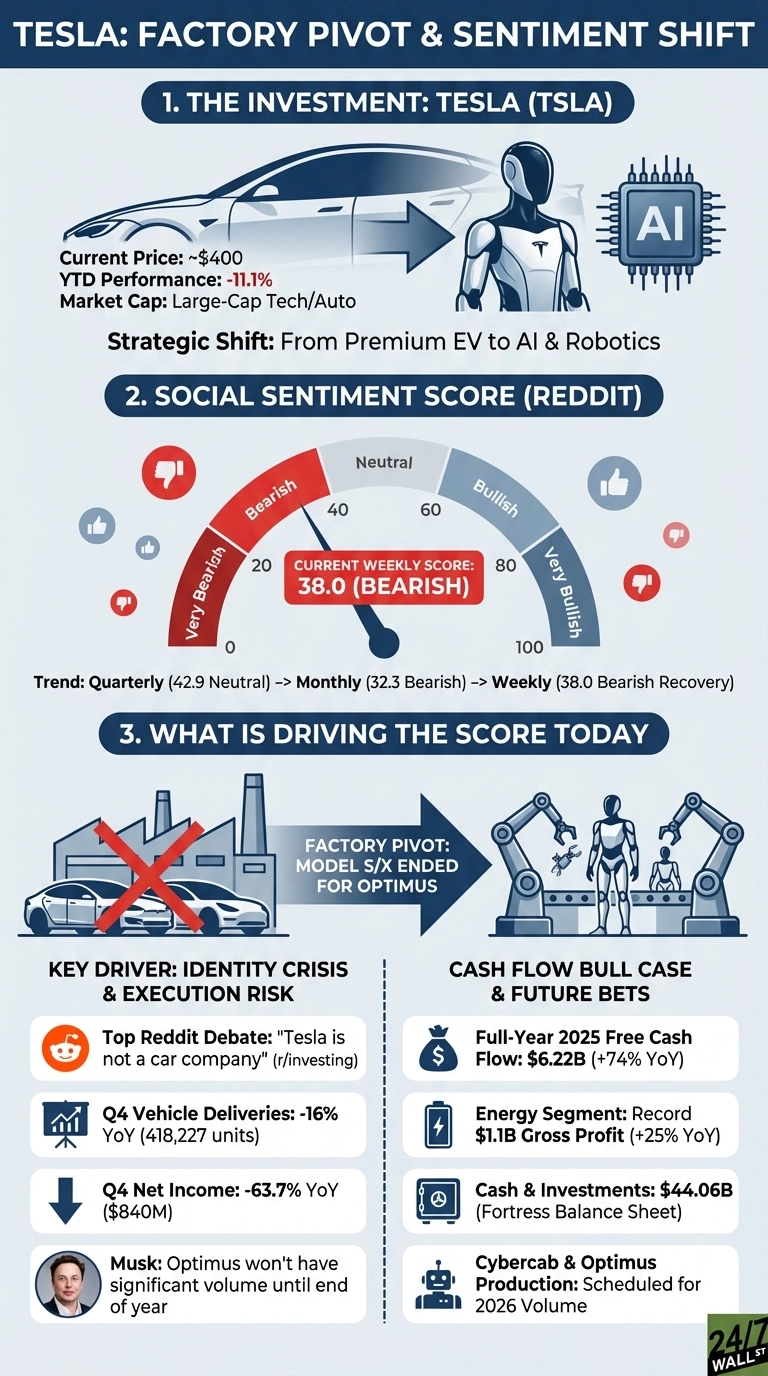

Still the big name in the EV world, Tesla (NASDAQ:TSLA | TSLA Price Prediction) shares are down roughly 10% year-to-date, trading near the $400 mark, as Reddit sentiment slid from a neutral quarterly average of 42.9 to a bearish 32.3 over the past month, with a modest recovery to 38.0 this week. The catalyst is straightforward: Tesla is winding down Model S and Model X production, converting that Fremont factory space into an Optimus robot manufacturing line.

On the most recent January earnings call, CEO Elon Musk was as direct as ever: “It’s time to bring the Model S and X programs to an end with an honorable discharge. We are going to take the Model S and X production space at our Fremont factory and convert that into an Optimus factory with a long-term goal of having a million units a year of Optimus robots.”

Tesla’s Identity Crisis Is Reddit’s Favorite Debate

The decision to end Model S and X production sparked immediate reaction on Reddit. On r/stocks, a post titled “Tesla to End Production of Model S, Model X vehicles to focus on Optimus” drew 2,010 upvotes and 510 comments:

Tesla to End Production of Model S, Model X vehicles to focus on Optimus

by in stocks

“Tesla to End Production of Model S, Model X vehicles to focus on Optimus” — r/stocks

The most engaged post driving current sentiment comes from r/investing, where user stone616 asked a pointed question in a thread titled “Tesla is not a car company”:

“Tesla is not a car company”

by u/stone616 in investing

“Tesla is not a car company” — u/stone616, r/investing

The post drew 455 upvotes and 284 comments, capturing the core tension: Tesla’s revenue still comes from cars, yet investors are pricing it as an AI and robotics platform. The numbers behind the skepticism:

- Q4 vehicle deliveries fell 16% year-over-year to 418,227 units; full-year 2025 automotive revenue declined 10%

- Net income dropped in Q4 to $840M, even as gross margins recovered to 20.1%

- Musk acknowledged Optimus won’t see “any kind of significant production volume until probably the end of this year”

The Cash Flow Case Bulls Are Making

Among the big takeaways from the earnings call that are making bulls eager are that full-year 2025 free cash flow hit $6.22B, up 74% year-over-year, even as revenue dipped. Cash and investments stand at $44.06B and CFO Vaibhav Taneja explained the funding approach: “We have over $44 billion of cash and investments on the books… anytime you have a consistent stream of cash flow, you can go and get money from the banks.” The energy segment posted a fifth consecutive record quarter of gross profit of $1.1B, up 25% year-over-year.

Always a heated discussion around its future, as of February 2026, 16 of 33 analysts rate Tesla a Buy or Strong Buy, with a 12-month consensus price target near $396. Helping drive this current analysis is that CyberCab production is expected to begin in April, all while Optimus volume production is targeted for late 2026. It’s safe to say that execution on either front will determine whether the identity debate shifts.

Contact [email protected] for any questions or corrections.