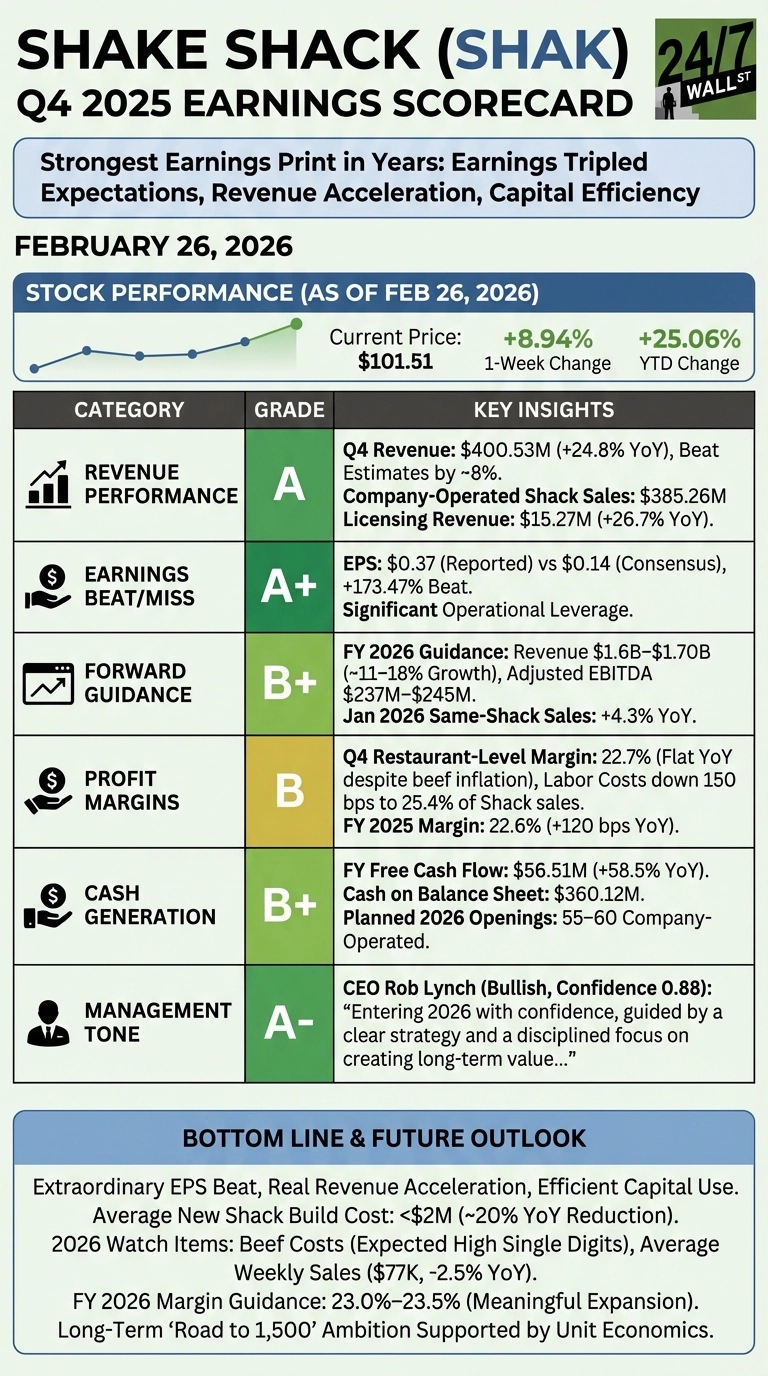

Shake Shack (NYSE: SHAK) | SHAK Price Prediction delivered a standout Q4, posting earnings that nearly tripled Wall Street’s expectations while accelerating revenue growth to its fastest pace in recent memory. Shares responded sharply, climbing to $101.51 as of Thursday morning, up nearly 9% over the past week and 25% year-to-date. For a brand still proving its profitability story, this report lands at exactly the right moment.

Q4 2025 Earnings Scorecard

Bottom Line

This was Shake Shack’s strongest earnings print in years, and the numbers back it up across nearly every dimension. The EPS beat was extraordinary, the revenue acceleration is real, and management is putting capital to work efficiently: average new Shack build costs fell 20% YoY to under $2M, making unit expansion far more capital-efficient than it once was.

The main watch items heading into 2026 are beef costs, which management expects to remain elevated at high single digits, and average weekly sales of $77K, down 2.5% YoY as newer locations ramp. Neither is alarming given the broader context, but both deserve monitoring. Guidance for restaurant-level margins to reach 23.0–23.5% in 2026 would represent meaningful expansion if achieved. Investors focused on Shake Shack’s long-term “Road to 1,500” ambition have the most tangible evidence yet that the unit economics can support it.

Contact [email protected] for any questions or corrections.