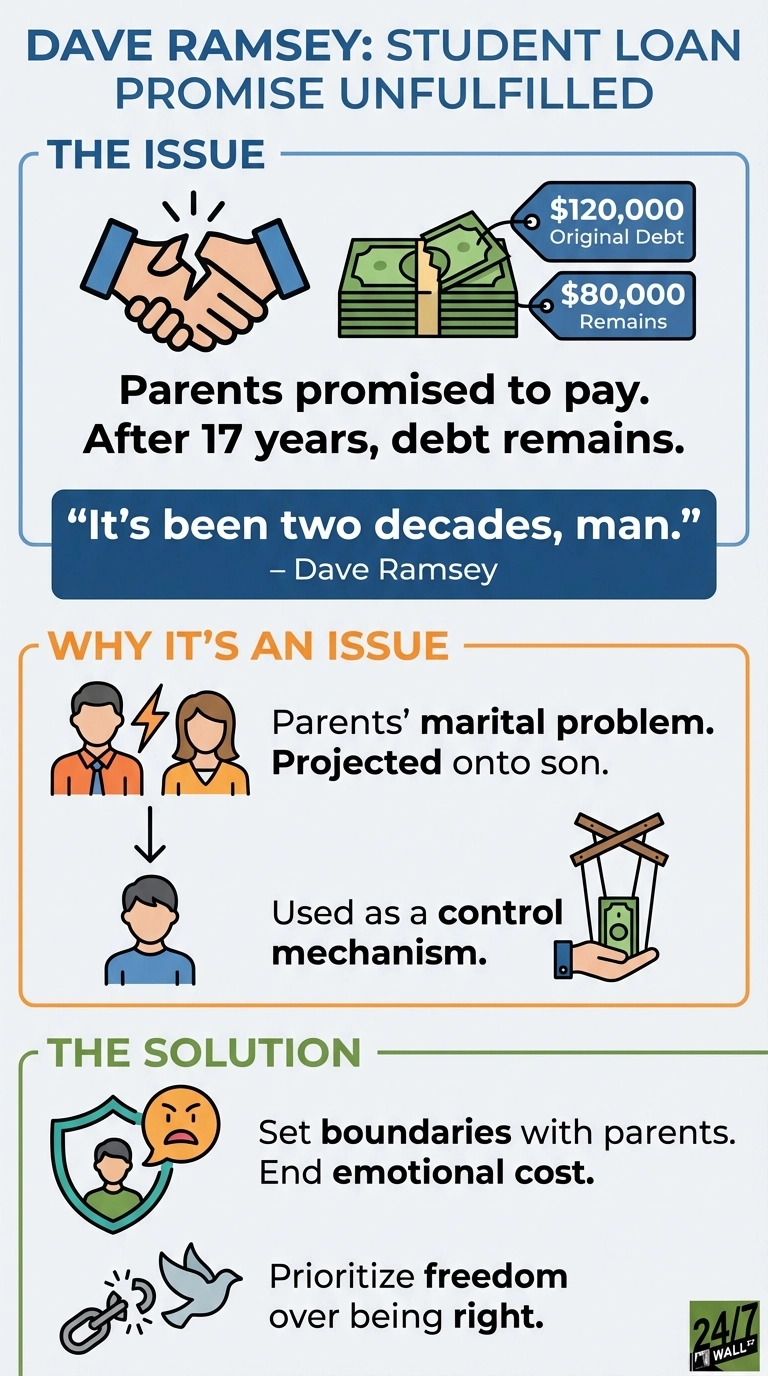

On a January 2026 episode of The Dave Ramsey Show, caller Shane laid out a situation that had festered for 17 years. His parents promised to pay his student loans when he was 18. The original debt was $120,000. Today, $80,000 remains. His parents are financially comfortable and continue making minimum payments, but his mother routinely criticizes how Shane spends his own money. “A lot of the times it’s like, oh, you just bought a truck, like that could have gone to the student loans,” Shane explained.

Ramsey cut straight to the heart of it: “It’s been two decades, man.” Working with co-host Jade Warshaw, he diagnosed the real dysfunction. This was no longer a debt problem. “This is now a marital problem they have of mom disagrees with how dad is handling a debt they agreed to pay,” Ramsey said. Shane had become the emotional proxy for a conflict his parents refused to resolve between themselves.

