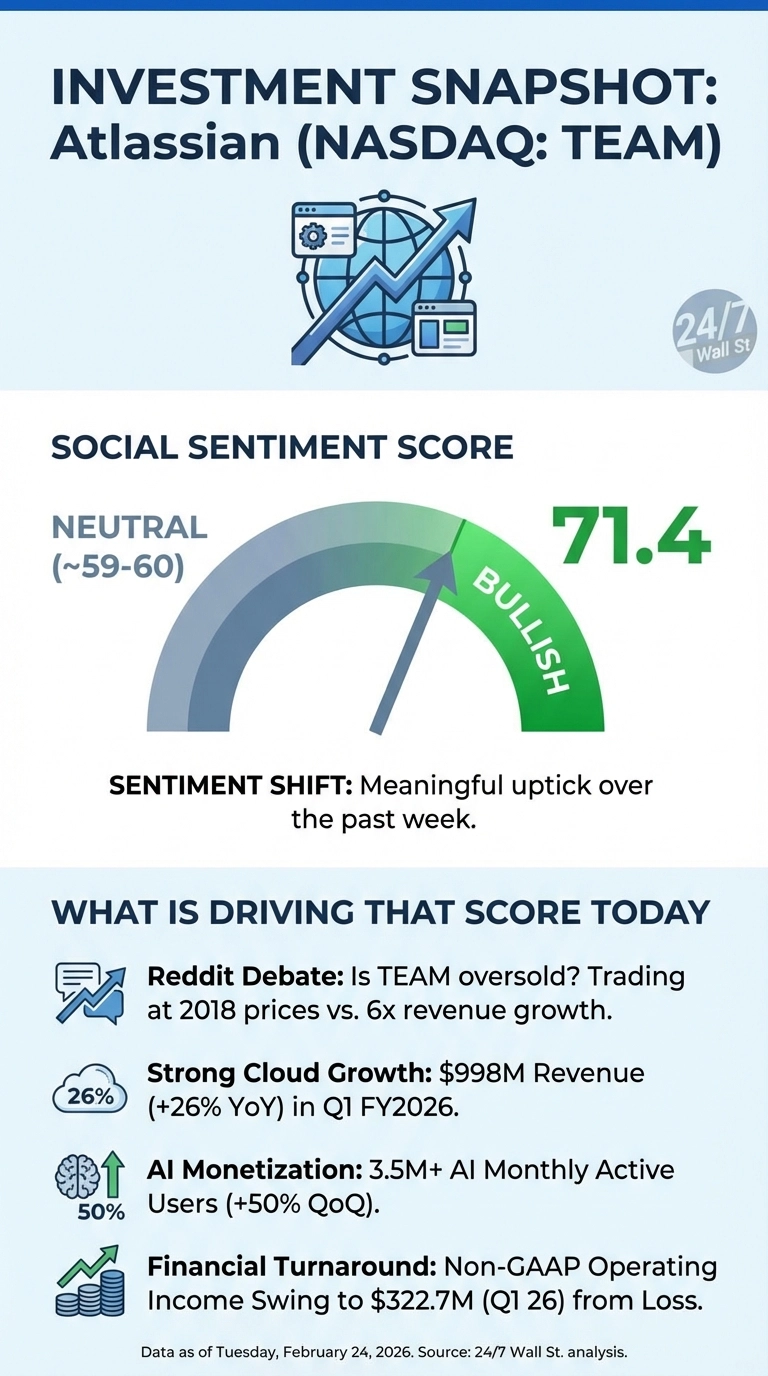

Widely known for its project management software, Atlassian (NASDAQ:TEAM) shares have collapsed 57.6% year-to-date and 75.9% over the past year, landing near 2018 price levels despite a business that looks nothing like it did eight years ago. That disconnect is driving Reddit sentiment from roughly 59 (neutral) to 71.4 (bullish) in a single week.

Strong Numbers, Falling Stock

Taking a closer look at the overall numbers, Q1 FY2026 revenue hit $1.432 billion, beating estimates by $30 million, while Non-GAAP EPS of $1.04 beat the analyst consensus by $0.20. One of the biggest staples for Atlassian, cloud revenue grew 26% year-over-year to $998 million, while AI monthly active users surpassed 3.5 million (up 50% quarter-over-quarter), and operating cash flow jumped 60% to $128.7 million. Positive numbers aside, Atlassian shares kept falling anyway, and it hasn’t been helped by a Citi downgrade on January 16, 2026, citing topline growth concerns, which sent the stock down 7.71% in a single session, followed by Pomerantz LLP securities investigation filings on multiple days between the end of January and late February.

Reddit Is Asking the Right Question

Atlassian stock, oversold?

by u/Monsjoex in investing

“This whole bear case is completely relying on massive layoffs for white collar workers that won’t get rehired in another role where they still need to use confluence/jira… these huge slow companies, governments etc that are all using atlassian software… would suddenly fire everyone [and] switch to some agentic created ai slop?” The post drew 48 upvotes and 66 comments with an 83% upvote ratio.

The bull case rests on three data points:

- Non-GAAP operating income swung from a $32 million loss in Q1 2025 to $322.7 million in Q1 2026, showing real leverage as cloud migration matures

- 25 of 33 covering analysts rate TEAM a Buy or Strong Buy, with a consensus price target of $206.42 against a current price near $70

- The seat-based pricing model embedded across 300,000+ enterprise and government customers creates switching costs that pure AI displacement narratives underestimate

The CFO Change and the Investigation Overhang

Among the big news related to Atlassian right now, the incoming CFO James Chuong, a former LinkedIn finance chief who helped scale that business to over 1 billion members and $18 billion in revenue, takes the role on March 30, 2026. As of now, the ongoing Pomerantz investigation centers on whether Atlassian adequately disclosed risks related to growth deceleration. The company projects $8.7 billion in revenue by 2028, requiring roughly 18.7% annual growth. Q2 cloud growth guidance of approximately 22.5% shows deceleration from Q1’s 26%, exactly the data point investigators will scrutinize. How Chuong frames the AI revenue story, and whether Atlassian deploys its $2.5 billion buyback authorization, will determine whether the stock can close the gap between its $68.81 price and the $177.85 analyst consensus.