVID-19 testing sales and procurement headwinds in China, while Nutrition and Established Pharmaceuticals posted solid gains.

Full-year 2025 guidance was narrowed, now projecting organic sales growth (excluding COVID-19 tests) of 7.5%-8.0% and adjusted EPS of $5.10-$5.20.

The company also highlighted pipeline progress, including FDA approval for its Tendyne mitral valve system and plans for a new manufacturing facility. Abbott declared its 406th consecutive quarterly dividend, reinforcing its status as a Dividend Aristocrat.

Abbott shares are now down 3.6% as the company posted largely inline results and slightly took down the high-end of EPS estimates for the year.

Shares were up 16% year-to-date headed into today, so this could be investors taking money off the table. That is to say, when shares have outperformed the market, largely matching results leads to selling pressure.

Abbott has tightened the range on 2025 EPS from $5.05 to $5.25 down to $5.10 to $5.20.

Abbott’s quarter is out. We’ll post more analysis shortly, but the headline is in-line EPS ($1.26, matching Wall Street expectations) and revenue slightly ahead of expectations.

Shares are down 3% after the release.

We continue to monitor for Abbott’s earnings, but as of 7:05 a.m., they still haven’t posted to the company’s investor relations page.

Abbott will host its conference call at 9 a.m. ET today. If you’d like to join, you can sign up to listen to the call at this link.

Eric Bleeker has been investing for more than 20 years. He began his career working at Microsoft before joining Motley Fool, one of the largest publishers of financial research. In his 15 years at Motley Fool Eric served as the General Manager for Fool.com and led coverage in the Technology & Telecom sector. In addition, he was a featured columnist and has hosted dozens of investing seminars attended by more than a million total investors. Eric has more than 1,000 financial bylines to his name and has been featured in The Wall Street Journal, CNBC, Fox Business, and many other leading publications. He is currently focused on artificial intelligence investing and is a CFA Charterholoder.