No matter where you go online, there is a better-than-good chance that you will see the 4% rule come up around the idea of retirement. This is basically the prevailing rule of thumb as to how much money you can withdraw every year and live on your investments indefinitely.

The problem with the 4% rule is that since it became one of the primary investment strategies, the market and retirement needs have shifted substantially. That raises a genuine question: is the 4% rule now outdated, and if so, what does a realistic retirement withdrawal strategy look like today?

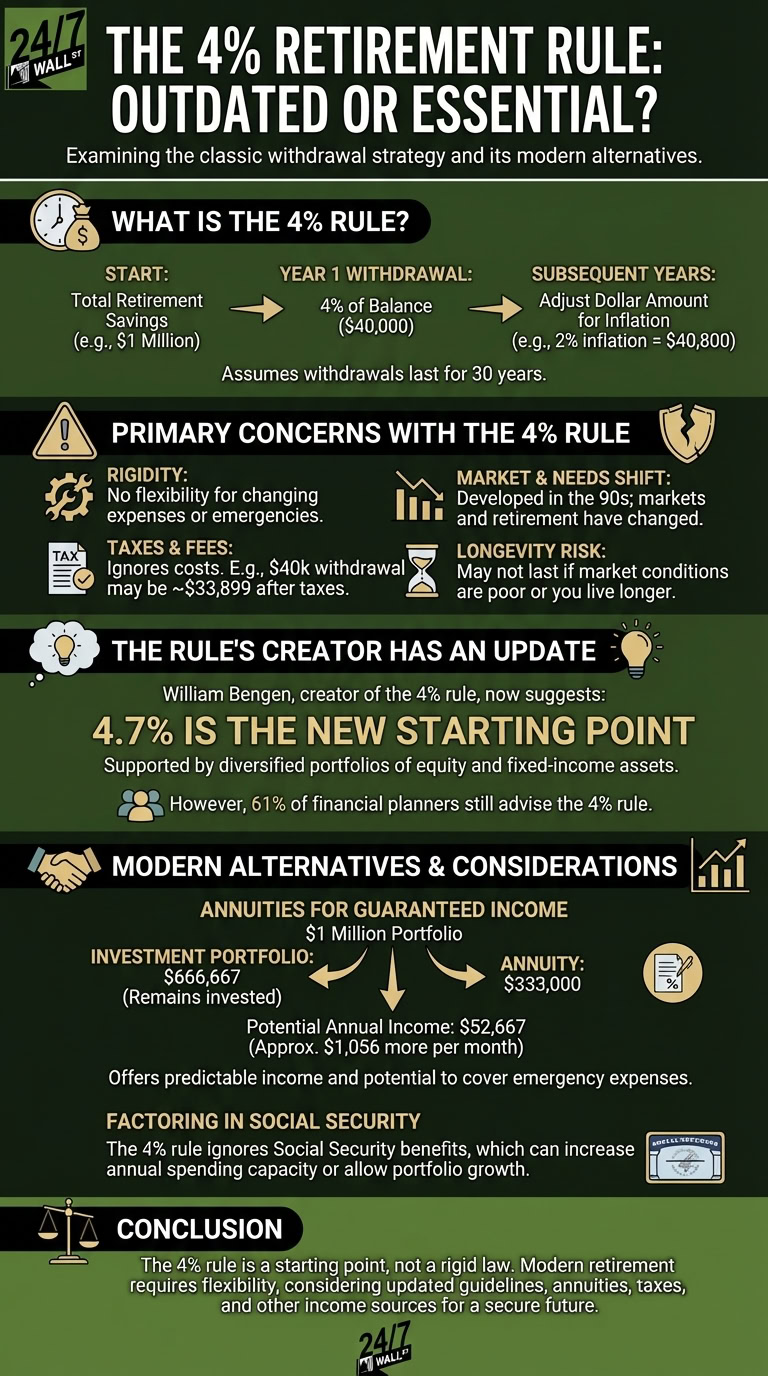

What Is the 4% Rule?

The 4% rule is straightforward in concept. A retiree takes the total value of all investments on day one of retirement and withdraws 4% of that balance during the first year. Each year after that, the dollar amount withdrawn is adjusted upward to keep pace with inflation. The core promise is that following this strategy makes it very unlikely a retiree will outlive their money over a 30-year span, which is generally longer than most people spend in retirement.

To put numbers to it: a retiree with $1 million in savings would withdraw $40,000 in year one. If inflation runs at 2% that year, the year-two withdrawal rises to $40,800. That same logic carries forward for three decades. The simplicity of the formula is a big part of why it caught on so widely after financial planner William Bengen first introduced it in the Journal of Financial Planning in 1994.

