Retirement forces some of the most consequential financial decisions a person will ever make. How much house can you afford? Should you help pay for your kids’ college at the expense of your own nest egg? And then there is perhaps the most pivotal question of all: when should you start collecting Social Security?

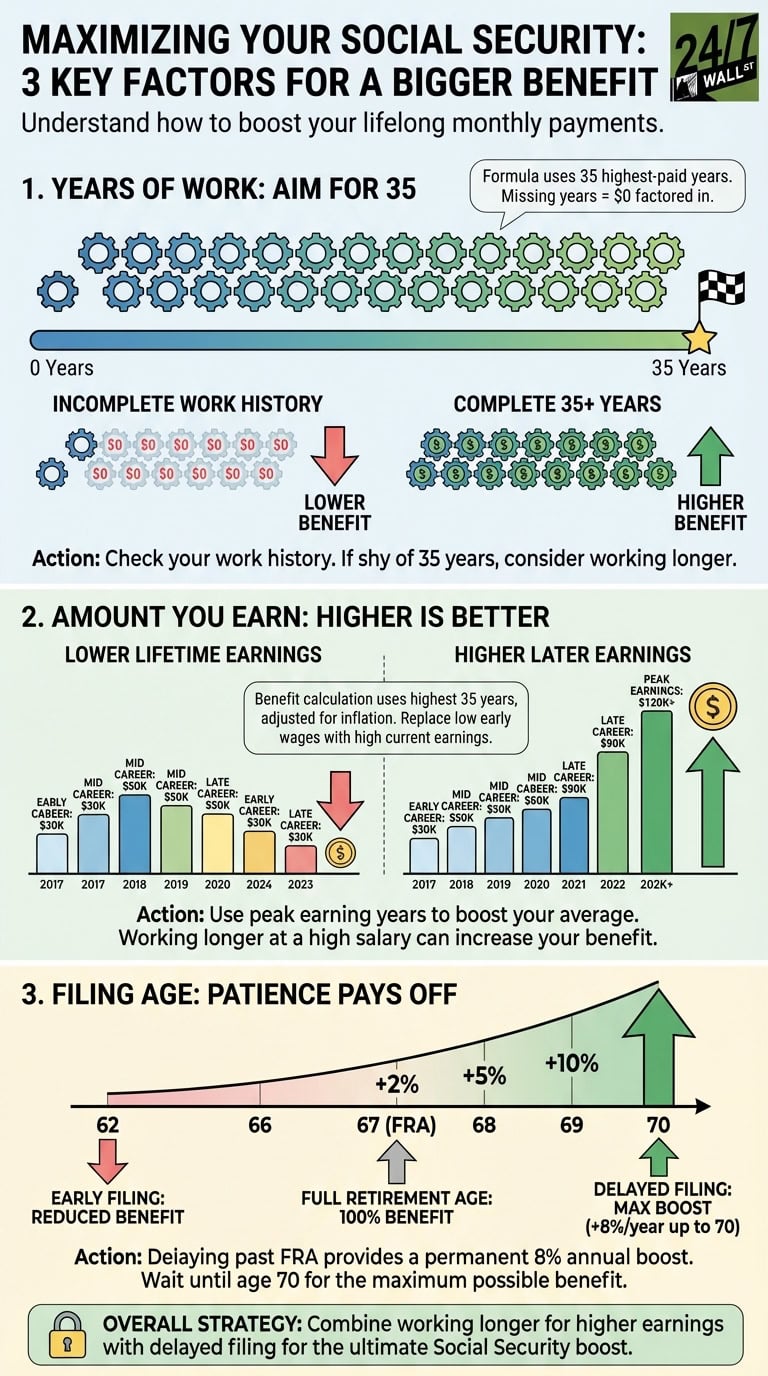

The answer is far from obvious. You can file as early as 62, but doing so permanently shrinks your monthly check. Wait until full retirement age (FRA) and you collect 100% of your earned benefit. Keep waiting, up to age 70, and your monthly payment grows even further.

For anyone born in 1960 or later, FRA is 67. Filing at 62 triggers a permanent 30% reduction in monthly benefits. Every year you delay past FRA adds a guaranteed 8% to your monthly payment, up to age 70. On a standard $2,000 monthly benefit, that math produces roughly $1,400 at 62 versus about $2,500 at 70, a gap of more than $13,000 per year for life.

Personal finance personality Dave Ramsey has a clear, and frequently debated, take on this decision: claim at 62. Here is why he believes that, and why his view deserves a closer look from both sides.

Why Ramsey believes in signing up for Social Security at 62

Ramsey’s core argument is a simple mortality calculation. As he has told listeners and readers, “Your retirement payments die when you die…so you might as well take the money and make the most of it while you can.” His reasoning: if you don’t live a long life, claiming early maximizes your total payout. Because no one can predict their lifespan with certainty at 62, he favors taking the money sooner rather than gambling on a longer life.

The second pillar of his argument is investment. Rather than letting the government hold your money while you wait for a bigger check, Ramsey suggests routing those early Social Security payments directly into a diversified mutual fund. He has argued that “you can do a much better job investing that money than the government ever could,” pointing to the long-run historical returns of broad equity portfolios. In his view, eight years of compounding on early Social Security payments can more than offset the guaranteed 8% annual boost available from delayed filing.

