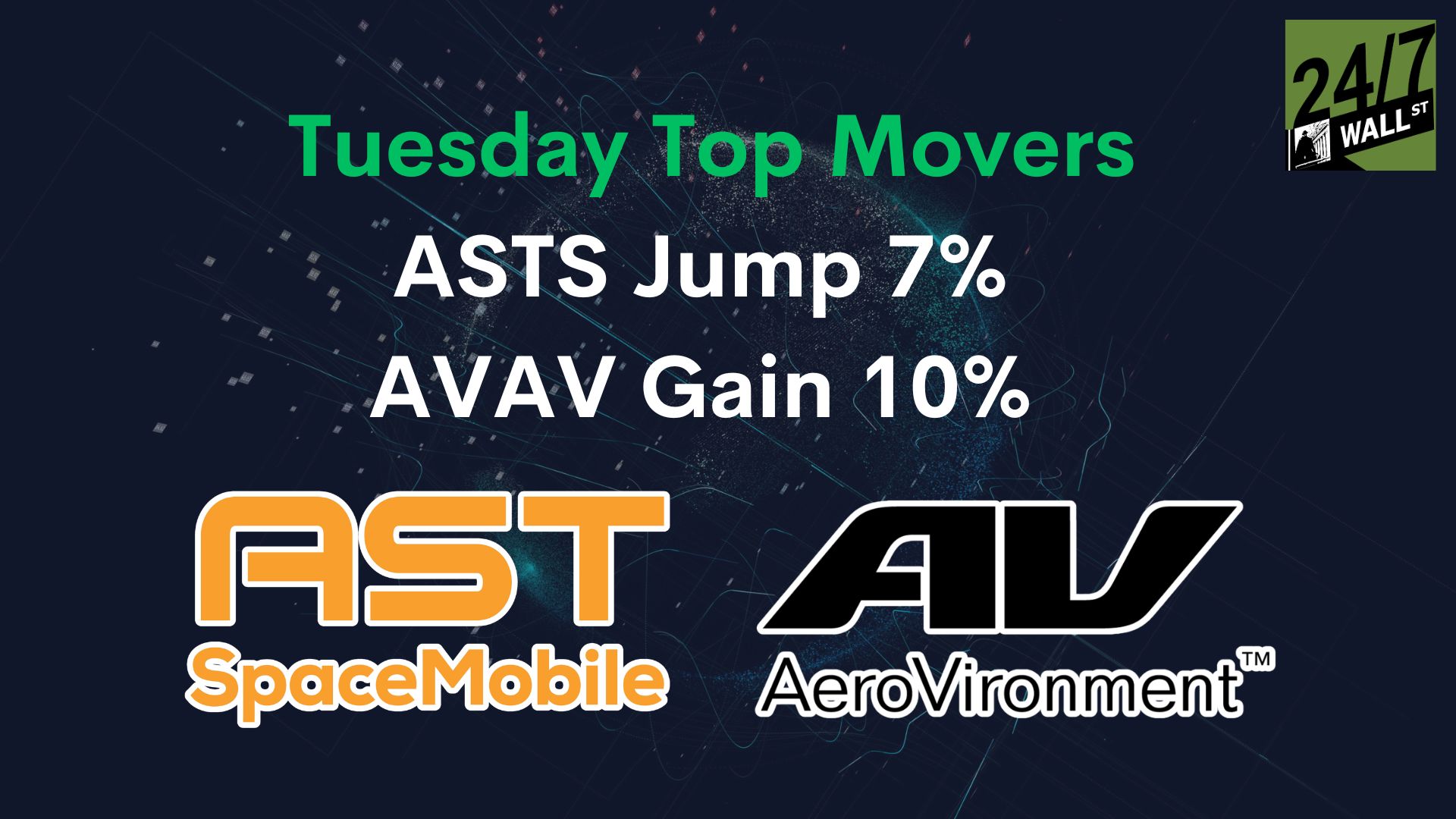

Two stocks bucked a rough tape on Tuesday, March 3, 2026. AeroVironment closed at $228.30, up 9.59%, while AST SpaceMobile finished at $92.68, up 6.63%. Both moves came against a backdrop of the S&P 500 slipping roughly 1% after a brutal opening, making these standout performances worth understanding.

