When interest rates rise, retirees face a pleasant problem: where to park cash reserves while earning more than near-zero yields. iShares 0-3 Month Treasury Bond ETF (NYSEARCA:SGOV) has emerged as a popular answer, offering Treasury Bill exposure with ETF convenience.

The Role It Plays: A Cash Alternative With Daily Liquidity

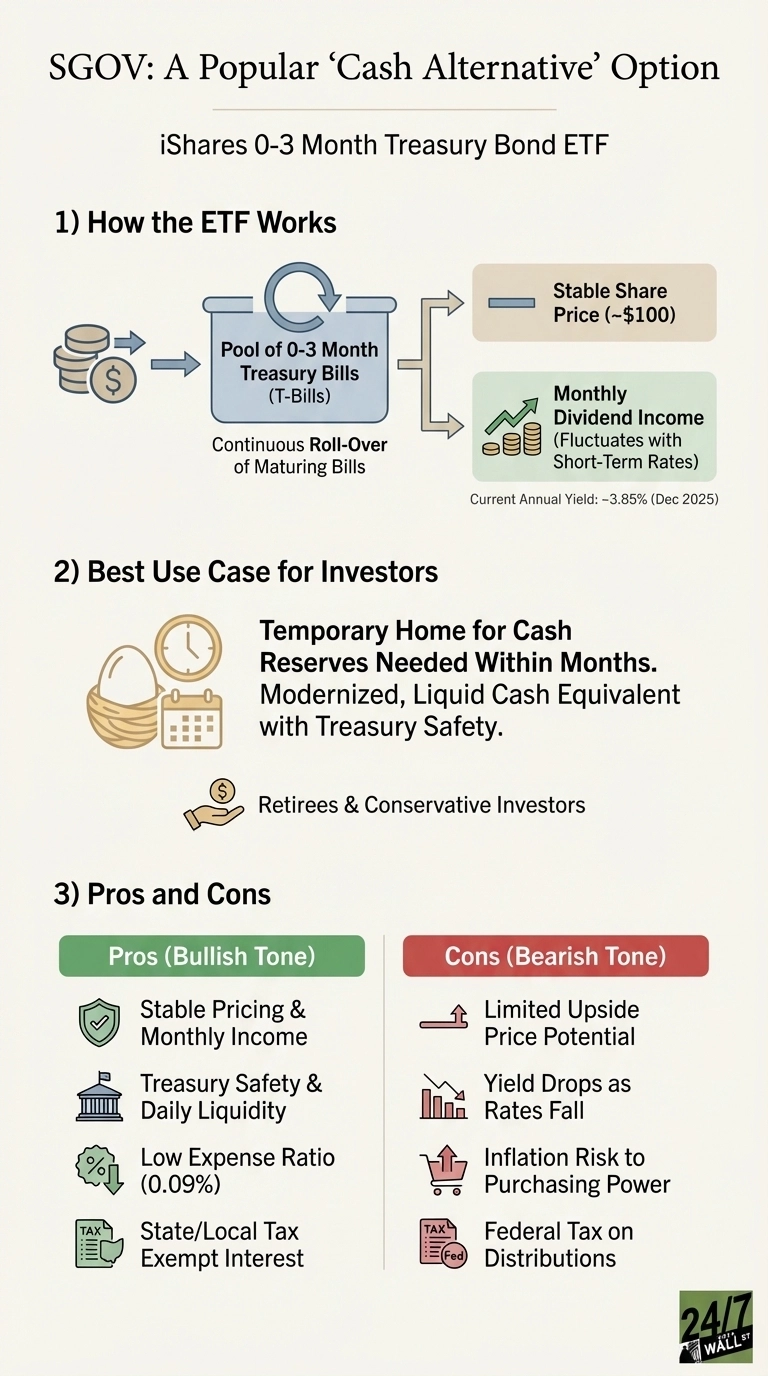

SGOV serves as a modernized cash equivalent for investors wanting Treasury safety without managing individual T-Bills. The fund holds ultra-short Treasury securities maturing in zero to three months, rolling over its portfolio continuously as bills mature. This creates stable pricing around $100 per share while generating monthly dividend income that fluctuates with short-term rates.