Importantly, Ramsey does not recommend collecting early just to spend it. His advice is premised on being debt-free, having emergency savings, and actually investing every dollar of those early checks. For retirees who meet those conditions, he frames the early-claim strategy as a genuine wealth-building tool rather than a shortcut.

A significant and growing shadow now hangs over Social Security as a whole. The 2026 Social Security Trustees Report, released June 9, projects that the OASI Trust Fund will be depleted in the fourth quarter of 2032, one quarter earlier than the 2025 report estimated. At that point, ongoing payroll tax revenue would cover only 78% of scheduled benefits. Part of the acceleration stems from the One Big Beautiful Bill Act, signed into law on July 4, 2025, which created a temporary $6,000 senior deduction for taxpayers age 65 and older through 2028. By lowering beneficiaries’ federal tax liability on Social Security income, the law reduced the tax revenue flowing back into the trust fund. That looming shortfall is a core reason Ramsey urges people to treat Social Security as a bonus rather than a foundation.

The break-even math Ramsey overlooks

Filing at 62 gives you a five-year head start on collecting checks, but at the cost of a permanent 30% reduction in your monthly payment. Actuarial calculations place the break-even point, the age at which a delayed filer’s cumulative lifetime benefits catch up with and surpass those of an early filer, somewhere between 78 and 78.5 years old. Anyone who lives longer than that comes out ahead by waiting.

The longevity data cuts against the early-claim assumption. According to the most recent CDC mortality statistics, a 65-year-old American can expect to live roughly 19.7 additional years on average, placing a typical retiree well into their mid-80s. Women at 65 can expect another 20.8 years; men, another 18.4 years. Claiming at 62 is essentially a bet that you will not outlive the statistical median, and for a large share of retirees, those are poor odds.

The tax drag of “claiming to invest”

Routing early Social Security payments into a taxable investment portfolio, as Ramsey recommends, introduces tax complications that can erode the strategy’s advantages. When a retiree’s provisional income exceeds $34,000 for single filers or $44,000 for married couples filing jointly, up to 85% of Social Security benefits become subject to federal income tax. This effect, commonly called the “tax torpedo,” can push retirees into higher marginal brackets they would not otherwise reach.

There is also the Medicare cost to consider. Generating additional capital gains and dividend income from newly invested Social Security checks can push a retiree’s modified adjusted gross income above the Income-Related Monthly Adjustment Amount (IRMAA) thresholds, triggering higher Medicare Part B and Part D premiums. Because IRMAA is calculated using income from two years prior, those premium surcharges arrive as a delayed and often surprising bill.

It is worth noting that the One Big Beautiful Bill Act’s $6,000 senior deduction may partially offset the tax torpedo for moderate-income retirees from 2025 through 2028. Higher-income seniors, however, see the deduction phase out above $75,000 in modified adjusted gross income, so the relief is not universal.

The working-and-filing trap (the earnings test)

Retirees who claim benefits at 62 while still earning a paycheck face a direct financial penalty. Under the Social Security earnings test, anyone who has not yet reached FRA and earns more than $24,480 in 2026 will have $1 in benefits withheld for every $2 earned above that threshold. In the year a retiree reaches FRA, a more generous rule applies: benefits are reduced by $1 for every $3 earned above $65,160. The withheld amounts are eventually restored through higher monthly payments once the retiree reaches FRA, but the interim cash-flow disruption can be severe, especially for anyone counting on those checks to fund investments.

The practical implication is clear: to execute Ramsey’s claim-and-invest strategy as he describes it, a retiree generally needs to be fully retired at 62 with enough savings to cover living expenses while directing Social Security income into the market. That is a prerequisite many 62-year-olds have not yet met. For anyone still working, filing early can mean receiving little to no Social Security income for portions of the year while the benefit reduction remains permanent.

How to decide when to claim Social Security

The right claiming age is genuinely personal. A few honest questions can clarify the decision:

- How much income will my savings provide outside of Social Security?

- How good is my health, and do I think I’ll live an average lifespan or longer?

- What does my family history of longevity look like?

- Do I want to continue working in retirement, or will I need larger benefits to make ends meet?

- How will my early filing choice affect the long-term survivor benefits for my spouse if I am the higher earner?

- Will my total provisional income from investments inadvertently trigger higher taxes or Medicare IRMAA premium surcharges?

A financial advisor can work through these variables with your specific numbers. The stakes are high enough, and the decision permanent enough, that a paid consultation is almost always worth the cost.

Editor’s note: This pass added context on the One Big Beautiful Bill Act (signed July 4, 2025), including its new $6,000 senior deduction and its role in accelerating the OASI Trust Fund depletion timeline as cited in the 2026 Social Security Trustees Report. It also incorporates the 2026 FRA-year earnings test threshold of $65,160, updated CDC 2024 life expectancy figures showing women at 65 can expect 20.8 more years and men 18.4 more years, and confirmation that the 2026 earnings test lower limit remains $24,480.

Contact [email protected] for any questions or corrections.