Rivian (NASDAQ:RIVN | RIVN Price Prediction) has proven to be a disappointing investment since its initial public offering in November 2021 at $78 per share. The stock closed yesterday at $14, reflecting an 82% decline from its IPO price and an 87% drop from its opening day high of $106.75. Over nearly every time frame, it has delivered losses: down 29% year-to-date in 2026, down 3% over the past year, and down 85% over three years.

However, the automaker’s Q4 and full-year 2025 earnings report yesterday marked a milestone: Rivian recorded its first annual consolidated gross profit of $144 million, an improvement of more than $1.3 billion from 2024, that was driven by cost reductions and software revenue. This shift means Rivian is no longer posting overall gross losses, though automotive-specific gross profit remained negative at $432 million for the year. That indicates it is still losing money on every car it sells, but the stock is soaring 20% in morning trading, Does that mean Rivian finally worth buying?

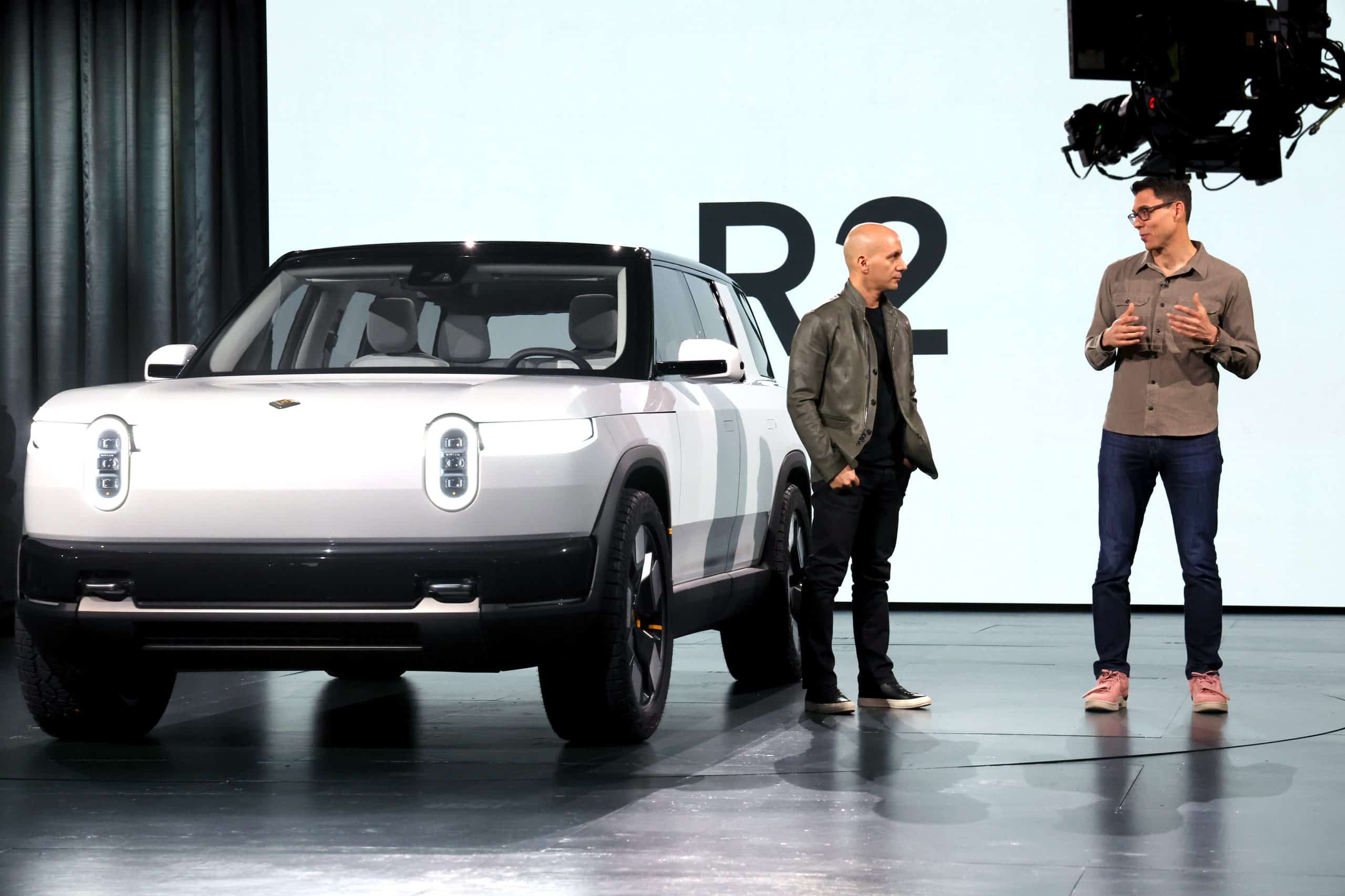

Betting Big on the R2 SUV

Rivian is staking its recovery on the upcoming R2 midsize SUV, with customer deliveries set to begin in the second quarter of 2026. Priced starting at around $45,000, the R2 targets a broader market than Rivian’s existing R1T pickup and R1S SUV, which start at $69,900 and $74,900, respectively. The company plans to launch a dual-motor all-wheel-drive version first — with options for single-motor and tri-motor configurations — offering over 650 horsepower and more than 300 miles of range in higher trims.

Rivian expects the R2 to drive a 47% to 59% increase in total deliveries to 62,000 to 67,000 vehicles in 2026, up from 42,247 in 2025. Full specifications, including exact pricing and trims, will be revealed on March 12, at SXSW.

Has the EV Window Closed?

The R2’s lower price point could appeal to cost-conscious buyers, positioning it as a competitor to Tesla‘s (NASDAQ:TSLA) Model Y. However, Rivian may have missed its optimal launch timing as the EV market has considerably cooled. Global EV sales fell 3% year-over-year in January 2026 to 1.2 million units, with North America down 33% and China down 20%.

