One of the biggest names in the AI world right now, Taiwan Semiconductor Manufacturing (NYSE:TSM) just raised its annual dividend to at least TWD 23 per share in 2026, up from TWD 18 in 2025, a roughly 28% increase, while guiding for 38% revenue growth in Q1 2026. The question is whether the geopolitical risk hanging over Taiwan matters, which has been an ongoing question given the political climate.

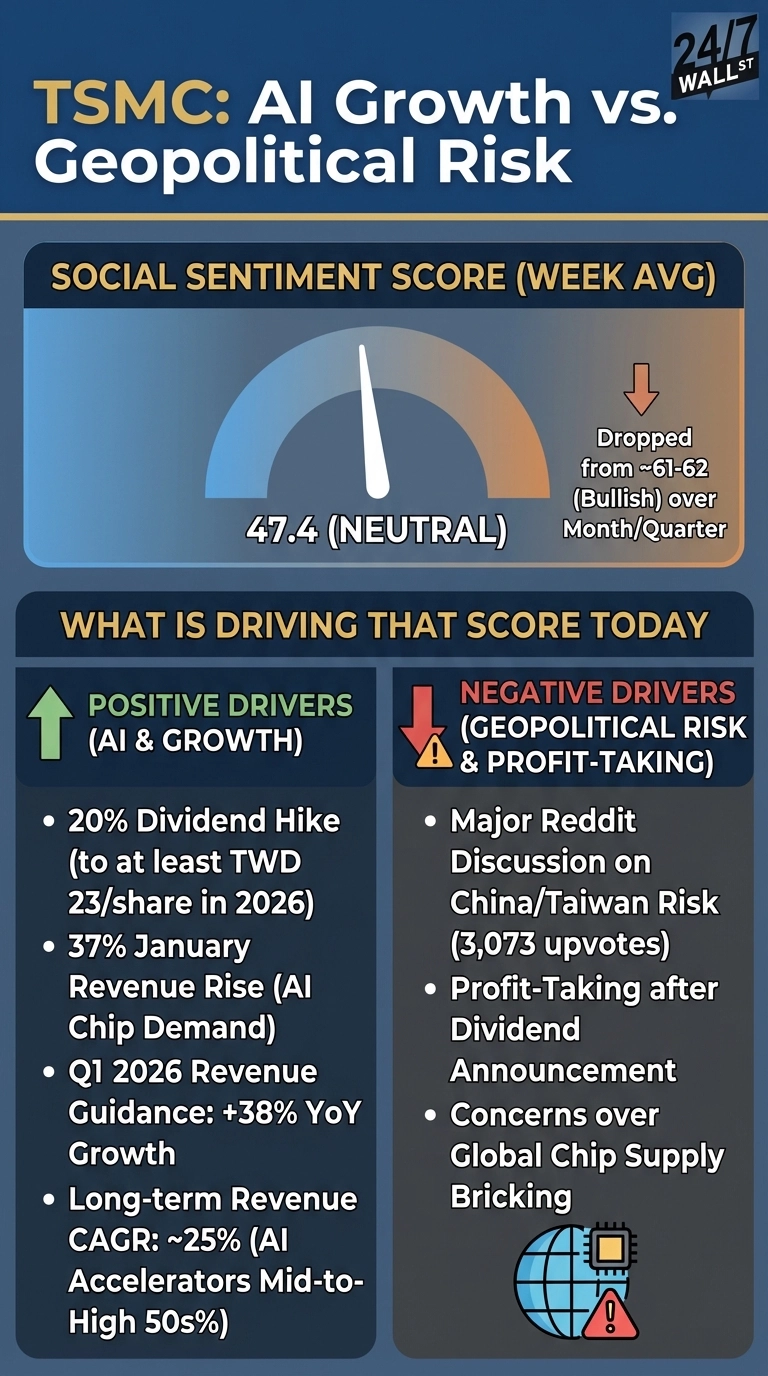

Reddit sentiment has pulled back to 47.4 (neutral) from a monthly average of 61.2 (bullish), coinciding with profit-taking discussion after the dividend announcement. The quarterly average of 62.5 tells the more durable story.

The Numbers Behind the Dividend Confidence

January 2026 revenue rose 37% year-over-year on AI chip demand as Q4 2025 delivered 62.3% gross margins and 54% operating margins, with full-year 2025 EPS of TWD 66.25, up 46.4% year-over-year. CEO C.C. Wei has guided for approximately 25% long-term revenue CAGR in USD terms through 2029, with AI accelerators projected at a mid- to high-50% CAGR over the same period.

The r/stocks community responded when “TSMC January revenue rises 37% on AI chip demand” drew 155 upvotes and 29 comments, pushing sentiment into the 68-75 range for several days.

TSMC January revenue rises 37% on AI chip demand

by u/[OP] in r/stocks

Three Key Metrics From Recent Earnings

- TSMC controls roughly 70% of the global semiconductor foundry market, giving it irreplaceable leverage over every AI chip roadmap from Apple to NVIDIA

- Q1 2026 revenue guidance of $34.6-$35.8 billion implies 38% year-over-year growth at the midpoint, with gross margins expected at 63-65%

- A $52-$56 billion 2026 capital expenditure budget, up from $40.9 billion in 2025, signals conviction that AI demand is durable

CFO Wendell Huang framed the long-term profitability floor directly: “We believe a long-term gross margin of 56% and higher through the cycle is achievable, and we can earn an ROE of high 20s percent through the cycle.” Q4 2025 ROE came in at 38.8%, well above that target.

Moving deeper into 2026, it’s fair to say that geopolitical risk remains the key overhang. A r/stocks thread on China-Taiwan tensions drew 3,073 upvotes and 988 comments, the most engaged TSM discussion in the dataset. TSMC’s Arizona expansion and a $250 billion U.S. chipmaking investment deal are the company’s most visible responses, though the community is clearly not dismissing the risk. With 17 of 18 analysts rating TSM as Buy or Strong Buy, the recent sentiment dip coincides with broader profit-taking discussions following the dividend announcement.

“With the US hitting Venezuela today, is anyone else terrified China takes Taiwan next? (and bricks the global chip supply)”

r/stocks thread on China-Taiwan tensions

by [OP] in r/stocks