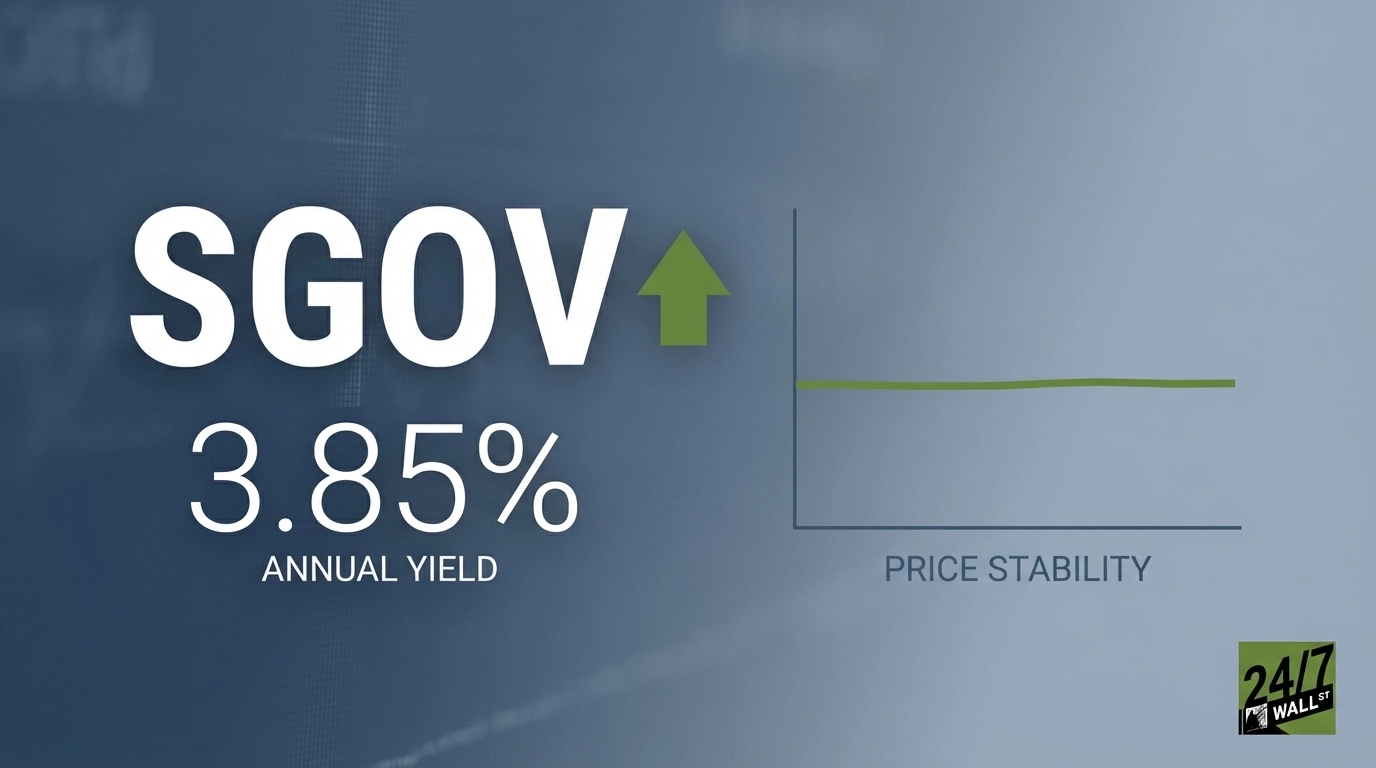

With $64.7 billion in assets and a 0.09% expense ratio, SGOV has become a default parking spot for conservative investors. The return engine is straightforward: you earn current short-term Treasury yields minus a minimal fee. As of today, that translates to approximately 3.85% annually, paid monthly.

The Federal Reserve cut rates to 3.5% to 3.75% in December 2025, following similar reductions earlier in the year. Market forecasts suggest further modest cuts in 2026, with median projections calling for rates to settle in the 3% to 3.5% range. SGOV’s yield will likely drift lower as the Fed continues normalizing policy.

Does It Deliver on the Promise?

SGOV accomplishes exactly what it sets out to do. Over the past year, the fund gained 0.38% in price appreciation but delivered roughly 4.2% in dividend income for a total return around 4.5%. Price has traded in an extraordinarily tight range between $100.38 and $100.72 over the past five months, demonstrating minimal volatility that makes it attractive as a cash substitute.

One Boglehead investor considering retirement options noted on Reddit that “SGOV seems to be a good choice as it is shorter term and more liquid than something like BND” when comparing fixed income alternatives. Monthly dividend payments have ranged from $0.31 to $0.36 per share throughout 2025, down from peaks above $0.45 in mid-2024 when Treasury yields were higher.

The Tradeoffs You Accept

SGOV’s safety comes at the cost of upside potential. When rates fall, you earn less income immediately since holdings mature and reinvest at lower yields within weeks. There’s no duration cushion to benefit from falling rates like longer-term bond funds enjoy. Inflation can erode purchasing power if Treasury yields don’t keep pace with rising prices.

Tax treatment deserves consideration. While Treasury interest is exempt from state and local taxes, you’ll owe federal income tax on distributions at ordinary income rates, making SGOV less attractive in taxable accounts for high-bracket investors compared to municipal money market funds.

Who Should Avoid SGOV

Investors seeking capital appreciation should look elsewhere. SGOV’s price barely moves, making it unsuitable for anyone hoping to grow wealth through price gains. Those with long time horizons would be better served by longer-duration bonds or equities offering higher expected returns over multi-decade periods.

Consider BIL as an Alternative

SPDR Bloomberg 1-3 Month T-Bill ETF (NYSEARCA:BIL) offers nearly identical exposure with $43.7 billion in assets and a 0.14% expense ratio. The key difference is cost: SGOV’s 0.09% fee means you keep an extra $50 annually for every $100,000 invested compared to BIL. For retirees managing substantial cash reserves, that difference compounds meaningfully. Both funds track short-term Treasury yields closely, but SGOV’s lower cost gives it a structural advantage.

SGOV works best as a temporary home for cash you’ll need within months, delivering Treasury safety with ETF liquidity, but its yield will decline alongside Fed rate cuts.

Contact [email protected] for any questions or corrections.