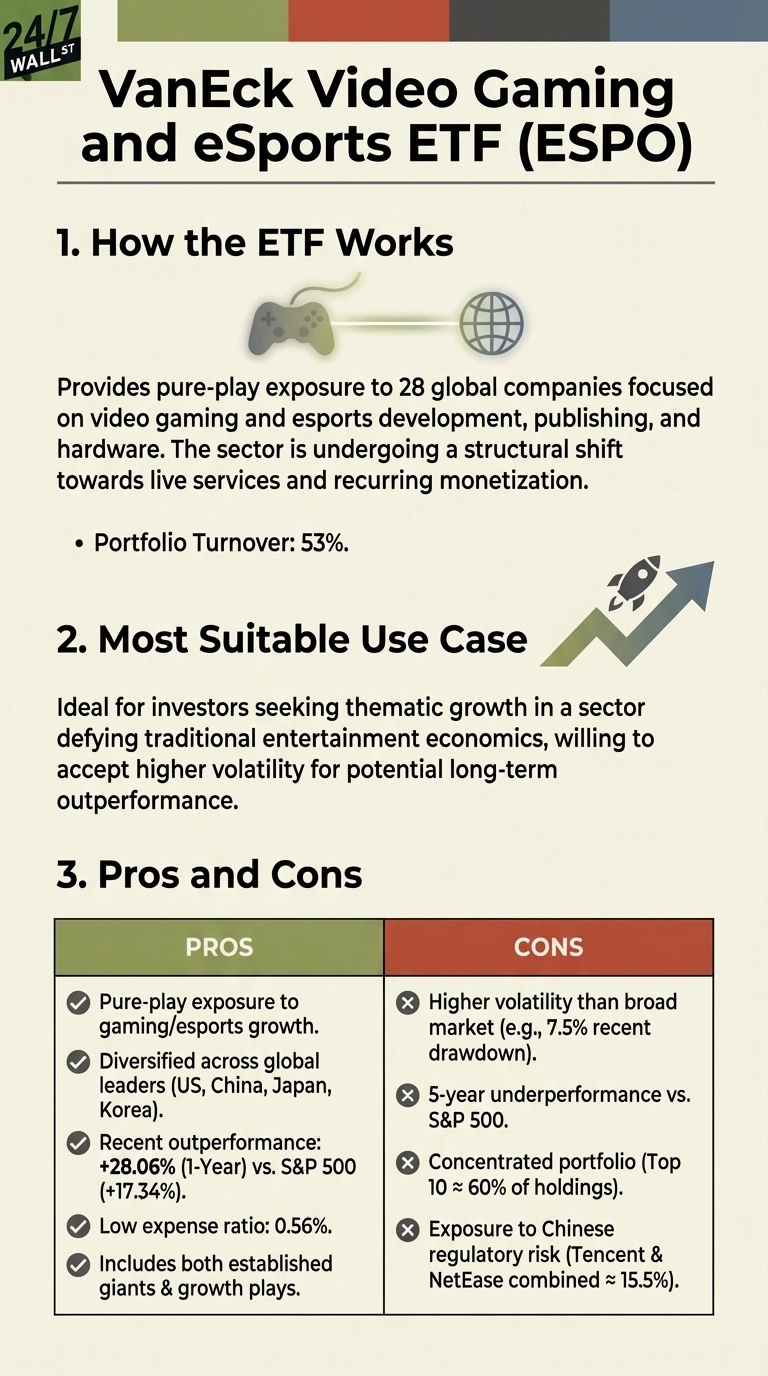

The VanEck Video Gaming and eSports ETF (NYSEARCA:ESPO) offers pure exposure to an industry defying traditional entertainment economics. With $405 million in assets and a 0.56% expense ratio, ESPO delivered 28% returns over the past year, outpacing the S&P 500 by nearly 11 percentage points. The fund holds 28 gaming companies, led by Tencent Holdings (NASDAQ:TCEHY) at 8.1%, Nintendo (NASDAQ:NTDOY) at 7.6%, and NetEase (NASDAQ:NTES | NTES Price Prediction) at 7.4%. Recent trading shows the ETF consolidating around $105 after hitting $111 in November 2025.

The Live Services Revenue Model Is Reshaping Gaming Economics

The biggest factor driving ESPO’s holdings forward is the structural shift toward live services and recurring monetization. Over 65% of all gaming revenue in 2025 came from live services and in-game purchases rather than upfront game sales. This represents a fundamental rewiring of how gaming companies generate cash flow.

This matters for ESPO investors because of predictability. Traditional gaming operated on a hit-or-miss cycle where studios lived and died by individual game launches. Live services turn games into platforms with subscription revenue, battle passes, seasonal content drops, and cosmetic purchases that generate income years after initial release. Electronic Arts (NASDAQ:EA), ESPO’s fourth-largest holding at 6.2%, exemplifies this transition. Despite a 51% earnings decline in its most recent quarter due to the cyclical nature of major releases, analysts expect significant earnings recovery, reflected in EA’s forward price-to-earnings ratio compressing from 60x to 23x.

Watch quarterly earnings reports from ESPO’s top holdings, specifically the split between premium game sales and live services revenue. EA, Take-Two Interactive (NASDAQ:TTWO), and Roblox (NYSE:RBLX) all break out these metrics in their investor presentations. When live services revenue accelerates while total player counts remain stable or grow modestly, it signals improving monetization efficiency. Monthly active user counts and average revenue per user are the two metrics that telegraph whether the live services model is working or stalling.

China Exposure Creates Concentrated Regulatory Risk

The most significant ETF-specific risk sits in ESPO’s top two holdings. Tencent and NetEase combine for over 15% of the portfolio, creating meaningful exposure to Chinese gaming regulation. Chinese authorities have repeatedly proposed restrictions on gaming monetization, including spending limits and warnings for what regulators call “irrational consumption behavior.” When these regulatory proposals surface, gaming stocks crater.

This isn’t theoretical risk. It’s structural exposure to policy decisions made outside market forces. For ESPO investors, monitoring Chinese regulatory announcements matters more than quarterly earnings from these holdings. The National Press and Publication Administration publishes game approval lists monthly. When approval rates slow or new restrictions appear in draft regulations, ESPO typically sells off regardless of underlying business performance at Tencent or NetEase.

Consider HERO for Broader Gaming Exposure

The Global X Video Games & Esports ETF (NASDAQ:HERO) offers a compelling alternative with $126 million in assets and a 0.50% expense ratio, slightly lower than ESPO. HERO’s top holding is Electronic Arts at 8.7%, followed by Take-Two Interactive at 7.1% and NetEase at 6.7%. The key difference: HERO holds 47 companies compared to ESPO’s 28, providing broader diversification across the gaming ecosystem. HERO also maintains lower China concentration, reducing single-country regulatory risk while preserving exposure to global gaming growth.

What Matters Most in 2026

The shift toward live services revenue will determine whether ESPO’s holdings can sustain premium valuations, while China regulatory decisions on gaming monetization represent the single largest downside catalyst for the fund’s concentrated top holdings.

Contact [email protected] for any questions or corrections.