Many retirees find Social Security covers essentials but not much more. Rising costs create steady pressure, and while benefits received a 2.8% cost-of-living adjustment for 2026, healthcare expenses have climbed well ahead of the general price level for years. That financial squeeze explains why people who claimed benefits early often continue working to supplement income, even though doing so triggers withholding rules they never anticipated.

Social Security does not prohibit working while collecting benefits. It temporarily reduces what recipients receive if earnings exceed certain thresholds before full retirement age. The withheld money does not disappear, but understanding how the mechanics work matters, because the penalty arrives fast and hits hard.

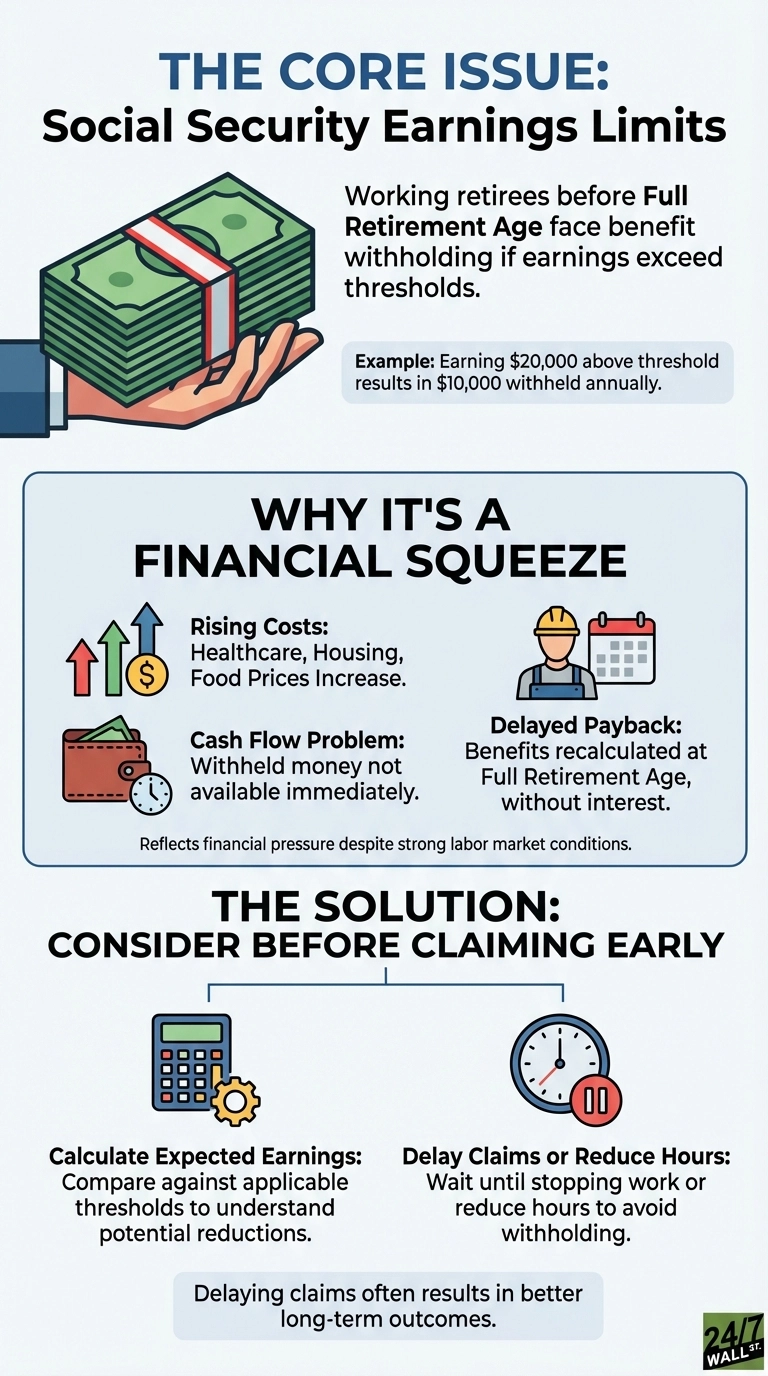

How the Earnings Limit Works

The Social Security Administration sets an annual earnings cap for those collecting benefits before full retirement age. For 2026, that threshold is $24,480 for anyone who remains under full retirement age the entire year, up from $23,400 in 2025. The cap sits surprisingly low, roughly equivalent to part-time work at about $12 an hour over a standard schedule. Above that level, Social Security deducts $1 for every $2 earned. For retirees who assumed part-time work would supplement their benefits without consequence, the result is an unexpected financial squeeze at a time when fixed incomes are already struggling to keep pace with rising costs.

