Financial advisors have long relied on the 4% rule as a benchmark for scheduling retirement account withdrawals. The rule has since migrated well beyond professional planning circles. It is now a fixture in the F.I.R.E. (Financial Independence, Retire Early) lexicon, and many Millennials and even Gen Z members have built their early-retirement income projections around it.

A rigid attachment to the 4% rule, however, can quietly undermine some retirees’ financial security depending on the assets they hold, their age, Required Minimum Distribution (RMD) obligations, and how long their portfolio needs to last. The good news is that several well-tested modifications can adapt the rule to a much wider range of situations.

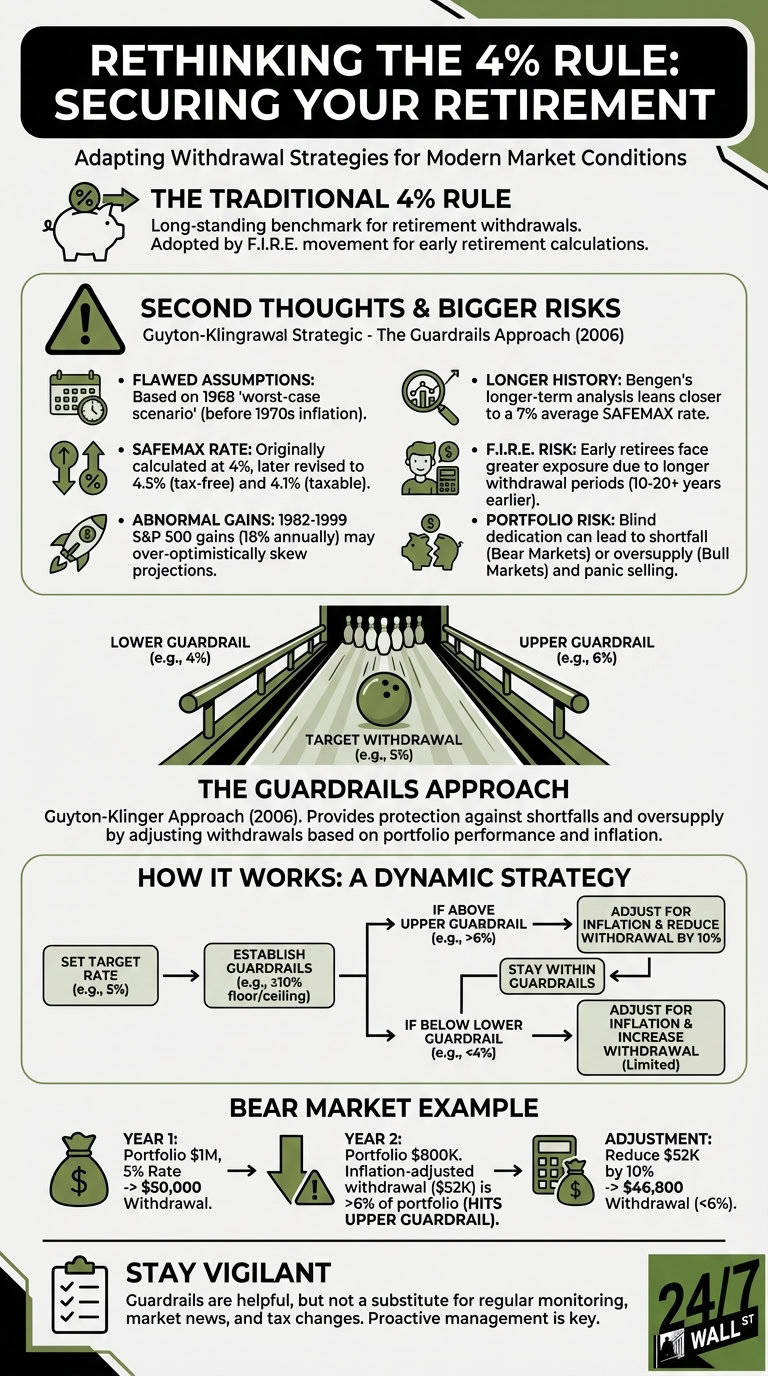

Second Thoughts and Bigger Risks

Bengen himself revisited his original analysis over time and acknowledged that several of its underlying assumptions were imperfect. His core points of revision included:

- The 4% rule grew out of a worst-case scenario calibrated to retirees circa 1968. That cohort went on to face a punishing combination of prolonged bear-market returns and double-digit inflation and interest rates through the 1970s, none of which was visible at the time the rule was set.

- The 4% rate was always Bengen’s SAFEMAX figure, meaning the absolute worst-case maximum safe withdrawal. In his 2025 book A Richer Retirement, Bengen updated the Universal SAFEMAX to 4.7%, reflecting a broader seven-asset-class portfolio (55% stocks, 40% bonds, 5% cash) that includes small-cap and mid-cap equities alongside large-cap stocks and government bonds.

- The S&P 500’s consistently above-average annual gains across most of the 1980s and 1990s were historically exceptional and can produce over-optimistic long-term projections if treated as a baseline.

- Looking across all historical retirement cohorts in his updated research, Bengen found the average SAFEMAX across 349 simulated retirees ran closer to 7%, once favorable market sequences and lower inflation periods were factored in alongside the worst-case scenarios.

Researchers at Morningstar have approached the same question using forward-looking return and inflation assumptions rather than historical averages. Their 2025 State of Retirement Income report placed the base-case safe starting withdrawal rate at 3.9% for a new retiree planning a 30-year horizon with a 90% probability of success, up slightly from 3.7% the prior year. That figure assumes a balanced portfolio weighted toward 30% to 50% equities and no supplemental income sources such as Social Security. Morningstar’s research also found that retirees willing to accept some year-to-year spending variability can start as high as nearly 6%.

