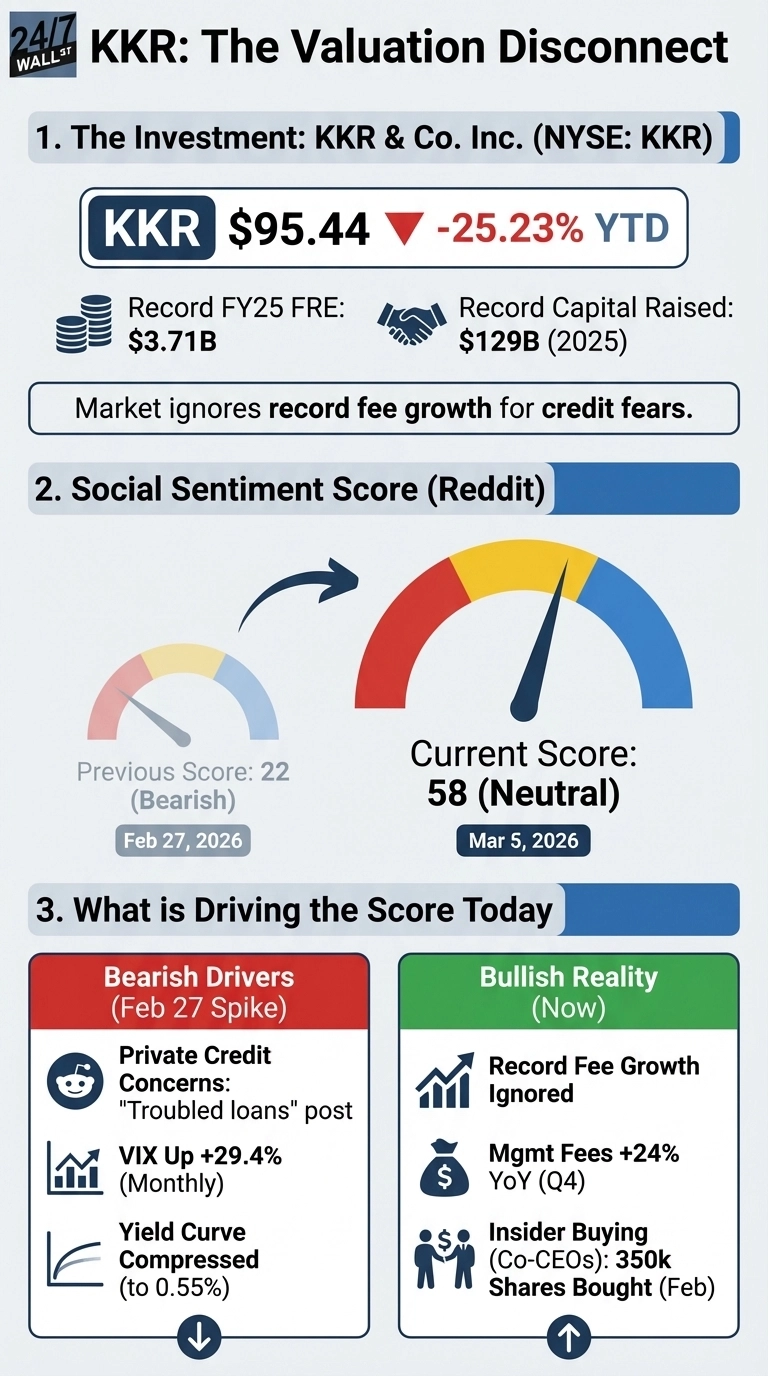

One of the foremost financial companies in the world, shares of KKR (NYSE:KKR) are trading at $95.44 today, down 25.23% year-to-date and off 27.83% from its July 2025 peak. That decline sits alongside a Q4 earnings report that included record full-year Fee Related Earnings of $3.71 billion and $129 billion in new capital raised, the highest fundraising year in KKR’s history. The gap between those two facts is what retail investors are wrestling with right now.

The Q4 EPS miss of $1.12 versus the $1.14 estimate was largely mechanical: a $207 million carried interest repayment obligation dragged the headline number. Stripping that out, adjusted EPS would have been $1.30. Management fees grew 24% year-over-year in Q4, and CFO Robert Lewin noted KKR grew management fees 46% relative to operating expense growth of 21%, an inverse of what its three closest peers delivered.

Private Credit Concerns Are Driving the Narrative

Reddit sentiment tells a specific story. Sentiment dropped to a bearish 22 on February 27, driven by a post in r/investing titled “Private credit fund managed by KKR reports jump in troubled loans”. The post spread quickly through retail investing communities, with the original poster writing:

“KKR’s private credit fund saw a notable rise in non-accrual loans, raising questions about credit quality as the firm continues to scale its direct lending business.” — r/investing

Private credit fund managed by KKR reports jump in troubled loans

by u/[unknown] in investing

By March 5, sentiment normalized to 58 in r/stocks, but the underlying concern remains.

Three reasons the skepticism has traction:

- The yield curve spread compressed from 0.74% on February 9 to 0.55% today, tightening conditions that pressure private credit portfolios

- Net realized performance income fell to $62 million in Q4 from $306 million year-over-year

- The VIX sits at 21.15, up 29.4% over the past month, reflecting risk-off sentiment that hits alternative asset managers disproportionately

KKR’s Own Insiders Are Answering the Question

The clearest counter-signal comes from inside the firm. Both Co-CEOs bought shares into the weakness: Joseph Bae and Scott Nuttall each acquired 175,000 shares across transactions on February 17 and February 27, with Nuttall purchasing 50,000 shares at $87.81 and Bae buying 50,000 shares at $88.56 on the same day the private credit headline hit Reddit. Board members followed, including Mary Dillon purchasing 22,225 shares at $90.96 on March 2.

What Analysts Are Watching

The analyst consensus target sits at $140.40 against today’s price near $95, with 19 buy ratings and zero sells. Analysts are watching whether KKR’s $60 billion of committed AUM not yet paying fees converts to revenue on schedule, and whether the Arctos Partners acquisition clears sports league approvals ahead of KKR’s 50th anniversary on May 1st.