Consider a 64-year-old working part-time who earns $20,000 above the threshold. Social Security withholds $10,000 annually, which works out to roughly $833 per month in lost income. With the average retired worker collecting about $2,081 per month in 2026, that shortfall represents close to five months of a typical benefit payment. The cash flow problem hits hardest for someone who claimed early precisely because they needed income right away, rather than years later when the government eventually recalculates benefits upward.

The rules ease as workers approach full retirement age. A separate, more generous threshold applies in the year someone reaches full retirement age: for 2026, earnings up to $65,160 are permitted before any withholding begins, and even then only $1 is deducted for every $3 earned above that limit, covering only the months prior to the birthday month. Once full retirement age arrives, all earnings restrictions disappear entirely.

The Money Comes Back, Eventually

Withheld benefits are not lost permanently. Once someone reaches full retirement age, the Social Security Administration recalculates the monthly payment to credit the months when benefits were reduced or not received due to the earnings test. The monthly benefit rises slightly to compensate over time. That adjustment is gradual, though, and it carries no interest or inflation protection for the years when that income was unavailable.

For someone who needs money now to cover rising costs, waiting years to recover withheld benefits offers little comfort. The tension between immediate financial needs and long-term benefit optimization forces working retirees into difficult tradeoffs: accept substantial benefit withholding in the near term, or reduce work hours to preserve monthly payments. Neither choice is straightforward when bills arrive monthly but benefit recalculations happen years later.

The issue has drawn fresh attention on Capitol Hill. On March 24, 2026, Sen. Rick Scott introduced the Senior Citizens’ Freedom to Work Act in the Senate, with Sen. Tommy Tuberville joining as a cosponsor. Rep. Greg Murphy introduced companion legislation in the House on April 16, 2026. The bill would repeal the retirement earnings test entirely, a provision that has been on the books since 1935, when policymakers designed it to push older Americans out of the workforce and free up jobs for younger workers during the Great Depression. Proponents argue the test now discourages older Americans from remaining in the workforce at a time when workers aged 55 and over are the fastest-growing segment of the labor force. As of mid-2026, the Senate version had been referred to the Committee on Finance and the House version to the Committee on Ways and Means, and both bills remain in their respective committees.

What to Consider Before Claiming Early

Financial advisors typically recommend that anyone considering claiming Social Security before full retirement age while continuing to work should first calculate expected earnings against the applicable annual threshold. Understanding the potential benefit reductions before they arrive prevents unpleasant surprises. Delaying the claim until work stops, or reducing hours enough to stay below the cap, often produces better cash-flow outcomes for those who have that flexibility.

The decision grows more complicated when health concerns or family circumstances make an early claim unavoidable. In those situations, understanding the withholding mechanics at least prevents surprises when benefit checks arrive smaller than expected. Every situation differs, and factors such as exact full retirement age, annual income level, and other household resources can shift the outcome considerably. Notably, income from pensions, annuities, investments, or veterans benefits does not count toward the earnings test, a distinction that matters greatly for retirees drawing from multiple income sources.

Editor’s note: This article corrects a prior editor’s note that misidentified the committee referrals for the Senior Citizens’ Freedom to Work Act. The Senate bill (S.4184) was referred to the Committee on Finance, and the House bill (H.R.8344) was referred to the Committee on Ways and Means. The article also adds that Sen. Tommy Tuberville is a cosponsor of the Senate version, and reflects that the earnings test has been law since 1935.

Contact [email protected] for any questions or corrections.