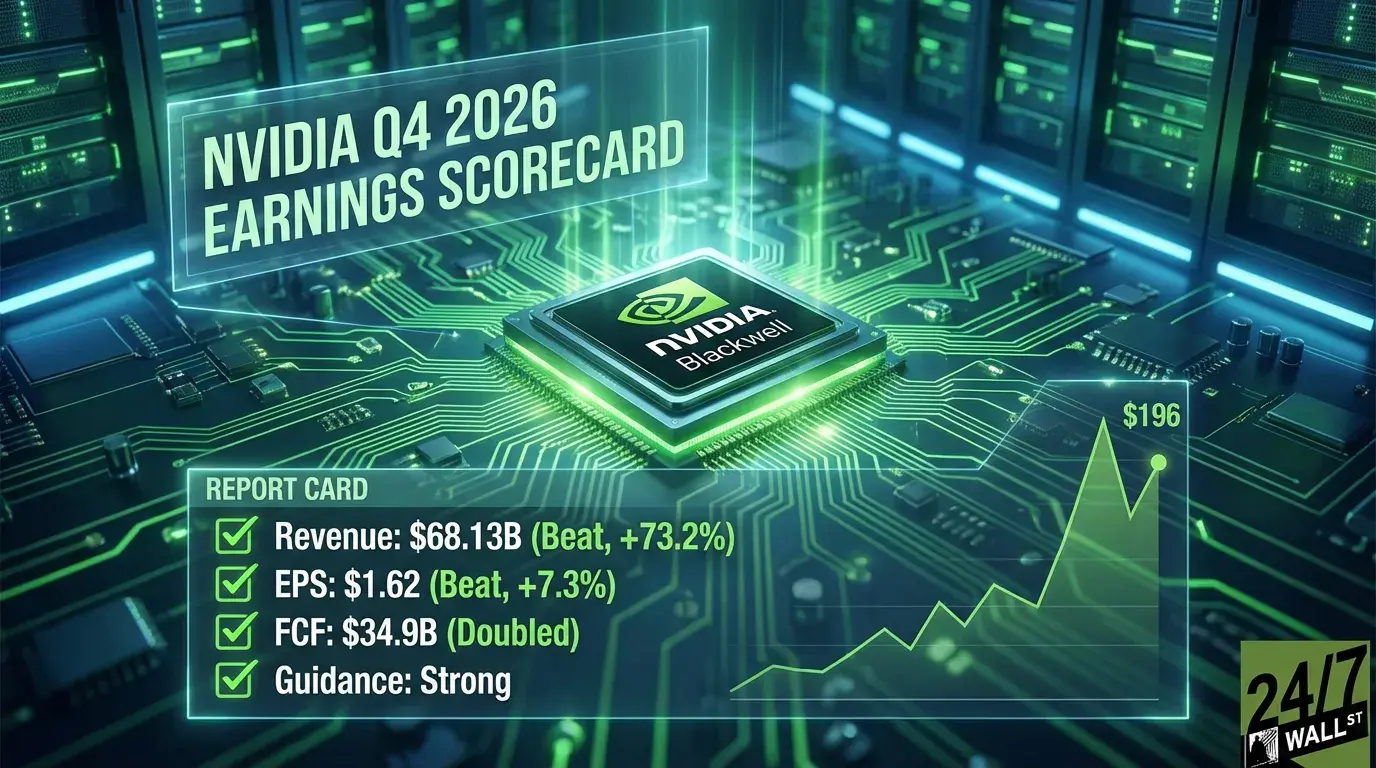

NVIDIA’s fiscal Q4 2026 results cleared the bar Wall Street had set, with revenue of $68.13 billion beating the $66.19 billion consensus and non-GAAP EPS of $1.62 topping the $1.51 estimate by 7.3%. Despite the beat, shares pulled back modestly after the report, trading near $196 the following morning after closing at $199.80 at the time of filing. The muted reaction reflects a market that expected a strong quarter and got one, but is now scrutinizing what comes next.

