Middleby Corporation (MIDD)

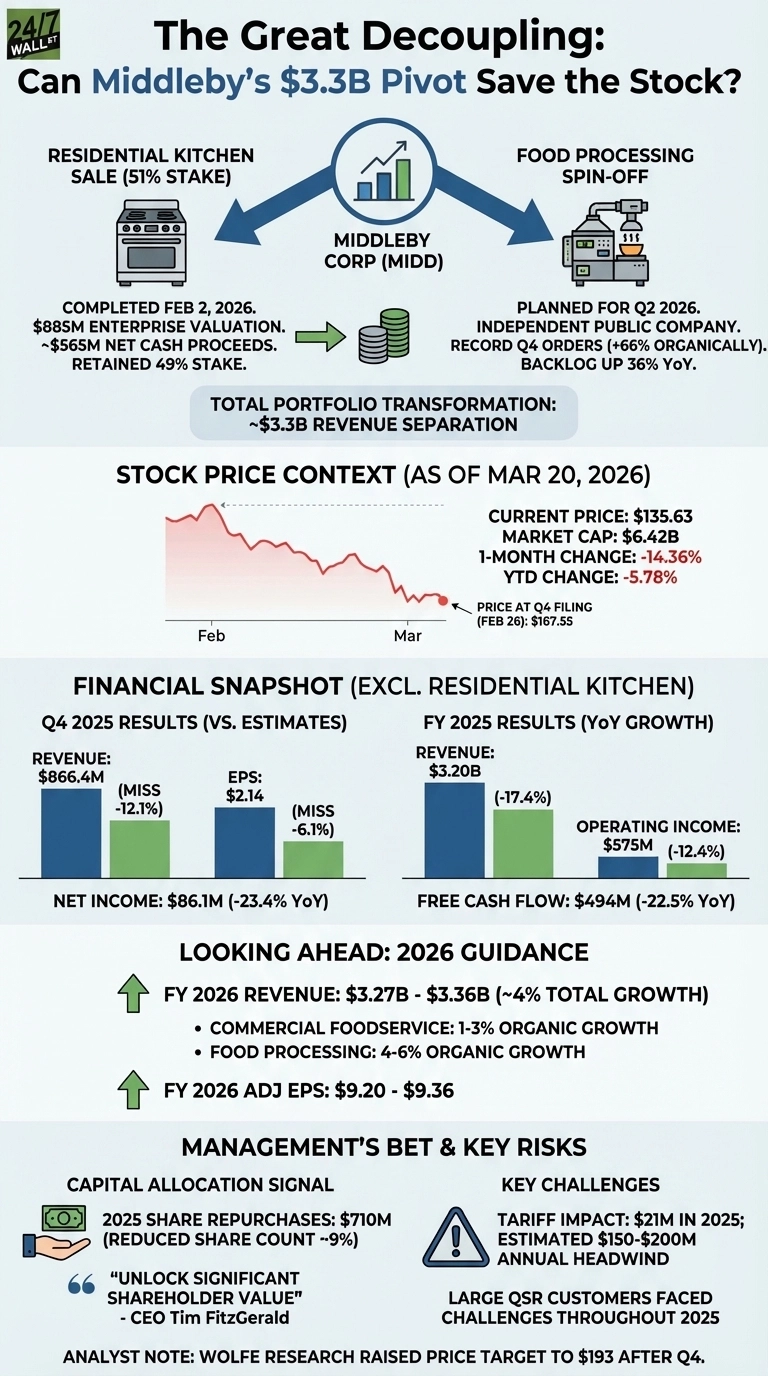

Middleby Corporation (NASDAQ:MIDD) is in the middle of its most aggressive restructuring in decades, and the stock’s reaction tells a complicated story. Despite completing a $885 million divestiture of its Residential Kitchen business and preparing a Food Processing spin-off for Q2 2026, shares have dropped 15.53% over the past month and trade at $135.81 today, well below the $169.44 52-week high the stock reached just after its Q4 earnings.

The Transformation Thesis

CEO Tim FitzGerald has framed 2025 as a pivot year for the company when he said: “We recently completed the sale of a 51% stake in our Residential Kitchen business at an $885 million enterprise valuation, delivering approximately $565 million in cash proceeds while retaining meaningful upside through our 49% ownership,” he said on the Q4 earnings call. The Food Processing segment, set to become an independent public company, finished the year with record Q4 orders, up 66% organically, and a year-end backlog, up 36%. Mark Salman, who will lead the standalone entity as CEO, grew the division’s revenue from $390 million in 2018 to $850 million in 2025 through 16 acquisitions.

As it stands, analysts are largely applauding the structure, with Wolfe Research raising its price target to $193, citing a path to improved EBITDA margins for the remaining Commercial Foodservice business. Canaccord Genuity went further, lifting its target to $203. The forward P/E is roughly 14x, a discount to peers for a business guiding to $9.20-$9.36 in adjusted EPS for 2026.

The Problem the Market Is Pricing In

The bull case depends on a business growing at a modest pace, as Commercial Foodservice posted just 0.7% revenue growth year-over-year in Q4, with full-year organic sales declining 2.4%. Large QSR (Quick Service Restaurants) customers, a key revenue driver, “faced lower traffic and cost pressures throughout 2025.” Management is counting on ice and beverage innovations and dealer channel momentum to accelerate growth, but the 2026 organic growth guide for Commercial Foodservice is only 1% to 3%.

Tariffs add uncertainty, with the company estimating the full-year 2025 impact at around $21 million and management flagging a potential annual headwind of $150 to $200 million at current rates. CFO Bryan Mittelman acknowledged “margin dilution in the first half of the year” despite pricing actions already implemented. A $0.34 per-share interest expense headwind from convertible note maturities compounds the pressure in 2026.

Capital Returns as a Signal

Middleby deployed $710 million in share repurchases in 2025, significantly reducing its share count, and has continued to buy back shares in 2026. FitzGerald has been explicit: “This reflects our conviction that Middleby shares remain significantly undervalued relative to our earnings power and growth prospects.” The average 2025 repurchase price was $144.50 per share, not far from its current price of $135.81, suggesting management viewed current levels as attractive even before the restructuring fully played out.

The restructuring logic is sound on paper: two focused pure-play businesses, cleaner capital structures, and a management team freed from three distinct end markets. Whether that clarity translates into multiple expansions depends on whether QSR customers return, tariff headwinds recede, and the Food Processing spin-off commands an independent premium. Investors will get more details at the May 12 Investor Day in New York.

Data Sources

- Middleby Q4 2025 earnings call transcript and segment financials via Alpha Vantage and Fuse API

- MIDD price performance data (1-month, YTD, 1-year, 5-year) via Fuse API price-performance endpoint

- Analyst price target and sentiment data from Alpha Vantage News Sentiment (Wolfe Research, Canaccord Genuity, Baird)

- Middleby Q4 2025 SEC 8-K Filing for reported financial metrics and guidance figures