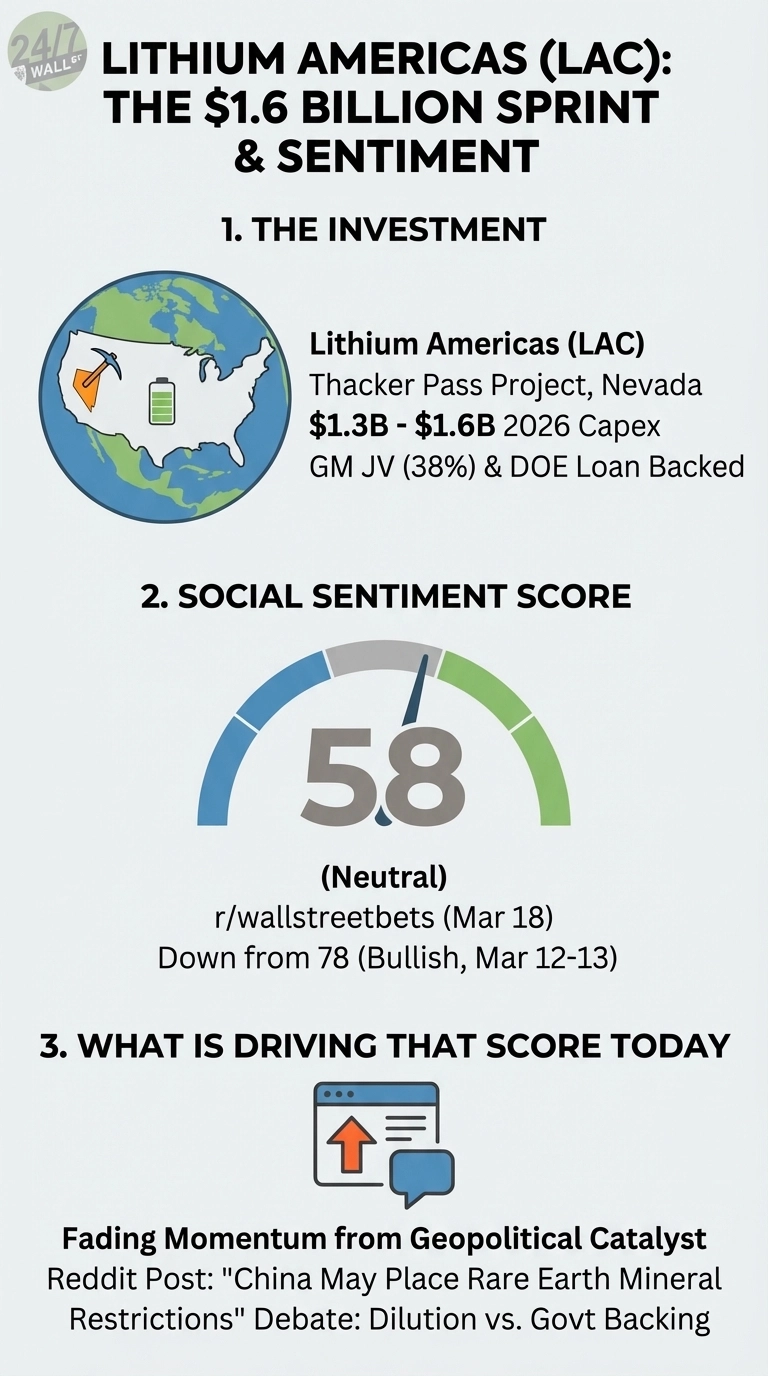

A Canadian-based mining company, Lithium Americas (NYSE:LAC), is spending at a pace that would make most pre-revenue companies flinch. With $1.3 billion to $1.6 billion in capital expenditures planned for 2026 and a workforce set to nearly double to roughly 1,800 workers on site by late 2026, this is the peak construction year at Thacker Pass. The question Reddit investors are wrestling with: is Lithium Americas a rare domestic lithium play backed by the U.S. government, or is relentless share dilution quietly eating away at future upside?

Sentiment shifted noticeably over the past week. LAC held a bullish score of 78 on r/stocks from March 12 through 13 before sliding to a neutral 58 on r/wallstreetbets by March 18, a 20-point drop tied to fading momentum around a geopolitical catalyst. Shares are down 8.74% over the past week, though still up 41.25% over the past year.

China’s Rare Earth Move Lit the Fuse

The bullish spike on March 12 traced directly to a post on r/stocks titled “China May Place Rare Earth Mineral Restrictions March 25th.” User breakyourteethnow argued that LAC and peers like MP Materials were positioned as a national security hedge, writing: “Long term, I believe rare earth minerals even lithium and copper will become of national security. Companies like LAC & MP, which are building infrastructure backed by the Department of Energy, are a hedge against this problem, which surely will arise again and again.” The post reached 94 upvotes with a 0.94 upvote ratio.

China May Place Rare Earth Mineral Restrictions March 25th

by u/breakyourteethnow in stocks

By March 18, the conversation had migrated to r/wallstreetbets with a more skeptical tone. Three reasons the online debate stays split:

- LAC sold 68.2 million shares in 2025 at an average of $5.98 per share, then added another 32.5 million shares post-year-end at $5.92, with a fresh ATM program now active while shares sit near $4.28

- Net losses nearly doubled year-over-year to $86.3 million in 2025, with the 2026 EPS estimate at -$0.9725 per share as construction costs accelerate

- Tariff exposure on equipment from Canada, China, India, the UAE, Turkey, and the EU creates real cost escalation risk against a $2.93 billion total Phase 1 capex estimate

The Backing Is Real, But the Clock Is Running

Among the bigger news for the company, LAC pulled a second DOE loan drawdown of $432 million in February 2026, bringing total DOE funding deployed to $867 million of a $2.23 billion facility. CEO Jonathan Evans called it a meaningful de-risking of the project, stating: “This investment reflects our shared commitment to rebuilding critical mineral supply chains here at home and reducing reliance on foreign sources.” With detailed engineering 93% complete and a GM joint venture holding a 38% stake, this is not a concept-stage story.

As of March 19, 2026, analysts are carrying a consensus price target of $6.53 against a current price near $4.04, with 3 buys and 9 holds reflecting the market’s wait-and-see posture. The next meaningful signal is whether the March 25 China rare-earth briefing yields real export controls or just noise. For LAC, that date matters more than any earnings report.