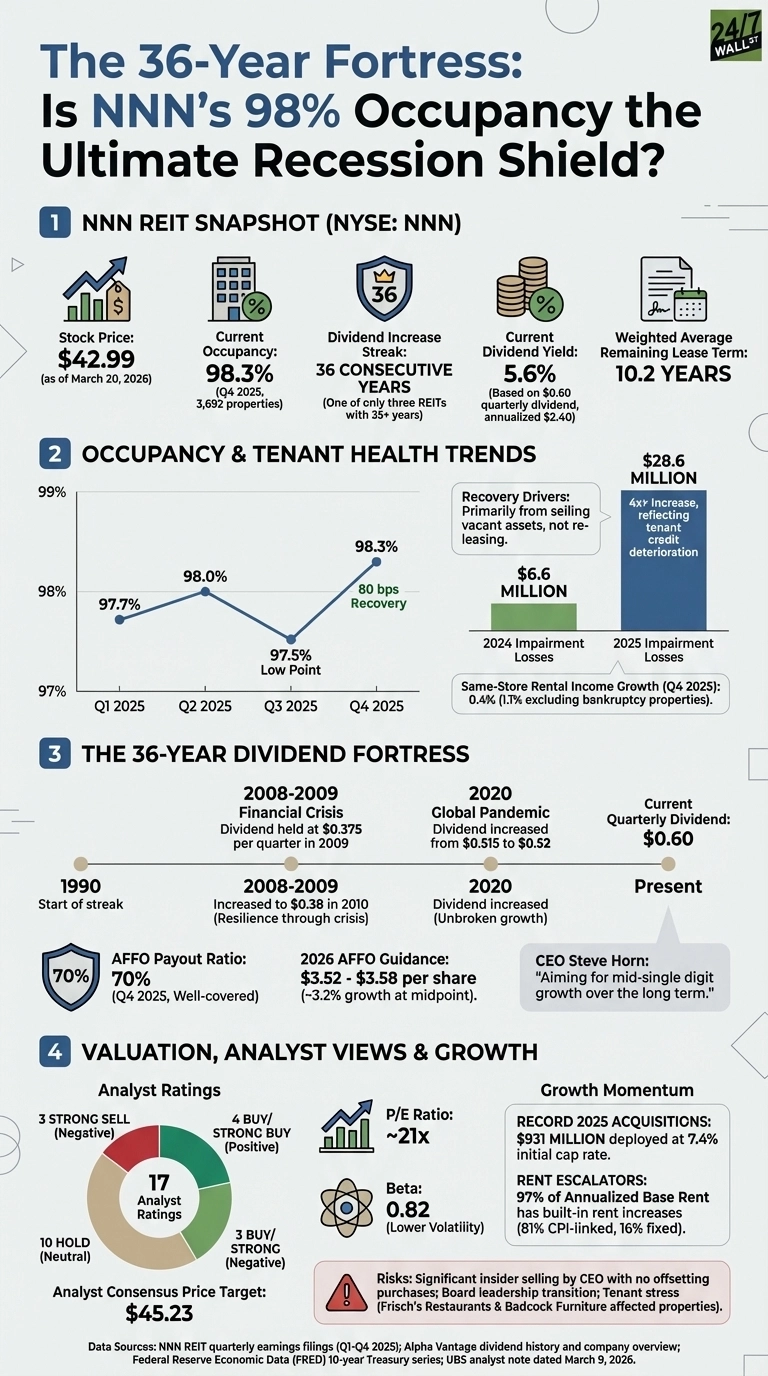

Few REITs can claim what NNN REIT (NYSE:NNN) has quietly built over three and a half decades: a dividend raised every single year since 1990, through two recessions, a global pandemic, and the sharpest rate-hiking cycle in a generation. With occupancy having improved to 98.3% in Q4 2025 and the stock trading near $42.46 as of March 20, the question is whether this is a structural floor or a temporary ceiling.

The Occupancy Story Is More Nuanced Than the Headline

The 98.3% figure marks an 80-basis-point sequential recovery from Q3 2025’s 97.5%, itself the low point after tenant stress from Frisch’s Restaurants and Badcock Furniture, which rejected leases for 32 properties, pushing vacancies to roughly 90 properties at their peak. CEO Steve Horn framed the recovery plainly: “Our occupancy is up 80 basis points from last quarter to 98.3%, which is in line with our long-term average of roughly 98%.” Most of that gain came from selling vacant assets rather than re-leasing them, a distinction the CFO was candid about on the earnings call.

The full-year impairment picture adds context: $28.6 million in impairment losses in 2025 versus $6.6 million in 2024, a 4x-plus jump reflecting real tenant credit deterioration even as headline occupancy held near historical norms. Same-store rental income grew just 0.4% in Q4 2025, or 1.1% excluding bankruptcy-affected properties.

The Dividend Fortress Has 36 Years of Proof

NNN raised its dividend through the 2008 financial crisis, holding at $0.375 per quarter through 2009 before increasing again in 2010, and through the 2020 pandemic, nudging from $0.515 to $0.52. The current quarterly rate of $0.60 per share yields approximately 5.65% at today’s price, compared with the 10-year Treasury at 4.38%. That spread of roughly 127 basis points above the risk-free rate is the core income argument for the stock.

The payout is well covered: AFFO payout ratio is 65.7%, with 2026 AFFO guidance of $3.52 to $3.58 per share, representing approximately 3.2% growth. Horn’s stated long-term goal is “mid-single digit growth over the long term.”

Valuation and What Analysts See

Looking at what analysts believe is next for NNN, UBS raised its price target to $45 from $43 on March 9 while maintaining a Neutral rating. The analyst consensus target sits at $45.23, implying modest upside from current levels. Of 17 analyst ratings, 10 are Hold, 4 are Buy or Strong Buy, and 3 are Strong Sell. The stock trades at a P/E of roughly 21.9x with a five-year beta of 0.83, reflecting its historically lower volatility relative to the broader market.

One risk worth watching: significant insider selling by CEO Stephen Horn with no offsetting insider purchases, alongside a board leadership transition. Neither is disqualifying on its own, but they add uncertainty to an otherwise methodical story.

NNN’s $931 million in record 2025 acquisitions at a 7.4% initial cap rate, with 97% of annualized base rent carrying built-in escalators, gives the portfolio structural momentum. Whether that momentum is already priced in remains the question the market has not yet decisively answered.

Data Sources: NNN REIT quarterly earnings filings (Q1-Q4 2025); Alpha Vantage dividend history and company overview; Federal Reserve Economic Data (FRED) 10-year Treasury series; UBS analyst note dated March 9, 2026.