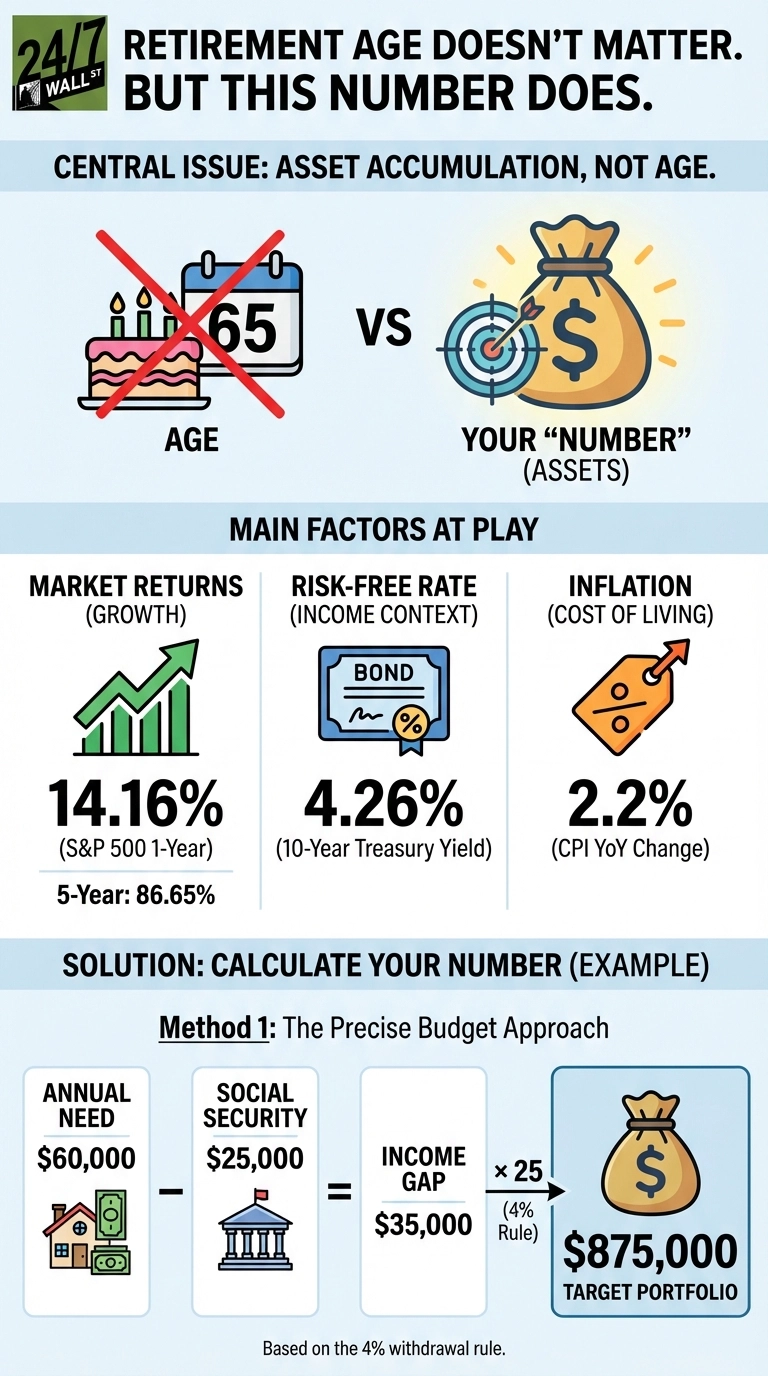

If you have a target retirement age circled on your calendar, you may be planning around the wrong metric. According to finance expert Dave Ramsey, retirement readiness is not determined by hitting 60, 65, or any other birthday milestone. What matters is whether you have accumulated enough invested assets to generate the income you need for the rest of your life.

The real question is not “Am I old enough to retire?” but “Do I have enough money to retire?” Your investment account balance, not your age, is what determines when you can afford to stop working. Here is how to calculate your personal financial number.

