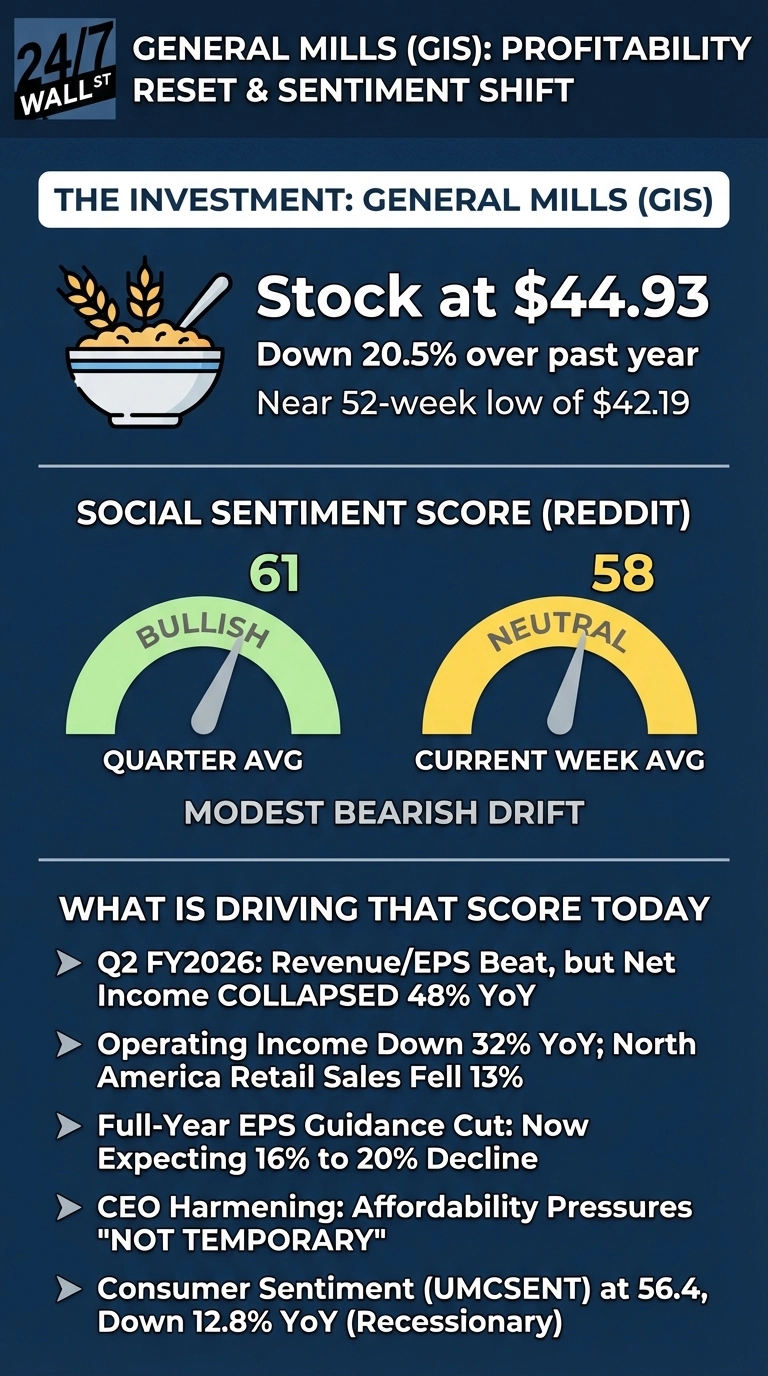

A household name in kitchens around the country and the world, General Mills (NYSE:GIS | GIS Price Prediction) shares trade at $44.93, down 24% over the past year and just $2.14 above the 52-week low of $42.79. The catalyst: a guidance reset that cut full-year organic sales by 1.5% to 2% and adjusted EPS by 16% to 20% for fiscal 2026, steeper than the prior 10% to 15% guide. CEO Jeff Harmening has rightfully acknowledged that affordability pressures are “not temporary,” as lower-income consumers shift toward private-label alternatives.

The Headline Beat Masked a Profitability Collapse

If you took just a quick look at Q2 FY2026 results, everything looks fine on the surface as the company reported revenue of $4.90 billion against a $4.83 billion estimate and adjusted EPS of $1.10 versus the $1.03 consensus. Underneath, operating income fell 32% year-over-year to $728 million, net income dropped 48% to $413 million, and North America Retail saw net sales fall 13% to $2.9 billion. Management is deliberately trading near-term margin for volume recovery through promotional pricing and media spend. Harmening framed it on the Q4 FY2025 call: “For a long-term algorithm to work in the food space, about half of your growth should come from volume and half from pricing. In recent years, we witnessed record inflation, relying heavily on pricing with little volume growth.”

Reddit Is Watching, Not Buying In

Retail sentiment on Reddit slipped from a quarterly average of 61 to a current weekly score of 58. Discussion is concentrated in r/investing and r/stocks, with GIS surfacing as a passive portfolio holding rather than an active thesis. One commenter in the r/stocks thread asked, “Are there any stocks hovering near their 52-wk low you’re closely watching right at the end of year, expecting selling pressure to lift?” — illustrating how retail investors are eyeing GIS near its 52-week low but remaining on the sidelines.

Are there any stocks hovering near their 52-wk low you’re closely watching right at the end of year, expecting selling pressure to lift?

by u/Puzzleheaded_Yam7582 in stocks

Three reasons retail investors remain hesitant:

- Analyst consensus forecasts an 8.1% annual earnings decline over the next three years, with Bank of America downgrading to Neutral at $48 and Mizuho trimming its target from $52 to $47.

- University of Michigan consumer sentiment sits at 56.4, down 12.8% year-over-year, directly pressuring the volume recovery General Mills is banking on.

- CIO Donald Monk’s departure to Hormel Foods creates execution risk at a critical moment for supply chain and promotional decisions.

A Low Bar With Shrinking Room for Error

As of late February 2026, General Mills trades at a trailing P/E of 9.71x and yields 5.3%, metrics that have historically attracted value-oriented investors to the stock. But the analyst target range tells the real story: $42 to $60, averaging $48.16, with the stock at $44.93 sitting barely above the low end. Zacks assigned a Strong Sell this week, calling it “Bear of the Day.” The next meaningful catalyst for investors to watch is the company’s Q3 FY2026 report, where investors will look for evidence that North America Retail volumes are stabilizing. Until then, this is a show-me story in a sector where the macro backdrop is not cooperating.

Contact [email protected] for any questions or corrections.