Q4 FY2026 Earnings Scorecard

| Category | Grade | Key Insight |

|---|---|---|

| Revenue Performance | A | $68.13B in revenue grew 73.2% year over year, topping estimates by nearly $2B and surpassing the prior quarter’s $57B with ease. |

| Earnings Beat/Miss | A- | EPS of $1.62 beat the $1.51 consensus, marking four consecutive quarters of EPS beats with each beat larger than the last. |

| Forward Guidance | B+ | Q1 FY2027 guidance of $78B (+/-2%) implies roughly 14.5% sequential growth, but explicitly excludes any Data Center compute revenue from China due to export restrictions. |

| Profit Margins | A- | Non-GAAP gross margin reached 75.2% in Q4, recovering from the product transition pressure that weighed on the full-year FY2026 non-GAAP gross margin of 71.3%, down 4.2 percentage points year over year. |

| Cash Generation | A+ | Free cash flow of $34.9B more than doubled year over year (+124.4%), with full-year FCF reaching $96.58B on minimal capital expenditure requirements. |

| Management Tone | A | CEO Jensen Huang declared the age of “physical AI” has arrived, framing NVIDIA’s next growth phase around robotics, autonomous systems, and sovereign AI infrastructure — not just data center GPU sales. |

Where the Quarter Was Won: Data Center

NVIDIA’s Data Center segment remains the engine driving everything else. Q4 Data Center revenue came in at approximately $66.4 billion, accounting for the overwhelming majority of total company revenue. The segment’s growth is being driven by the Blackwell GPU architecture ramp — specifically the GB200 NVL72 rack-scale systems that hyperscalers including Microsoft, Amazon, Google, and Meta are deploying at scale to support next-generation AI training and inference workloads.

Jensen Huang described Blackwell’s ramp as “the fastest product ramp in our company’s history,” and the numbers support that claim. The transition from H100 to Blackwell happened at a speed that surprised even NVIDIA’s own supply chain partners, with CoWoS-L packaging capacity at TSMC representing one of the few genuine bottlenecks the company has faced in meeting demand.

The China Constraint

The one structural limitation embedded in NVIDIA’s otherwise clean beat is impossible to ignore: the Q1 FY2027 guidance of $78 billion explicitly excludes Data Center compute revenue from China. This is not a new development — H20 chip sales were described as “insignificant” by Q3 FY2026 following $4.5 billion in H20-related inventory charges earlier in the fiscal year — but its persistence as a guidance caveat is a reminder of the regulatory ceiling on NVIDIA’s total addressable revenue.

China was once a meaningful contributor to NVIDIA’s Data Center business. The export control regime that began tightening in late 2022 and accelerated through 2023 and 2024 has effectively removed that market from the near-term growth equation. The $78 billion guide is being delivered without it. That is both a testament to the strength of demand elsewhere and a clear signal of how much higher NVIDIA’s ceiling could be in a different geopolitical environment.

Gross Margin: Recovery in Progress

One area that deserves more attention than it typically gets: gross margins are in a transitional phase. The full-year FY2026 non-GAAP gross margin of 71.3% was down 4.2 percentage points year over year, reflecting the cost complexity of ramping Blackwell’s rack-scale systems. The GB200 NVL72 is a fundamentally different product from the H100 — it integrates GPUs, CPUs, high-bandwidth memory, and liquid cooling infrastructure into a single system, which carries meaningfully higher manufacturing and integration costs in early production.

The Q4 recovery to 75.2% non-GAAP gross margin is an encouraging sign that Blackwell unit economics are improving as volumes scale. Management has guided Q1 FY2027 gross margins to approximately 71%, suggesting another transitional quarter before the expected drift back toward the mid-70s. Investors who have modeled mid-70s margins through FY2027 should treat that as an aspiration rather than a certainty until the data confirms it.

Free Cash Flow: The Number That Doesn’t Get Enough Credit

NVIDIA generated $96.58 billion in free cash flow for the full fiscal year FY2026. To put that in context: that is more free cash flow than most S&P 500 companies generate in total revenue. The $34.9 billion in Q4 free cash flow alone represents a 124.4% year-over-year increase and it is being generated with capital expenditure requirements that remain modest relative to the revenue base, since NVIDIA designs chips but does not fabricate them.

That FCF machine is what funds the $50 billion share repurchase program NVIDIA has been executing, as well as the dividend. It also provides the financial flexibility to invest in software, systems integration, and the emerging physical AI stack that Huang outlined as the next chapter of growth.

What Jensen Huang Is Actually Saying

The management tone grade of A reflects something more than polished optimism. Huang’s framing on the earnings call was notably forward-leaning in ways that go beyond the typical guidance beat. His declaration that the age of “physical AI” has arrived — encompassing robotics, autonomous vehicles, industrial automation, and sovereign AI infrastructure — is a deliberate signal that NVIDIA’s addressable market is expanding, not plateauing.

The Rubin GPU architecture, succeeding Blackwell, represents the next compounding catalyst on the hardware roadmap. NVIDIA has not provided formal mass shipment timing for Rubin, but the implication from the product cadence is a late calendar 2026 introduction. If Rubin ramps with anywhere near the velocity of Blackwell, the FY2028 revenue trajectory becomes a very different conversation.

Contact [email protected] for any questions or corrections.