Palo Alto Networks (NASDAQ:PANW | PANW Price Prediction) had a volatile week, climbing 4.79% to close Friday at $166.95 after starting the week at $159.32. The stock remains down 9.36% year-to-date and 17.3% below year-ago levels.

Let’s dive into three storylines that drove the action.

The Stock Bounced While the Market Sagged

Palo Alto Networks outperformed both the broader market and cybersecurity peers this week. The S&P 500 dropped 1.29% while the ETFMG Prime Cyber Security ETF (NYSEARCA:HACK) gained 3.51%.

The stock opened Friday at $165.03, hit an intraday high of $170.49, and closed at $166.95. That’s well below the $222.97 average analyst price target, implying roughly 33% upside.

The $25 Billion CyberArk Deal Just Closed

On February 11, Palo Alto completed its $25 billion acquisition of CyberArk Software, the second-largest acquisition of an Israeli company ever. CyberArk shareholders received $45 cash plus 2.2005 PANW shares per share. The company announced plans for a secondary listing on the Tel Aviv Stock Exchange under the CYBR ticker.

Identity security is the new perimeter in a world where everything from humans to machines to AI agents needs authentication. CyberArk’s Identity Security Platform slots directly into PANW’s platformization strategy alongside Strata, Prisma, and Cortex. CEO Nikesh Arora has been consolidating point solutions into unified platforms, and this deal puts identity at the center.

The acquisition follows PANW’s $3.35 billion purchase of Chronosphere in January 2026, which added cloud-native observability capabilities. Two massive deals in two months signals aggressive expansion into adjacent markets where AI-era threats demand integrated defenses.

Earnings Tuesday Could Reset Expectations

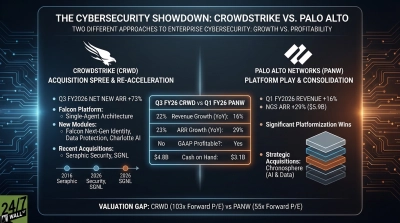

Palo Alto reports Q2 fiscal 2026 earnings on February 17. Wall Street expects $0.94 EPS on $2.58 billion in revenue, representing 16% EPS growth and 14.15% revenue growth year-over-year. Last quarter, the company beat on all metrics and grew Next-Gen Security ARR 29% to $5.9 billion.

Analyst sentiment is mixed. Jefferies maintains a $250 price target and sees CyberArk driving upside, while Stifel cut its target from $225 to $200 on concerns about reseller feedback and organic growth. JPMorgan trimmed from $235 to $225 but kept its Overweight rating. The consensus of 12 Strong Buy, 30 Buy, 11 Hold, and 2 Sell ratings suggests confidence, but downgrades reflect uncertainty about whether PANW can sustain growth while integrating two massive acquisitions.

Once again, the average price target for Palo Alto stands at $224.42, which suggests upside. Palo Alto has been selling off alongside the broader software category, but sentiment can shift quickly. It wouldn’t surprise me if security incidents throughout 2026 as agent use explodes will lead to investors seek out the security space as an investment opportunity rather than selling it off alongside software stocks.

AI Security Is the Battlefield

Palo Alto Networks is betting traditional rule-based security tools can’t handle non-deterministic AI threats. The company’s pushing “Agentic Remediation” and “Precision AI” as the future of autonomous security operations, and its Prisma AIRS platform aims to secure AI ecosystems end-to-end.

Gartner predicts 50% of organizations will adopt zero-trust data governance by 2028 due to AI-generated data risks. PANW’s platformization strategy, now turbocharged by CyberArk’s identity capabilities, positions it to capture that shift. But competitors like Fortinet (NASDAQ:FTNT) and Zscaler (NASDAQ:ZS) are pouring resources into AI-driven security too.

Fortinet reported earnings on February 5th and absolutely smoked expectations, delivering adjusted EPS of $.81 versus expectations of $.74. Thanks to that beat, shares are now up year-to-date while most software stocks sell off.

Can Palo Alto repeat Fortinet’s performance? We’ll see when the company reports after the bell on Tuesday.

Contact [email protected] for any questions or corrections.