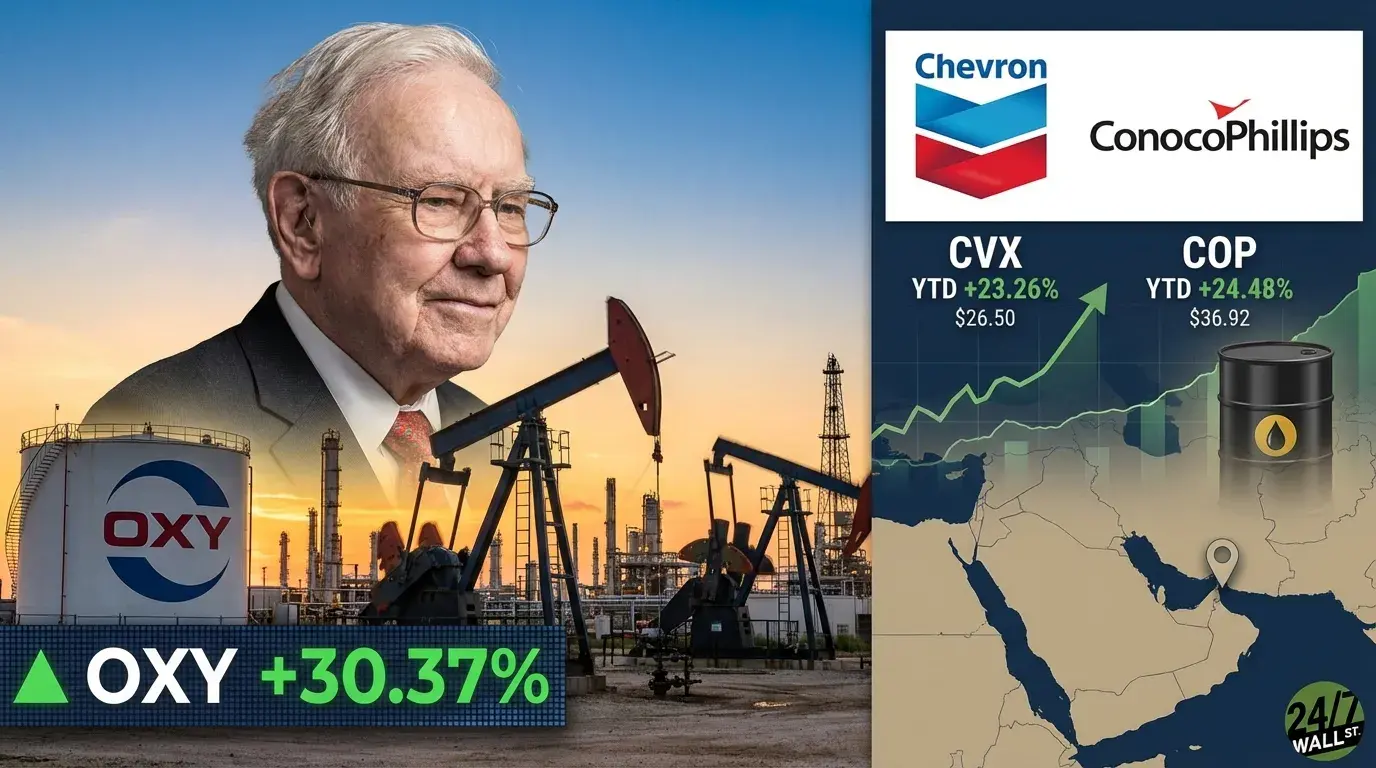

Warren Buffett’s long-running bet on Occidental Petroleum is looking prescient. Occidental Petroleum (NYSE:OXY) has surged 30.37% year-to-date, and the catalyst accelerating that move is the same one rattling global energy markets: the death of Iranian Supreme Leader Ayatollah Ali Khamenei on February 28, 2026, which triggered fears of Strait of Hormuz supply disruptions and sent WTI crude to $71.13 per barrel, up 10.3% over the past month. Some analysts are now suggesting prices could reach $100 if tensions persist.

Berkshire Hathaway closed its acquisition of OXY’s chemicals unit, OxyChem, on January 2, 2026, with OXY using proceeds to slash principal debt by $5.8 billion, bringing total debt to $15.0 billion. The leaner balance sheet, combined with a Q4 2025 production beat of 1,481 Mboed and an 8% dividend increase to $0.26 per share quarterly, validates the strategic pivot CEO Vicki Hollub has been executing. The stock trades at a forward P/E of roughly 27x, above the analyst consensus target of $51.88, meaning much of the good news is priced in at current levels near $53.61.

Two other large-cap energy names have also moved sharply on the geopolitical catalyst.

Chevron: Scale, Yield, and Record Cash Flow

Chevron (NYSE:CVX) delivered 23.26% gains year-to-date and generated a record $33.9 billion in operating cash flow for full-year 2025, returning $27.1 billion to shareholders through buybacks and dividends. Its quarterly dividend of $6.84 annually per share represents a 3.6% yield at current prices near $186. The forward P/E sits around 25x, with 16 analyst buy or strong-buy ratings against just one sell. Permian Basin production hit 1 million BOE per day in 2025, and structural cost cuts of $1.5 billion achieved with a $3-4 billion target by end of 2026 give Chevron meaningful earnings leverage if oil prices hold.

ConocoPhillips: Valuation and Metrics

ConocoPhillips (NYSE:COP) trades at a trailing P/E of 18x. It is up 24.48% year-to-date with the analyst consensus target of $117.04 implying modest additional upside from the current price near $115.65. The Marathon Oil integration has already delivered more than $1 billion in run-rate synergies, and management projects $7 billion in incremental free cash flow by 2029. The company plans to return 45% of cash from operations to shareholders in 2026.

With WTI near a 12-month high and geopolitical risk still elevated in the Middle East, energy fundamentals remain supportive. The key variable to watch is whether Hormuz tensions escalate further or de-escalate quickly, as that will largely determine whether this oil rally has legs or fades as fast as it arrived.