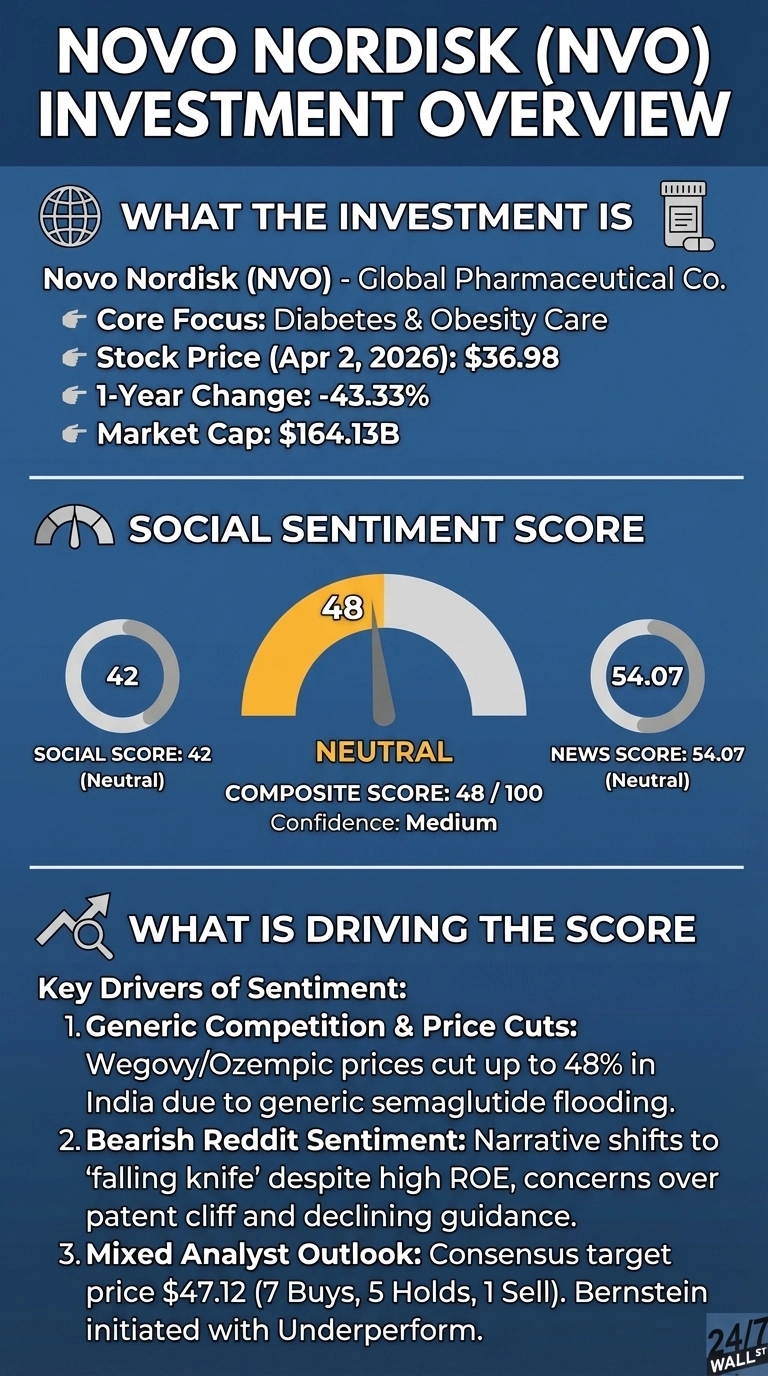

One of the world’s leading healthcare names, Novo Nordisk (NYSE:NVO) cut prices on Wegovy and Ozempic by up to 48% in India at the start of April 2026, a direct response to low-cost generic semaglutide flooding the market. A debate has been building on Reddit for weeks: is Novo Nordisk a deeply undervalued pharmaceutical franchise being temporarily disrupted, or a value trap with structurally deteriorating pricing power? Shares are trading at around $36.98, down 43% over the past year and near their 52-week low of $35.12.

The price cuts land at a complicated moment. On March 19, Novo Nordisk received FDA approval for Wegovy HD under a National Priority Voucher in just 54 days, with the higher-dose injectable achieving an average weight loss of 20.7% over 72 weeks. On March 26, the FDA approved Awiqli, the first once-weekly basal insulin for adults with type 2 diabetes. The oral Wegovy pill, launched January 5, was already generating roughly 50,000 weekly prescriptions by late January. The pipeline is active. The financials are under pressure.

Sentiment Collapse: From Bullish Bets to Bearish Caution

Reddit sentiment on Novo Nordisk traced a sharp arc over four weeks. In early March, the dominant r/wallstreetbets thread “380k NVO yolo,” drew over 150 upvotes, pushing sentiment as high as 88.

380k NVO yolo

by in r/wallstreetbets

By March 20, a post on r/stocks titled “Everyone is panic selling NVO while the WHO is literally begging for more supply” generated the highest engagement in the dataset: 100 upvotes and 25 comments, pushing sentiment to 82. That bullish spike collapsed within 48 hours.

Everyone is panic selling NVO while the WHO is literally begging for more supply

by in r/stocks

By April 1 and 2, r/investing had taken over, with the dominant post asking “Is Novo Nordisk the new ‘Intel’? (When high ROE meets a falling knife).”

Is Novo Nordisk the new ‘Intel’? (When high ROE meets a falling knife).

by in r/investing

Sentiment dropped to 22 to 42. The composite sentiment index now sits at 48 out of 100, rated neutral with medium confidence.

The bearish case rests on three concerns:

- Eli Lilly now holds more than 60% of the U.S. obesity drug market, with tirzepatide outpacing semaglutide on volume share.

- Novo Nordisk’s 2026 guidance calls for adjusted sales growth of -5% to -13% at constant exchange rates, reflecting the Most-Favored-Nations pricing agreement with the U.S. government and reduced Medicaid coverage for obesity.

- The semaglutide compound patent expires in certain international markets, and compounding of GLP-1s in the U.S. continues to erode realized prices despite the FDA grace period ending.

CagriSema Is the Bet Novo Nordisk Is Making to Win

CagriSema, a combination of cagrilintide and semaglutide, was submitted to the FDA for obesity, with a regulatory decision expected around the turn of 2026 and 2027. Phase 3 data from the REDEFINE 2 trial showed 14.2% weight loss in adults with type 2 diabetes, while REDEFINE 3 showed 11.97% weight loss at 40 weeks versus placebo. CEO Lars Fruergaard Jørgensen said in February: “We remain confident in our ability to drive volume growth over the coming years. Also, this year we look forward to regulatory decisions on next-generation treatments, such as… CagriSema within obesity.”

The consensus analyst target sits at $47.12, with 7 buys, 5 holds, and 1 sell. Bernstein initiated with an Underperform rating in March, warning of an “ongoing earnings downgrade cycle” with a “bare” catalyst path. The CagriSema decision is the clearest binary catalyst before Novo Nordisk’s Capital Markets Day in September 2026.