Founded in 1991, Arbor Realty Trust (NYSE:ABR) sits at the center of one of the sharpest disagreements in the REIT sector: insiders are buying aggressively, while short-sellers have built a formidable position betting against it.

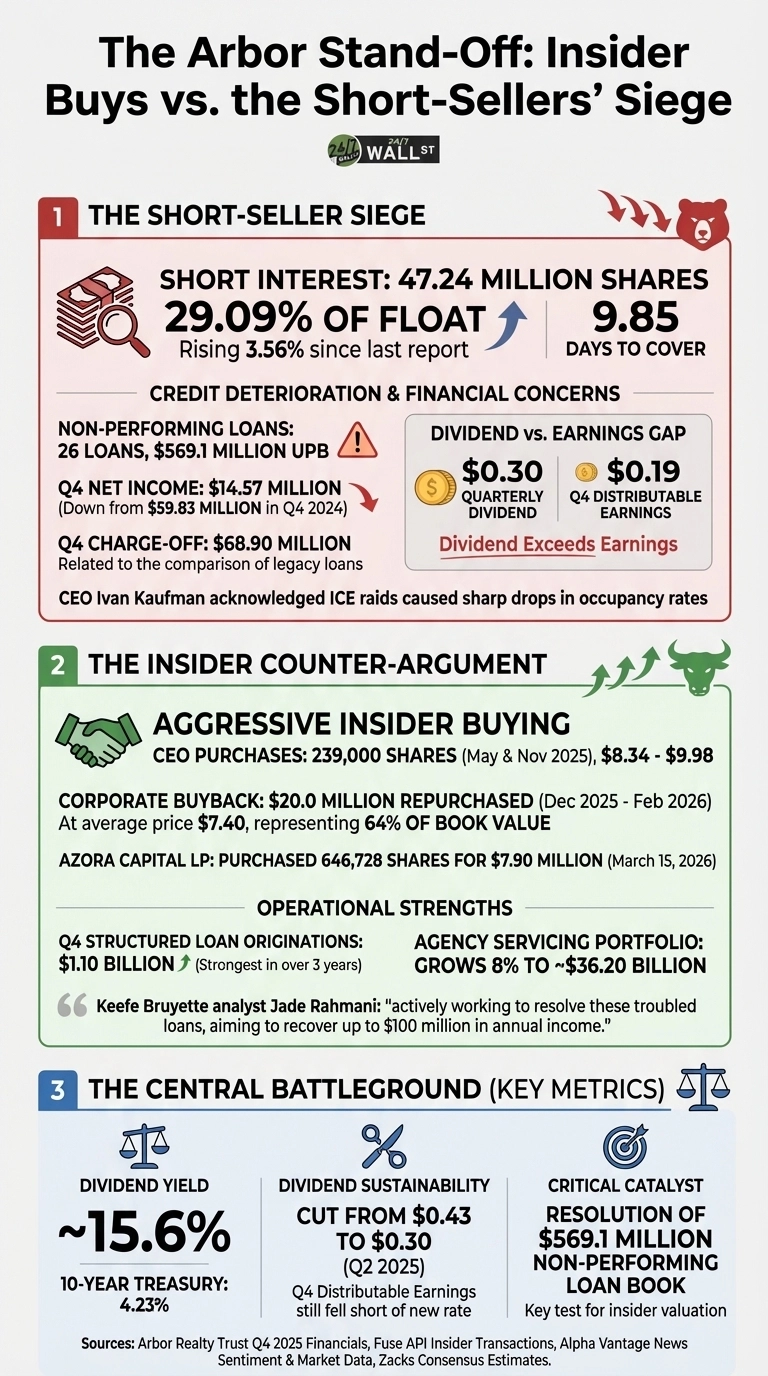

The Short-Seller Position

Nearly 47.24 million shares are sold short, representing 29.09% of the float, with 9.85 days to cover, and short interest has risen 3.56% since the last report. Bears point to a deteriorating credit picture: 26 non-performing loans with an unpaid principal balance of $569.1 million; a $68.90 million charge-off in Q4 tied to legacy loans; and net income fell to $14.57 million in Q4 2025 from $59.83 million in Q4 2024. The dividend math also raises flags: the $0.30 quarterly dividend exceeds Q4 distributable earnings of $0.19 per share.

Analysts have taken note, with the Zacks consensus estimate revised down 28.1% over the last 30 days and the stock carrying a Zacks Rank of #4 (Sell). ICE enforcement activity in Sun Belt markets added another wrinkle: CEO Ivan Kaufman acknowledged that raids “caused sharp drops in occupancy rates at affected properties, particularly in Houston.”

The Insider Counter-Argument

Kaufman and his management team have been putting personal capital to work. The CEO made open-market purchases totaling 210,000 shares in May 2025 at prices ranging from $8.70 to $9.98 per share, followed by another 29,000 shares in November 2025 at $8.34 per share. The CFO, CCO, and multiple EVPs joined the May buying wave.

At the corporate level, Arbor repurchased $20.0 million of stock at an average price of $7.40 per share between December 2025 and February 2026, representing 64% of book value. Institutional investor Azora Capital LP added to the signal, purchasing 646,728 shares for $7.90 million as recently as March 15, 2026.

The bull case rests almost entirely on operational momentum beneath the credit noise. On the plus side, structured loan originations hit $1.10 billion in Q4, the strongest quarter in over three years, while the agency servicing portfolio grew 8% to approximately $36.20 billion.

Keefe Bruyette analyst Jade Rahmani, despite maintaining an Underperform rating, noted that “the company is actively working to resolve these troubled loans, aiming to recover up to $100 million in annual income.”

What Investors Should Watch

The dividend, yielding roughly 15.6% against a 10-year Treasury at 4.23%, is the central battleground. The cut from $0.43 to $0.30 in Q2 2025 was meant to reset the payout to a sustainable level, but Q4 distributable earnings still fell short of the new rate. Analysts project next fiscal year EPS of $1.10, which analysts suggest would materially improve dividend coverage.

Resolution of the $569.1 million non-performing loan book is the clearest near-term catalyst, either way. Resolution of the $569.1 million non-performing loan book will be the key test of whether the insider purchases at 64% of book value were well-calibrated. If delinquencies deepen, the short thesis gains further support.

Data Sources

- Arbor Realty Trust Q4 2025 earnings and financial data via 247 Wall St. stock data context

- Insider transaction history sourced from Fuse API insider transactions endpoint (1,222 records, filtered extract covering January 2024 through March 2026)

- Short interest, analyst commentary, and CEO quotes sourced from Alpha Vantage news sentiment feed (February-March 2026 coverage window)

- Dividend history and forward earnings estimates from Alpha Vantage Dividends and Overview endpoints, supplemented by Zacks consensus data via user-provided source documents