Live: Will Cadence Design Systems (CDNS) Beat Q4 Earnings Tonight?

Live Updates

Earnings Scorecard

Overall Grade: A-

Cadence delivered a strong finish to 2025 with execution across most key metrics, though revenue fell slightly short. The $1.99 EPS beat and robust FY26 guidance of $5.9B–$6.0B revenue drove the 7% after-hours surge—a meaningful reversal after the stock fell 10.3% over the past month.

| Category | Grade | Notes |

|---|---|---|

| Revenue Performance | B+ | Q4 revenue $1.44B missed estimates but grew 6.2% YoY; FY25 up 14% |

| Earnings Beat/Miss | A | EPS beat by 2%, extending 6-quarter beat streak |

| Guidance Quality | A | FY26 outlook implies 11–13% growth; record $7.8B backlog |

| Margin Trends | A- | Q4 non-GAAP operating margin 45.8%, stable vs guidance |

| Cash Flow | A+ | Operating cash flow $1.73B, up 37% YoY |

| Management Confidence | A | Repurchased $925M shares; planning ~50% of FCF for buybacks in FY26 |

What Changed This Quarter

-

Backlog stepped higher (now $7.8B vs the ~$7.0B record level you referenced pre-print), reinforcing durability.

-

Margins stayed firm: Q4 non-GAAP op margin essentially flat YoY, while FY25 margin expanded meaningfully.

-

Guidance clarity improved: FY26 outlook presented cleanly and explicitly excludes Hexagon, reducing modeling noise tonight.

Cadence Design Systems Up 4.88% After Earnings

Cadence proved the AI design cycle is still in full force — and it’s converting into both growth and margins.

Revenue accelerated, EPS beat, margins held near peak levels, and backlog climbed to a new record. That combination matters more than any single metric. Investors were worried that hardware mix could pressure profitability or that AI enthusiasm might be peaking. Instead, Cadence delivered operating leverage and reinforced visibility into 2026.

The most important signal was not the Q4 beat — it was the clean FY26 setup. Revenue approaching $6 billion with mid-40% non-GAAP margins tells you the model remains structurally strong. And by excluding Hexagon from guidance, management avoided adding noise to what was otherwise a clear growth story.

The stock was weak into the print because the market was recalibrating expectations for the entire EDA space.

Key Operating Highlights

| KPI | Latest | What it signals |

|---|---|---|

| Backlog | $7.8B (record) | Visibility remains a major pillar of the bull case |

| RPO expected to be recognized next 12 months | $3.8B | Near-term revenue support looks solid |

| Q4 Non-GAAP Op Margin | 45.8% | Margins held despite mix concerns |

| FY25 Non-GAAP Op Margin | 44.6% (up vs 2024) | Operating leverage remains intact |

-

Core EDA +13% (FY25) driven by hyperscaler adoption and AI-driven product proliferation.

-

Hardware: another record year, 30+ new customers, with “7 of top 10” buying both Palladium Z3 and Protium X3 — supports the “AI infrastructure buildout” narrative.

-

IP: grew ~25% YoY in 2025 (HBM/UCIe/PCIe/DDR/SerDes), which matters because IP is a key attach lever as advanced packaging ramps.

-

System Design & Analysis +13%, helped by 3D-IC and simulation demand for AI/HPC.

Management Commentary

Two quotes frame the quarter the way investors want to hear it:

-

CEO Anirudh Devgan: “Strong customer demand for our expanding AI-driven product portfolio… positions us well to capture the massive opportunities in the AI era.”

-

CFO John Wall: “With strong Q4 bookings, we began 2026 with a record backlog of $7.8 billion and excellent momentum.”

Translation: they’re leaning hard into (1) AI-driven product differentiation and (2) bookings/backlog visibility as the foundation for FY26.

Guidance Update

A big part of the huge after-hours jump comes from future guidance.

Cadence’s FY26 outlook:

| FY26 Guide | Company Outlook |

|---|---|

| Revenue | $5.9B–$6.0B |

| Non-GAAP Op Margin | 44.75%–45.75% |

| Non-GAAP EPS | $8.05–$8.15 |

| GAAP Op Margin | 31.75%–32.75% |

Guidance excludes the pending Hexagon D&E acquisition impact, keeping the core trajectory clean and easier to underwrite.