ASTS: First Revenue, Real Momentum

AST SpaceMobile reported its Q4 2025 earnings on the evening of March 2, 2026, and the numbers gave investors something concrete to hold onto for the first time.

Revenue came in at $54.3 million, crushing the consensus estimate of $42.2 million by nearly 29%. That kind of beat gets attention. But the bigger story is what that number represents. A year ago, this company was barely generating revenue at all. Year-over-year revenue growth clocked in at 2,731%. That is not a typo.

CEO Abel Avellan framed it plainly on the earnings call:

“For the first time in 2025, AST SpaceMobile became a revenue generating business and it significantly advanced all key aspects of our operations including commercial, government, manufacturing, spectrum rights, IP portfolio, and capital position.”

That is a company crossing a threshold. Investors responded accordingly. AST pointed toward revenue reaching $1 billion in 2027, driven by both commercial contracts and government business.

The revenue breakdown matters too. Product revenue of $36.2 million came from 15 gateway deliveries across five continents, while service revenue of $18.1 million included a $30 million Space Development Agency prime contract. These are real contracts with real counterparties, not letters of intent.

The forward picture adds fuel. The company holds over $1.2 billion in contracted partner commitments, including a $175 million prepayment from stc Group. Liquidity stands at over $3.9 billion pro forma, including a $1.07 billion convertible notes offering. And BlueBird 7 is already encapsulated at Cape Canaveral, awaiting a March launch, with the company targeting 45 to 60 satellites in orbit by end of 2026. The losses remain real, with a net loss of $74 million in Q4, but the market is clearly pricing the trajectory, not the current income statement.

AVAV: Bouncing Back From a Downgrade

AeroVironment’s story today is a rebound. The stock took a hit Monday following a Wall Street downgrade, but buyers stepped in hard on Tuesday. The stock is still down nearly 18% over the past month, so context matters: today’s bounce comes off a compressed base, not a new high.

The underlying business, however, tells a different story than the recent price action suggests. The company’s most recent quarter showed revenue of $472.5 million, up 181.9% year over year, driven heavily by the BlueHalo acquisition that closed in May 2025. Yes, the company missed EPS estimates by a wide margin and gross margins compressed to 22% from 39% a year earlier, largely due to $48.2 million in quarterly intangible amortization and purchase accounting charges from BlueHalo. Those charges are non-cash and expected to fade over time.

The company’s backlog has been the bigger battleground.

AeroVironment reported record contract awards with a ceiling value of $3.5 billion in the most recent quarter, including an $874 million FMS IDIQ for UAS and Switchblade systems. The book-to-bill ratio hit 2.9x, meaning the company is booking nearly three dollars of new business for every dollar it recognizes in revenue. That is a powerful leading indicator.

CEO Wahid Nawabi put it directly: “AV is operating from a position of strength as evidenced by our record second quarter results, all-time high bookings and long-term contract wins.”

We covered it yesterday, but Raymond James downgraded the company on fears its contract with Space Force (the SCAR program) could be recompeted, which could potentially cut the company’s backlog in half. The uncertainty punished share severly esterday, with shares dropping more than 30% intraday. Yet, several Wall Street firms came to Aervironment’s defense today, with the company noting it’s in active talks with Space Force on an amendment to the SCAR ground station contract.

Full-year FY2026 guidance calls for $1.95 to $2.0 billion in revenue with 93% visibility. Analysts who hold a consensus price target of $367 on the stock are clearly looking through the near-term margin noise to what the business could look like once BlueHalo integration settles.

What to Watch

For ASTS, the next satellite launch in March is the immediate catalyst to track. Whether the company can maintain its launch cadence will determine if the revenue ramp holds. For AVAV, watching the news will be important in the coming weeks. The debate around its potential revenue loss from the SCAR contract will continue to dominate price action around the stock.

Contact [email protected] for any questions or corrections.