Why This Advice Resonates

Ramsey’s diagnosis speaks to anyone caught between broken promises and family guilt. After 17 years, Shane carries no obligation to fix his parents’ emotional mess. They made a commitment when he was barely an adult, and their failure to honor it while using his purchases as ammunition for criticism has created a dynamic that poisons every conversation. The real problem Ramsey identifies is not the debt itself. It is the passive-aggressive communication pattern that has corroded the relationship for close to two decades.

Families that use money as a control mechanism rarely recognize it clearly. Shane’s parents likely believe they are being responsible by spreading out payments. What they miss is that every comment about his truck or his spending transforms their original promise into ongoing leverage, converting a financial obligation into an emotional toll Shane pays every time they speak.

Where the Advice Holds Up

Ramsey is right that Shane needs firm boundaries with his mother. When parents make a financial commitment and then weaponize it for criticism, they violate the implicit contract behind that promise. If Shane’s parents can afford to make payments but choose to stretch this across two decades while commenting on his purchases, they are using the debt as a control tool rather than treating it as their own responsibility.

The marital conflict observation is particularly sharp. One parent likely wants to pay off the debt while the other resists. Rather than resolving this between themselves, they have made Shane the proxy for their disagreement. Every passive comment erodes trust and turns what should be a straightforward financial obligation into a relational minefield that Shane never asked to be placed in.

The Missing Context

Ramsey did not fully explore whether Shane’s parents’ financial circumstances changed dramatically after making the promise. If they agreed to pay $120,000 when they were financially secure and then faced job loss, medical expenses, or other shocks, the conversation becomes more nuanced. An honest discussion about changed circumstances is entirely reasonable. Seventeen years of minimum payments accompanied by guilt trips is not.

The advice also sidesteps important tax considerations that apply in 2026. If Shane’s parents have been claiming the student loan interest deduction while making payments, they can deduct up to $2,500 annually, subject to income limits. For 2026, the deduction phases out for single filers with modified adjusted gross income between $85,000 and $100,000, and for married joint filers between $175,000 and $205,000. If Shane’s parents were to pay off the remaining $80,000 balance, gift tax rules come into play. The 2026 annual gift tax exclusion is $19,000 per recipient, so amounts above that require filing Form 709, though actual tax is rarely owed. Under the One Big Beautiful Bill Act (OBBBA), signed into law on July 4, 2025, the lifetime gift and estate tax exemption was permanently raised to $15 million per person ($30 million for married couples), up from $13.99 million in 2025. Structuring any large payoff to minimize paperwork requires modest planning, but for most families the exemption is high enough that no actual gift tax would be owed.

The broader student loan landscape has also shifted significantly. The American Rescue Plan Act provision that shielded income-driven repayment (IDR) forgiveness from federal taxation expired on December 31, 2025. Borrowers who receive IDR forgiveness in 2026 or later now face taxable income on the forgiven amount, creating what experts call a “tax bomb.” For someone with $80,000 forgiven, the federal tax liability alone could exceed $12,000 depending on their bracket. Public Service Loan Forgiveness remains tax-free under a separate, permanent statutory provision. The OBBBA also restructured federal repayment options: for loans disbursed on or after July 1, 2026, the new Repayment Assistance Plan (RAP) replaces SAVE, PAYE, and ICR as the primary income-driven option, requiring 30 years of qualifying payments before forgiveness. Shane’s situation is a reminder that multi-decade debt arrangements increasingly collide with shifting policy, and the longer a family dispute stretches on, the more complex any resolution becomes.

How to Think About Broken Financial Promises

If you find yourself in Shane’s position, weigh whether ending the emotional cost is worth taking over the debt yourself, even when you are technically right. Being right can cost more than being free. Setting a boundary might mean saying, “I will take over the remaining balance so we can move forward without this hanging over every conversation.”

If you are a parent in a similar situation and circumstances have changed since you made the promise, have the honest conversation now. Seventeen years of resentment compounding with interest serves no one. If you made a commitment you now regret or cannot afford, own it directly rather than letting passive comments do the work. Financial promises that become emotional weapons destroy relationships far more effectively than they manage debt.

Editor’s note: This article was updated to reflect the 2026 gift and estate tax lifetime exemption increase to $15 million per person under the One Big Beautiful Bill Act (OBBBA), the restructuring of federal student loan repayment plans under OBBBA effective July 1, 2026, and the December 31, 2025 expiration of the American Rescue Plan Act provision that had shielded income-driven repayment forgiveness from federal taxation.

Contact [email protected] for any questions or corrections.