Consider This: Dave Ramsey: “You Make $140K. Stay Out of Restaurants, Don’t Go on Vacation, And Get Rid of the Ferrari Bike”

Three Methods to Calculate Your Retirement Number

Method 1: The Precise Budget Approach

This method delivers the most accurate result but requires detailed planning. Start by estimating your annual retirement spending, then subtract guaranteed income sources like Social Security to find your true income gap.

For example, if you need $60,000 annually and expect $25,000 from Social Security, your portfolio must generate $35,000 per year. The 4% rule, a widely accepted guideline, holds that you can withdraw 4% of your portfolio in year one and then adjust for inflation each subsequent year. Multiply your income gap by 25 to get your target: $35,000 x 25 = $875,000 needed.

The 4% rule works because historical data shows this withdrawal rate has sustained portfolios through 30-year retirement periods. That picture, however, has grown more nuanced in recent research. The rule’s original author, Bill Bengen, updated his “SAFEMAX” figure to 4.7% in his August 2025 book, arguing that a more diversified portfolio including small-cap and international equities supports a higher safe withdrawal rate. Morningstar, taking a more cautious, forward-looking approach, put the safe starting rate at 3.9% for 2026 retirees in its December 2025 analysis, up slightly from 3.7% the prior year as improved bond yields raised projected returns. Neither revision overturns the basic 4% math, but both suggest the right number for any individual depends on their portfolio mix and time horizon.

The macro backdrop also matters. Headline inflation ran as hot as 4.2% year-over-year in May 2026, its highest pace since April 2023, driven by an energy price surge tied to geopolitical tensions. By June 2026, however, the Consumer Price Index had cooled to 3.5% year-over-year as energy prices reversed sharply, dropping 5.7% for the month alone. That pullback provided some relief, though inflation remains well above the Federal Reserve’s 2% target. Meanwhile, 10-year Treasury yields stood near 4.63% in late July 2026, offering meaningful income on the bond side of a balanced portfolio. Taken together, today’s environment calls for more careful inflation modeling than the 4% rule’s original 1994 assumptions required.

Try This: Suze Orman Says This Is the One Expense You Must Cut in Retirement

Method 2: Income Replacement Ratio

For workers years away from retirement, pinning down exact future expenses can feel like guesswork. A practical shortcut is targeting 70% to 90% of your pre-retirement income. Someone earning $50,000 who aims for a 90% replacement rate would need $45,000 annually. Subtract projected Social Security income, then multiply the remaining gap by 25 to arrive at a nest-egg target. This method trades some precision for simplicity, making it well-suited for mid-career planning when the spending picture will sharpen over time.

Method 3: The 10x Rule

The simplest benchmark: multiply your final working salary by 10. A worker earning $100,000 at retirement should target a $1 million portfolio. Less precise than a full budget analysis, this rule gives younger savers a concrete number to orient around early in their careers, when compounding has the most time to do its work. Treat it as a starting point, not a finishing line.

Which Method Should You Use?

Your life stage drives the answer. Workers within five years of retirement benefit most from the precise budget approach. Mid-career professionals can rely on the income replacement ratio as a reliable compass. Younger workers can anchor to the 10x rule and refine their target as retirement draws nearer and their spending picture becomes clearer.

Ramsey’s core insight holds up under scrutiny: age is irrelevant if the assets are not there. A 55-year-old with $1.5 million invested is more retirement-ready than a 67-year-old carrying only $200,000. The number in your investment accounts, not the number of candles on your birthday cake, determines when you can truly stop working. If you have not yet reached your target, keep building your nest egg until the math actually works.

Editor’s note: This article has been updated to reflect the latest available market and economic data. The 10-year Treasury yield has risen to approximately 4.63% as of late July 2026, and the S&P 500 one-year total return stands at 16.48% as of July 24, 2026 per S&P Dow Jones Indices. Headline CPI inflation, which spiked to 4.2% in May 2026, cooled to 3.5% year-over-year in June after a sharp decline in energy prices. The article also incorporates updated 4% rule research, including Bill Bengen’s revised 4.7% SAFEMAX figure and Morningstar’s December 2025 safe starting rate estimate of 3.9% for 2026 retirees.

Contact [email protected] for any questions or corrections.