The deeper challenge with the rule is its rigidity. It assumes withdrawals increase only with inflation and never deviate from the original schedule, which rarely reflects how retirement spending actually behaves.

Primary Concerns Over the 4% Rule

Even though the 4% rule has earned broad acceptance over the decades, critics have long noted that its rigidity is also its greatest weakness. The rule provides no mechanism for spending more in any given year, regardless of the reason, whether that is a medical bill, a home repair, or a once-in-a-lifetime trip. Real retirement expenses fluctuate, and the formula simply does not account for that reality.

A related concern is the rule’s dependence on the 30-year assumption. If a retiree is forced to spend meaningfully more than planned during even a few of those years, the original math breaks down, and the portfolio may not hold up for the full three decades. The formula also assumes a specific portfolio mix and historical market returns that may not match what any individual retiree actually holds.

Taxes are another blind spot. Withdrawals from traditional pre-tax accounts such as 401(k)s and IRAs are treated as ordinary income by the IRS. A retiree pulling $40,000 per year from a traditional retirement account will owe federal income tax on that amount, with the actual bill depending on total taxable income, account type, and filing status. The result is that the real spending power of a $40,000 withdrawal is almost always less than $40,000, and those lost dollars are rarely factored into the original 4% calculation.

The Rule’s Own Creator Has Moved On

When Bengen, an MIT-educated financial planner, published his original 4% research in 1994, he built it around historical U.S. market data going back to 1926. His goal was to identify a withdrawal rate that would have survived every worst-case historical starting point, including the Great Depression and the stagflation of the 1970s. The result was 4.15%, rounded to 4%, which he called the SAFEMAX: the maximum safe historical withdrawal rate.

Thirty years later, Bengen has revisited the data with a broader set of asset classes, adding small-cap, mid-cap, and international stocks alongside bonds and cash. His August 2025 book, A Richer Retirement: Supercharging the 4% Rule to Spend More and Enjoy More (Wiley), presents 4.7% as the new SAFEMAX. Greater diversification across more asset classes lifted the floor for worst-case scenarios. Notably, Bengen now frames 4.7% as a worst-case floor, not a standard rate. His research found that many retirees may comfortably sustain withdrawals in the range of 5.25% to 5.5% without meaningfully raising the risk of running out of money, depending on market conditions at the time of retirement.

Despite Bengen’s own evolution on the number, the old figure persists throughout the financial planning industry. According to research from PGIM DC Solutions, roughly 61% of financial planners still advise clients to follow the traditional 4% withdrawal rule.

What Other Researchers Are Saying

Not everyone has moved in the same direction as Bengen. Morningstar takes a forward-looking approach to withdrawal rates rather than relying on historical data, using Monte Carlo simulations built around projected future returns and inflation. Its December 2025 “State of Retirement Income” report set 3.9% as the highest safe starting withdrawal rate for new retirees in 2026, targeting a 90% probability of having funds remaining after 30 years. That is an improvement from the 3.7% figure Morningstar published in 2024, but it still sits below the traditional 4% benchmark. The divergence between Bengen’s historically grounded 4.7% and Morningstar’s forward-looking 3.9% reflects genuine disagreement among researchers, not a settled answer.

Where Annuities and Social Security Fit In

One growing response to the limits of any fixed withdrawal formula is incorporating annuities into a retirement income plan. If a retiree with a $1 million portfolio redirected $333,000 into an annuity, the resulting guaranteed income stream could push total annual income to roughly $52,667, while still leaving $666,667 invested in the portfolio. That adds approximately $1,056 per month in predictable income beyond what the portfolio alone would generate, providing a buffer for unexpected expenses without forcing the portfolio to absorb every cost shock.

Social Security is the other major variable that the 4% rule ignores entirely. A retiree receiving Social Security benefits has a source of income that sits completely outside the portfolio calculation. In practice, that means the portfolio may not need to carry the full weight of living expenses, allowing the retiree to withdraw at a lower rate, let the principal compound further, and potentially extend the portfolio’s life well beyond the 30-year window the original rule was designed around.

Editor’s note: This article was updated to reflect William Bengen’s August 2025 book formally establishing 4.7% as the new worst-case SAFEMAX withdrawal rate, his additional suggestion that many retirees may safely withdraw 5.25% to 5.5%, and Morningstar’s December 2025 “State of Retirement Income” report recommending 3.9% as the safe starting withdrawal rate for new retirees in 2026. An unverifiable tax figure tied to Florida residency was also removed and replaced with a general discussion of how federal taxes reduce the real spending power of pre-tax account withdrawals.

Contact [email protected] for any questions or corrections.