One of the primary criticisms of the 4% rule is that blind adherence to it can leave a portfolio dangerously short during prolonged bear markets or with an uncomfortable surplus during sustained bull markets. Abnormally volatile stretches can also trigger panic selling that permanently locks in losses. F.I.R.E. adherents face compounded exposure because their portfolios must stretch across 40 or more years rather than the standard 30. Historical simulations of 45-year horizons show that the stagflation era of 1965 to 1969 is a more destructive sequence for fixed-rate strategies than the 1929 market crash, though adding guardrails to the spending plan has historically lifted success rates from roughly 83% to over 98%.

Customizing the Recipe With Guardrails

Bowling lanes for children have guard rails to prevent balls from falling into the gutter. The Guardrails Approach for retirement fund withdrawals serves a similar purpose for retirees’ protection.

Many bowling alleys designate specific lanes for children, equipping those lanes with guardrails along both sides to prevent balls from rolling into the gutter. The rails keep the ball heading toward the pins, improving the odds of success and making the game more rewarding. The Guyton-Klinger Guardrails Approach borrows that logic for retirement spending.

Jonathan Guyton and William Klinger introduced the framework in a 2006 paper in the Journal of Financial Planning. The strategy works within a target annual withdrawal range, typically somewhere between 4% and 7%, and applies automatic adjustments whenever spending drifts beyond either boundary. Those adjustments dramatically reduce the odds of both a painful shortfall and an unexpected surplus. Shortfalls are the more serious problem because they can threaten a retiree’s ability to cover basic necessities. An overage carries its own risks too, particularly if RMD obligations and tax bracket management require keeping income below a specific threshold and the excess pushes a larger tax bill.

A standard 20% guardrails setup illustrates how the mechanics work. With a 5% target withdrawal rate, the lower guardrail sits at 4% and the upper at 6%. The retiree targets that 5% rate each year, adjusting the dollar withdrawal for inflation. If performance shifts the withdrawal rate outside the corridor, the spending amount gets a 10% trim (at the upper guardrail) or a 10% boost (at the lower guardrail) to pull it back in range.

A bear-market scenario makes the adjustment concrete. In Year 1, the portfolio stands at $1 million and the 5% rate produces a $50,000 withdrawal. In Year 2, a market downturn drops the portfolio to $800,000. Applying a 4% inflation adjustment to last year’s withdrawal produces a scheduled draw of $52,000, which would represent more than 6% of the shrunken portfolio and trip the upper guardrail. Reducing that inflation-adjusted amount by 10% brings the actual withdrawal to $46,800, pulling the rate back below 6% and protecting the portfolio’s long-term runway.

One practical nuance is that a guardrail-triggered reduction does not automatically require an equivalent cut in lifestyle spending. With a traditional IRA or 401(k), a lower withdrawal also reduces the taxable income that year, which can partially offset the dollar impact of the adjustment.

A Meaningful Limitation Worth Knowing

The Guyton-Klinger approach is not without critics. Research published on Kitces.com by financial planning researchers Justin Fitzpatrick and Derek Tharp found that classic Guyton-Klinger guardrails can force severe income cuts during sustained downturns. Their analysis showed that in a worst-case scenario, a retiree could see income fall as much as 66% below the original withdrawal amount. For a retiree starting at a 5.3% initial rate, they found a 10% chance of a 48% income reduction within 10 years and as large as an 84% reduction within 30 years. The underlying issue is that the framework adjusts spending based solely on the ratio of withdrawals to the current portfolio value rather than on a comprehensive probability-of-success assessment, which can cause it to overcorrect during normal market cycles.

The Shift to Risk-Based Dollar Guardrails

Modern financial planning software has moved beyond the classic Guyton-Klinger percentage triggers toward risk-based guardrails. Rather than adjusting spending when an absolute withdrawal-rate ratio crosses a threshold, this newer approach continuously evaluates the ongoing probability that a retirement plan will succeed over its full lifetime horizon. It translates probability thresholds into real dollar amounts, defining clear spending corridors that expand or contract based on the actual health of the portfolio. The practical advantage is substantial flexibility for multi-phase retirements where spending patterns change across lifestyle stages or where the timing of Social Security benefits creates gaps in income early in retirement.

The Psychological Cost of Overcorrection

Standard financial planning models often ignore an underappreciated cost of rigid spending cuts: the emotional and psychological burden on the retiree. Monte Carlo simulations typically count it as a success whenever a retiree preserves substantial principal by aggressively trimming lifestyle expenses, but that framing misses the human side of the outcome. Cutting spending in response to normal short-term market volatility can mean unnecessary deprivation during years when a retiree is still healthy and active, years that cannot be recovered later. A well-calibrated guardrails system protects capital while keeping the spending corridor wide enough that retirees are not forced to live persistently below their actual means.

The Guardrails Approach is a useful and flexible tool, but it does not eliminate the need for regular portfolio reviews, ongoing attention to legislative changes affecting tax treatment, or proactive planning around RMD schedules. Dynamic withdrawal strategies perform best when they are revisited annually and adjusted to reflect both portfolio performance and any changes in the retiree’s personal circumstances.

Editor’s note: This update adds Morningstar’s 2025 safe withdrawal rate guidance (3.9% base case for a 30-year horizon with 90% probability of success), corrects the timeline for Bengen’s SAFEMAX revision to 4.7% as stemming from his 2025 book A Richer Retirement rather than a 2012 statement, adds the Kitces/Fitzpatrick-Tharp research on the income-reduction risks of classic Guyton-Klinger guardrails, and updates the characterization of S&P 500 1980s-1990s returns.

Contact [email protected] for any questions or corrections.