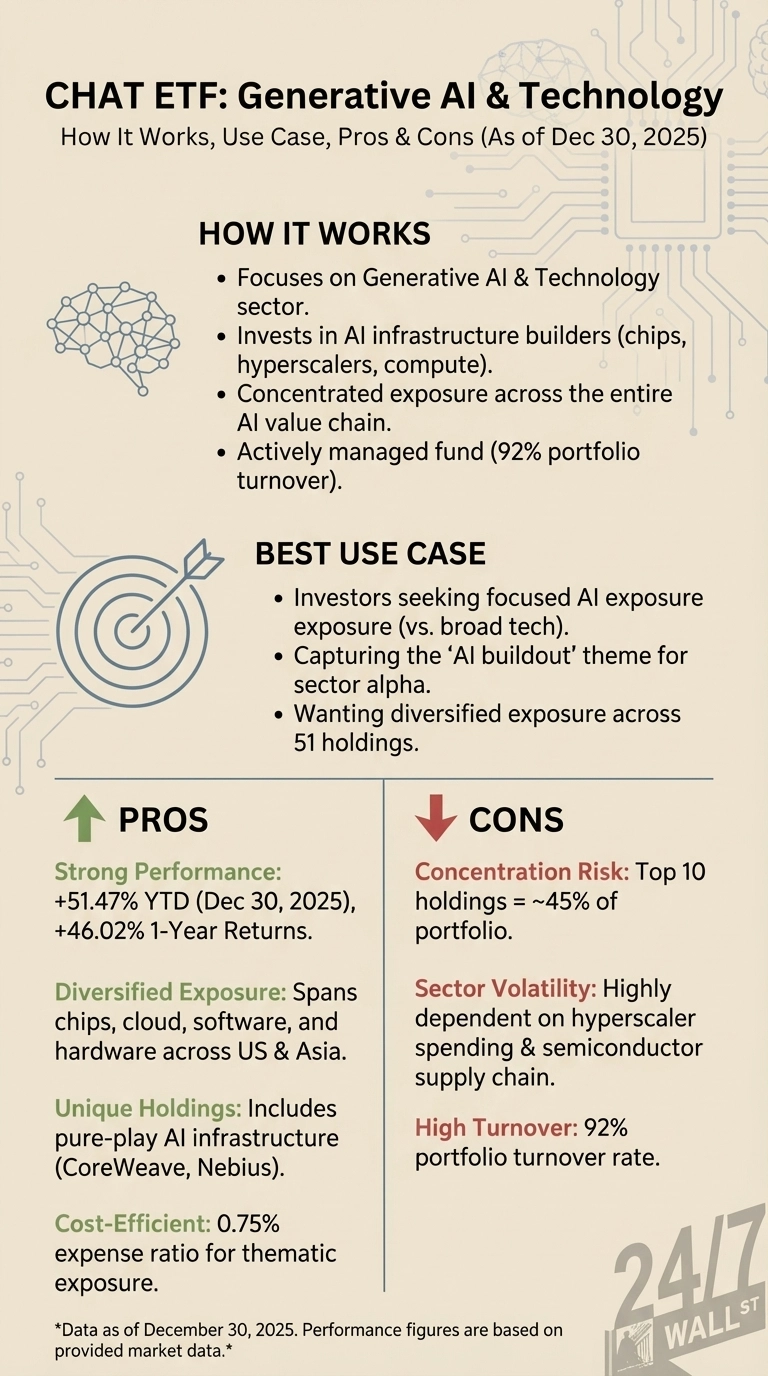

The Roundhill Generative AI & Technology ETF (NYSEARCA:CHAT) soared just over 45% in 2025, outpacing the S&P 500’s 17% gain and the Nasdaq-100’s 21% advance. The fund’s 2026 performance trajectory depends on hyperscaler spending on AI infrastructure and the fund’s concentrated exposure to companies building that infrastructure.

Hyperscaler Capital Spending Is the Engine

The biggest macro factor affecting CHAT’s performance is capital expenditure by the world’s largest cloud providers. According to Goldman Sachs Research, consensus estimates for 2026 capex by AI hyperscalers now stand at $527 billion, up from $465 billion at the start of third quarter earnings season. Analysts have consistently underestimated how much Amazon (NASDAQ:AMZN | AMZN Price Prediction), Google (NASDAQ:GOOGL), Microsoft (NASDAQ:MSFT), and Meta (NASDAQ:META) are willing to invest in AI infrastructure.

CHAT holds meaningful positions in all four hyperscalers. Alphabet is the fund’s largest holding at 7.6%, followed by Microsoft at 5.1%, Meta at 4.2%, and Amazon at 3.4%. When these companies report quarterly earnings, capex guidance and commentary about AI workload growth provide key signals. Any indication that spending will moderate could pressure the entire AI infrastructure chain, while continued aggressive investment supports the thesis.

Each hyperscaler provides capex guidance and discusses demand trends for AI compute during quarterly earnings season. Goldman Sachs Research notes that the market has become more selective, rotating away from AI infrastructure companies where operating earnings growth is under pressure. The market wants to see a clear link between capex and revenue growth.

Concentration Risk in the Chip Stack

CHAT’s heavy concentration in semiconductor and chip infrastructure companies matters most at the micro level. Nvidia (NASDAQ:NVDA) represents 6.3% of the portfolio, Advanced Micro Devices (NASDAQ:AMD) is 3.3%, Broadcom (NASDAQ:AVGO) is 3.0%, and SK Hynix is 3.2%. Together with other chip-related holdings like Taiwan Semiconductor (NYSE:TSM) and Samsung Electronics, the fund has significant semiconductor cycle exposure.

This concentration amplifies both upside and downside. When chip demand is strong and pricing power holds, CHAT outperforms. But if memory prices soften or GPU demand moderates, the fund feels it acutely. Supply constraints for high-bandwidth memory used in AI chips remain a key factor to monitor.

Roundhill’s monthly fact sheets and holdings files track any shifts in sector allocation or individual position sizes. The fund has a 92% portfolio turnover rate, meaning management actively adjusts positions. Changes in chip stock weighting versus software or cloud infrastructure can signal how the fund is positioning for the next phase of the AI buildout.

IGPT Offers Different Structure and Lower Costs

The Invesco AI and Next Gen Software ETF (NYSEARCA:IGPT) provides a different approach to AI exposure. IGPT charges a 0.56% expense ratio compared to CHAT’s 0.75%, and it has a longer track record dating back to 2005. The fund holds $628 million in assets and emphasizes software and communication services more heavily, with 53% in information technology and 19% in communication services.

IGPT’s top holdings include Alphabet at 9.3% and AMD at 8.8%, but it also has larger positions in software names like Adobe (NASDAQ:ADBE) and Snowflake (NYSE:SNOW). The fund also has lower turnover at 18%, suggesting a more passive approach.

The Bottom Line

CHAT’s performance in 2026 will hinge on whether hyperscaler capex continues climbing toward $500 billion and whether the semiconductor supply chain can sustain pricing power as memory and chip demand remains robust.

Contact [email protected] for any questions or corrections.