In the U.S., EV sales are projected to hover around 1.2 million units for the year, reflecting a slowdown after the expiration of the $7,500 federal tax credit in September 2025. Overall new-vehicle sales are forecasted at 15.8 million units, a 2.4% decline from 2025, due to economic headwinds, high prices, and policy uncertainties like tariffs and USMCA renegotiations. Market share for EVs also dropped to 6.6% in January, down from prior levels, as consumers shift toward internal combustion and hybrid options.

While the R2’s affordability might carve out demand, Rivian faces significant uncertainty until it demonstrates sustained sales growth in this weakened environment.

Suddenly, an AI Chip Maker

Rivian has also ventured into AI hardware with its in-house Rivian Autonomy Processor (RAP1) chip, debuting on the R2 to power advanced driver-assistance and autonomy features. Built on a 5 nanometer process in collaboration with Arm Holdings (NASDAQ:ARM) and fabricated by Taiwan Semiconductor Manufacturing (NYSE:TSM), the RAP1 replaces Nvidia (NASDAQ:NVDA) processors and offers 2.5 times better performance per watt and processing 5 billion pixels per second for AI tasks like sensor fusion and neural networks. This supports Rivian’s push toward Level 4 autonomy, including LiDAR integration and point-to-point self-driving capabilities by the end of the year.

Key Takeaway

Rivian’s achievement of a $144 million consolidated gross profit in 2025 is a positive step, but the company continues to burn cash, posting a $3.6 billion net loss for the year and an adjusted EBITDA loss guidance of $1.8 billion to $2.1 billion for 2026. Automotive gross profit was still negative at $432 million in 2025, and management forecasts pressure on this metric in the first half of 2026 due to the R2 production ramp-up, with improvement expected toward year-end and eventual positive automotive and R2 gross profits.

This means a temporary return to gross losses on vehicle sales. With ongoing net losses, high capital expenditures of $1.95 billion to $2.05 billion, and a challenging EV market, Rivian remains a high-risk stock not worth buying today.

Contact [email protected] for any questions or corrections.