Marathon Petroleum Corp. (NYSE:MPC | MPC Price Prediction) has been a standout energy sector performer, with shares up nearly 25% over the past month and nearly 48% year to date. The stock is trading around $244 on March 25, not far off its 52-week high of $247.14.

The Street’s average price target sits at $212.83 across 10 buy and 9 hold ratings analysts. Raymond James just raised its target to $270 from $210, maintaining an Outperform rating and implying upside from current levels. That target sits well above consensus. Can MPC realistically reach $270 by end of 2026?

Raymond James’s $270 MPC Prediction

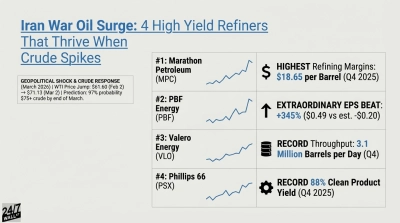

Raymond James notes that consensus estimates for Q1 may have risen sharply due to oil market and Middle East conflict-driven margin spikes, with near-term capture of these “spiky” margins presenting timing challenges. The conviction sits further out: forward strip margins suggest considerably higher earnings potential in Q2 and beyond, with medium-term upside likely to dominate market focus as elevated refining margins persist well after the conflict subsides. That thesis is grounded in real operational momentum. Marathon’s refining and marketing segment delivered adjusted EBITDA of $2.00 billion in Q4 2025, up from $559 million in Q4 2024, with margins expanding to $18.65 per barrel from $12.93 a year earlier.

Key Drivers of MPC Stock Performance

- Geopolitical tailwinds sustaining refining margins: WTI crude has surged to $93.39 per barrel, sitting at the 98.4th percentile of its 12-month range. Supply disruptions tied to Middle East conflict have compressed refined product availability globally, widening crack spreads that flow into Marathon’s per-barrel earnings. Sustained margin expansion translates directly into free cash flow funding buybacks and dividends.

- MPLX midstream distributions as a compounding engine: Marathon’s midstream subsidiary is expected to deliver more than $2.8 billion in annualized distributions to MPC in 2026, enough to cover the company’s dividend and standalone capital spending, providing a stable cash flow base independent of refining cycle volatility.

- Shareholder return program with remaining firepower: Marathon returned $4.50 billion to shareholders in full-year 2025 and entered 2026 with $4.4 billion remaining in its share repurchase authorization. Continued buybacks reduce share count, lifting per-share earnings over time.

What Will It Take for MPC to Reach $270?

With 294.5 million shares outstanding, a $270 price would imply a market capitalization above current levels, with the current market cap at $79.5 billion. Three conditions matter most: refining margins holding above historical averages through mid-2026 as geopolitical tensions persist; Marathon executing its capital return program at pace; and MPLX growth projects including the Blackcomb Pipeline and Harmon Creek III coming online on schedule to support distribution growth.

The primary risk is a rapid Middle East de-escalation that collapses crude prices and compresses crack spreads before the market can reprice Marathon’s earnings power. With a forward P/E of 13x, a structurally growing midstream segment, and a buyback program with significant runway, Raymond James’s $270 target reflects a credible path for long-term investors willing to hold through near-term volatility.

Contact [email protected] for any questions or corrections.