Huge Pop After Earnings Release

Cadence delivered the clean “beat plus guide” combo investors were looking for, and the stock is responding accordingly.

The stock immediately up 7% after-hours.

| Metric | Reported | Consensus | Beat/Miss |

|---|---|---|---|

| Q4 Revenue | $1.440B | $1.42B | ✅ Beat |

| Q4 Non-GAAP EPS | $1.99 | $1.91 | ✅ Beat |

| FY25 Revenue | $5.297B | $5.28B | ✅ Beat |

| FY25 Non-GAAP EPS | $7.14 | $7.04 | ✅ Beat |

Why the stock is up: this wasn’t just a modest Q4 beat — Cadence paired it with strong FY26 guidance and reinforced visibility with record backlog.

Earnings Snapshot

Cadence Design Systems (NASDAQ: CDNS | CDNS Price Prediction) reports fourth-quarter 2025 results tonight after the bell. After three consecutive quarters of accelerating momentum, investors are watching whether the EDA software leader can maintain its streak and deliver credible guidance for 2026.

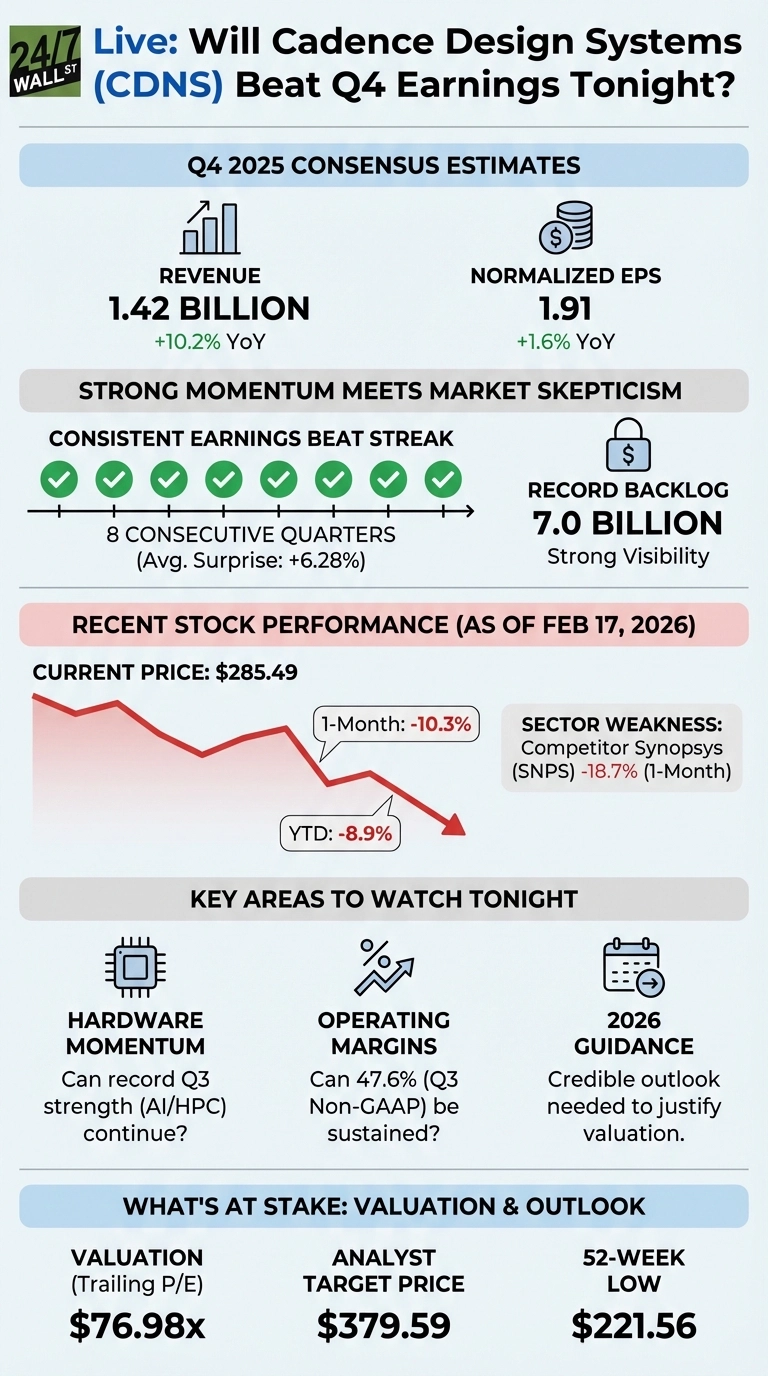

Strong Momentum Meets Market Skepticism

Cadence enters tonight’s report with a solid track record. The company has beaten earnings estimates for eight consecutive quarters, averaging a 6.28% surprise over that period. Last quarter delivered particularly strong results: revenue of $1.34 billion beat expectations by $16 million, while non-GAAP EPS of $1.93 topped consensus by $0.14.

But the stock tells a different story. Shares have dropped 10.3% over the past month and are down 8.9% year-to-date to $285.49. That decline mirrors broader EDA sector weakness: competitor Synopsys has fallen 18.7% over the same month and is down 10.7% year-to-date. The parallel moves suggest investors are recalibrating expectations for the entire design automation space, not just Cadence specifically.

Management raised full-year 2025 guidance last quarter to approximately 14% revenue growth, targeting $5.26 billion to $5.29 billion in revenue. The company also reported a record $7.0 billion backlog, providing strong visibility into future quarters. CEO Anirudh Devgan emphasized “ongoing broad-based strength” across the business.

Consensus Estimates

| Metric | Q4 2025 Estimate | YoY Growth | FY 2025 Estimate | YoY Growth |

|---|---|---|---|---|

| Revenue | $1.42 billion | +10.2% | $5.28 billion | +14.0% |

| Normalized EPS | $1.91 | +1.6% | $7.04 | +17.9% |

Hardware Strength and Margin Discipline

I’ll be watching two areas closely tonight. First, whether the hardware segment can sustain its recent performance. Cadence reported record third-quarter hardware results driven by expansions at AI and HPC customers. That momentum matters because hardware typically carries lower margins than software, and investors need to see that growth translating into profitability.

