Dividend King stocks are those that have over half a century of consecutive dividend increases on record. Kimberly-Clark (NASDAQ:KMB), Federal Realty Investment Trust (NYSE:FRT), and Stanley Black & Decker (NYSE:SWK) yield over 4% and have good upside potential as investors move back to dividend stocks. Growth stocks are finally letting off some steam, and with interest rates potentially coming down more, these dividend stocks are worth getting more exposure to.

Dividend Kings in particular deserve more attention since these companies are unlikely to disappoint. The typical tech growth stock comes with an expiry date, since competition is high and Wall Street is constantly re-rating the stock. Dividend Kings are on a more stable trajectory, and their place in the market has crystallized. You get reliable, increasing dividends that can snowball your holdings over time.

If you buy them at a discount, that makes it all the better. There are only 6 Dividend King stocks that have a dividend yield above 4%, so these three are your best bets.

Kimberly-Clark (KMB)

Kimberly-Clark makes essential products with low demand elasticity, such as Huggies diapers and Kleenex tissues. These products are not going to get hit during downturns, and consumers have the purchasing power to keep buying them as they’re not big-ticket purchases.

KMB stock is down by 19% in the past 6 months due to Kimberly-Clark announcing it is buying Tylenol-maker Kenvue in a massive $48.7 billion cash-and-stock deal. That’s on top of the core business itself having anemic growth and declining margins.

The acquisition itself can be very positive for Kimberly-Clark, since it sees $1.9 billion in cost synergies and another $500 million in revenue synergies, totaling $2.1 billion in run-rate benefits. That changes the optics of the deal dramatically. At face value, paying 14.3x Kenvue’s EBITDA sounds steep. But once you fold in those synergies, the effective acquisition multiple drops to 8.8x.

The market’s worries are more near-term due to the acquisition, and KMB has likely bottomed out already.

You get a 4.88% dividend yield with a 66.9% payout ratio. There have been 53 consecutive years of dividend growth.

Federal Realty Investment Trust (FRT)

Federal Realty Investment Trust is a retail-focused real estate investment trust (REIT). It is one of the oldest names in the industry, and that’s also why you get 57 consecutive years of dividend growth. FRT stock has a 4.13% dividend yield and a payout ratio of 60.76%.

REITs are special, especially in this environment. Interest rates are declining, property prices are still climbing, and these companies have shown they can survive record interest rate hikes and keep raising dividends without budging.

Federal Realty ended 2025 with its overall portfolio 96.1% leased and 94.1% occupied. CEO Donald Wood put it simply on the call: “Strong quarter, strong year, strong 2026 guidance.” The company delivered its highest-ever annual leasing volume in company history, alongside the strongest comparable rent spreads achieved in over a decade. COO Wendy Seher added that those rent spreads were truly broad-based, not concentrated in one geography or property type: “It does not get any better than right now.”

The stock itself has underperformed since 2016, but is now recovering due to all the tailwinds REITs are receiving. It’s a broad phenomenon across the whole sector, but FRT is the only REIT that is also a Dividend King. I see significantly more upside ahead as the stock recovers to $130 and beyond.

Stanley Black & Decker (SWK)

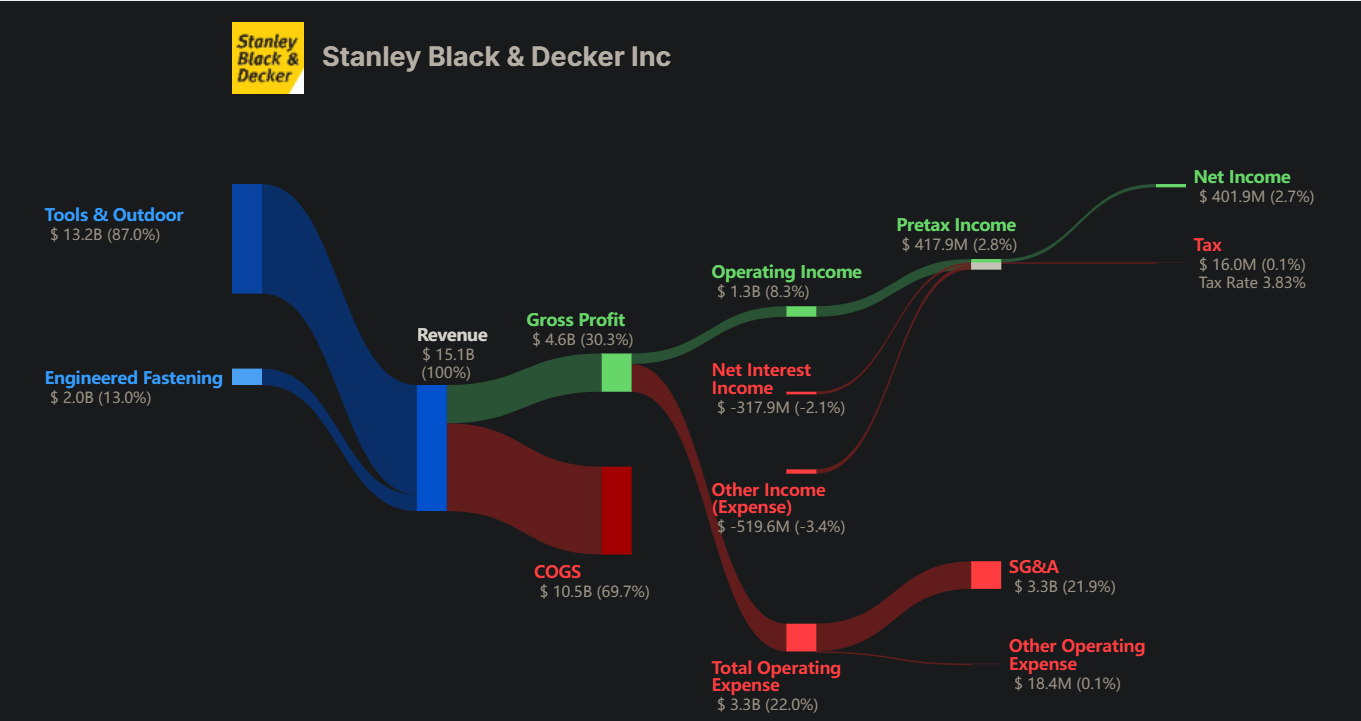

SWK stock was one of the worst-hit victims of the interest rate hike cycle, and it is now 64% off its high in 2021. The company carries $6 billion of debt with a $12 billion market cap. Stanley Black & Decker carried a debt load of more than $7.5 billion in 2022 when interest rate hikes got aggressive.

It is still reeling from high interest rates, but I believe SWK is on the brink of an impressive recovery. Net interest losses came in at $317.9 million for all of 2025. The company still managed to post $401.9 million in net income, but it’s clear just how much this is dampening sentiment.

SWK stock has been recovering strongly, up 25% from its November 2024 low, but a full recovery is still far. I see opportunity in this, as this is a stock with triple-digit upside potential in the coming years and a Dividend King at that. The floor price of SWK is ~$60, which makes it a very good deal in my book.

SWK has a forward P/E ratio just over 14, with the dividend yield at 4.23%. If you factor in the debt paydown, the enterprise value is rising fast, so you have a shareholder yield pushing to nearly 6.5%. This is better than 87% of stocks in the Industrial sector.

Dividends have been increased for 57 consecutive years.