Valero Energy (NYSE:VLO | VLO Price Prediction) has been one of the energy sector’s standout performers and the Street’s consensus price target sits at just $214.22, but Raymond James is making a far bolder call.

Raymond James raised its price target on Valero to $290 from $215, maintaining a Strong Buy rating. With the stock trading near $241.75, that target sits well above the current trading price and sits well above analyst consensus. But can VLO realistically reach $290 by end of 2026? Raymond James

Raymond James’s $290 VLO Prediction

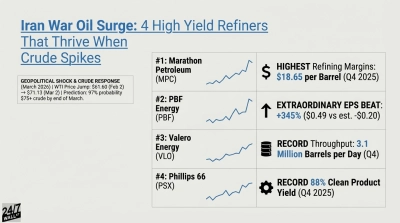

Raymond James acknowledges that consensus estimates for Q1 may have risen sharply due to oil market and Middle East conflict-driven margin spikes, but short-term refiners may struggle to fully capture these “spiky” margins. The conviction is in what comes next: forward strip margins suggest considerably higher earnings potential, with medium-term upside likely to dominate market focus as elevated refining margins persist well after the conflict subsides. That structural thesis is grounded in real operational data. Valero posted Q4 2025 EPS of $3.82, beating estimates of $3.27, while Q3 2025 refining margins reached $13.14 per barrel versus $9.09 a year earlier.

Key Drivers of VLO Stock Performance

- Structural sour crude advantage: Valero’s Gulf Coast coker infrastructure gives it a durable edge processing discounted heavy crude. Management noted on the Q4 earnings call that Venezuelan crude processing capability is now “substantially north” of the historical 240,000 barrels per day following the 2023 Port Arthur coker expansion, creating a lasting feedstock cost advantage that compounds returns through the cycle.

- Record operational efficiency: CEO Lane Riggs called 2025 “our best year for mechanical availability, personnel safety, and environmental performance,” with record throughput of 3.1 million barrels per day at 98% capacity utilization. That reliability directly converts to cash flow.

- Shareholder returns with dividend growth: Valero raised its quarterly dividend 6% to $1.20 per share in January 2026, extending 38 consecutive years of dividend payments. With FY2025 operating cash flow of $5.826 billion and a commitment to return a minimum of 40-50% of adjusted operating cash flow to shareholders through the cycle, the income stream is well-supported.

What Will It Take for VLO to Reach $290?

At a $290 target and 298.95 million shares outstanding, Valero would carry a substantially higher market cap, approaching roughly $86.7 billion, compared to its current $72.27 billion $72.29 billion. Getting there requires three things: refining margins holding at elevated levels into Q2 and beyond as Raymond James projects; continued execution on the $230 million St. Charles FCC unit optimization project expected online in H2 2026; and the market re-rating the stock as investors recognize the margin cycle has structural, not purely geopolitical, underpinnings.

The primary risk is a faster-than-expected normalization of refining margins if geopolitical tensions ease sharply and global refinery utilization rebounds simultaneously. Raymond James’s conviction rests on the forward strip, not the current spike, making $290 a target grounded in where earnings are heading rather than where they are today. That target implies roughly 20% additional upside and sits well above analyst consensus.

Contact [email protected] for any questions or corrections.