Which brings me to the second focus: operating margins. Last quarter’s 47.6% non-GAAP operating margin demonstrated pricing power, but the question is whether that level is sustainable as the business mix shifts. Management guided full-year non-GAAP operating margins to 27.9% to 28.9% on a GAAP basis. You should look at whether Q4 margins come in at the high end of that range or if there’s compression from hardware mix.

Cash generation also deserves attention. Third-quarter operating cash flow surged 187% year-over-year to $1.18 billion, an exceptional result that likely included timing benefits from collections. I’ll be looking at whether Q4 shows similarly strong cash conversion or if that was a one-time boost.

The company completed its acquisition of Arm’s Artisan foundation IP business and announced plans to acquire Hexagon’s design and engineering division. Management commentary on integration progress and the strategic rationale will matter for 2026 modeling.

Guidance Will Set the Tone for 2026

Tonight’s real test isn’t Q4 results. It’s whether management can articulate a credible 2026 outlook that justifies the current 76x trailing PE ratio and 38x forward PE. Analysts have a $379.59 average price target, implying 33% upside from current levels, but that assumes continued double-digit growth and margin expansion.

The stock’s recent weakness alongside Synopsys suggests the market is questioning whether AI-driven design tool demand can sustain current growth rates. Cadence needs to show that its $7.0 billion backlog converts into predictable revenue and that new customer wins are replacing any slowdown in existing accounts. If guidance disappoints or management sounds cautious about first-half 2026 linearity, the stock could test recent lows near $221.56. But if they deliver confidence backed by specific customer traction, this could be where sentiment starts to turn.

Contact [email protected] for any questions or corrections.

Joel South covers large-cap stocks, dividend investing, and major market trends, with a focus on earnings analysis, valuation, and turning complex data into actionable insights for investors.

He brings more than 15 years of experience as an investor and financial journalist, including 12 years at The Motley Fool, where he served as an investment analyst, Bureau Chief, and later led the Fool.com investing news desk. He has also co-hosted an investing podcast and appeared across TV and radio discussing market trends.

© 24/7 Wall St.