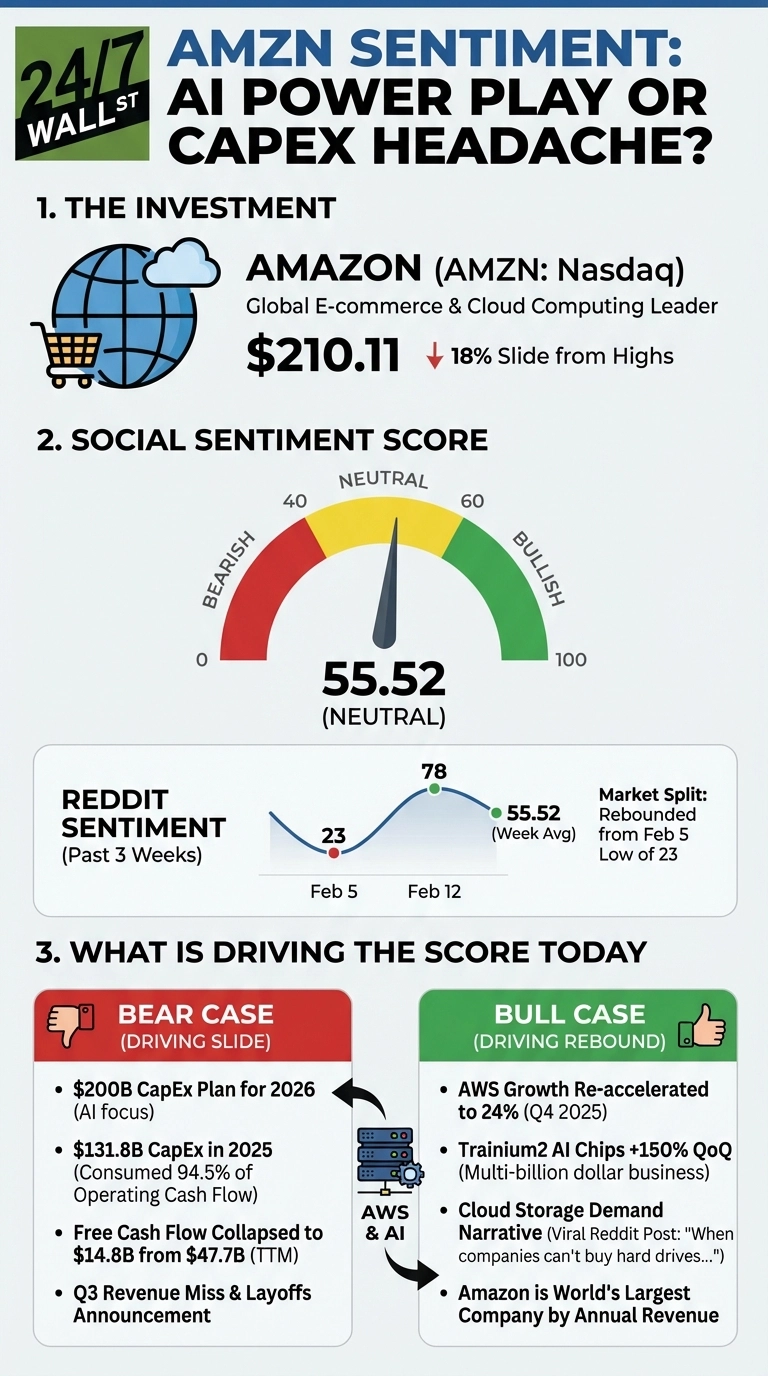

One of the magnificent seven, Amazon (NASDAQ:AMZN | AMZN Price Prediction) shares are currently sitting at $210.11 after shedding some valuation from previous highs. This slide occurred even as the company beat revenue expectations by $2.64 billion in Q3 2025 and came alongside management’s announcement of a $200 billion capital expenditure plan for 2026, almost entirely focused on AWS and AI infrastructure. As a result, retail investors are now split between two very different reads on the same company.

Reddit sentiment bottomed at a score of 23 on February 5 as post-earnings shock set in, then rebounded to 72 by February 18 as a bullish narrative took hold. The week’s average settled at a neutral 55.52: the market genuinely cannot make up its mind.

The CapEx Argument That Broke Reddit in Half

The bear case is concrete, albeit disappointing, as Amazon spent $131.8 billion in capital expenditures in 2025, consuming 94.5 cents of every dollar of operating cash flow. Trailing twelve-month free cash flow collapsed to $7.7 billion from $32.9 billion a year earlier. The layoffs announcement, which drew 3,150 upvotes and 455 comments on r/wallstreetbets, prompted one user to write: “Combined with AI-driven lay-offs. $AMZN”

The bulls came back fast, and the most viral recovery post, with over 2,000 upvotes, argued that hardware shortages funnel enterprise demand straight into AWS. The post’s author wrote: “When companies can’t buy hard drives, they’ll buy the next best thing (cloud storage)” — making the case that supply constraints on physical hardware are a direct tailwind for Amazon Web Services as enterprises shift spending to cloud infrastructure.

When companies can’t buy hard drives, they’ll buy the next best thing (cloud storage)

by u/wallstreetbets_user in wallstreetbets

Three data points driving the bull case:

- AWS re-accelerated to 20% growth in Q3 2025, the fastest since 2022, then posted 24% growth in Q4 at a $142 billion annualized run rate

- Amazon’s Trainium2 AI chips grew 150% quarter-over-quarter into a fully subscribed, multi-billion dollar business

- As of February 2026, Amazon has surpassed Walmart as the world’s largest company by annual revenue, with AWS generating a disproportionate share of operating profit despite representing roughly 20% of sales

Wall Street Sees $280, Prediction Markets See $210

Given all of the buzz around Amazon and AI bets, 41 of 44 analysts rate Amazon a Buy or Strong Buy, with a consensus price target of $279.59. For its part, Morgan Stanley carries a $300 target with an Overweight rating. Prediction markets disagree: Polymarket gives just 6.7% odds that Amazon will close above $220 by month-end.

CEO Andy Jassy called the $200 billion commitment “an extraordinarily unusual opportunity to forever change the size of AWS,” but offered no explicit financial guardrails when pressed. Whether that reads as visionary or reckless depends on which Reddit thread you found first.