A popular Tesla (NASDAQ:TSLA | TSLA Price Prediction) alternative, Lucid Group (NASDAQ:LCID) shares are trading near their 52-week low at $8.81, down 64% over the past year and off roughly 16% year-to-date. The catalyst bringing Lucid back into Reddit’s crosshairs is a messy Q1 delivery report combined with a product recall that exposed a supply chain vulnerability.

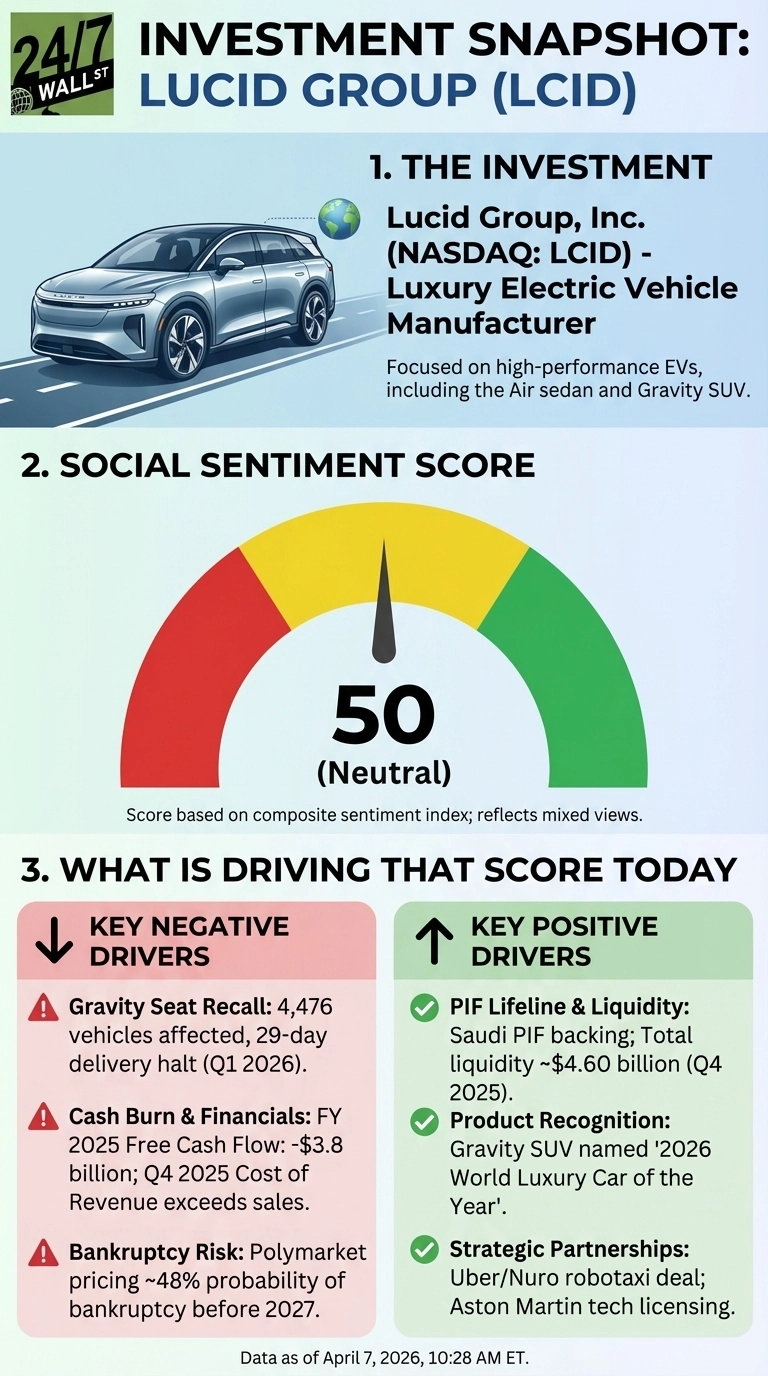

In Q1 2026, Lucid sold 3,093 vehicles, a 42% drop from the prior quarter, despite producing approximately 5,500 units. The gap traces back to a 29-day halt in Gravity deliveries caused by improperly welded seatbelt anchors in second-row seats, resulting from an unauthorized supplier change. The recall covered 4,476 Gravity SUVs produced through mid-February 2026. Management says the issue is resolved and reaffirmed full-year production guidance of 25,000 to 27,000 vehicles.

Reddit’s Weekend Surge Was About More Than a Recall

Discussion volume around Lucid spiked over the weekend of April 5 to 6, concentrated in r/wallstreetbets. The peak came Sunday, April 5, at 9 AM ET, with an activity score of 48, 309 upvotes, and 65 comments. By Tuesday morning, activity had fallen to scores of 19-21, with fewer than 10 comments per window.

The most recent classified sentiment reading, from March 17, came in at a score of 28 (bearish) from r/stocks, tied to a post titled “Watched Lucid Investor Presentation and Left with Doubt”.

Watched Lucid Investor Presentation and Left with Doubt

by u/unknown in r/stocks

Several fundamentals weigh on the stock:

- Lucid’s cost of revenue in Q4 2025 was $944.64 million, compared with revenue of $522.73 million, meaning the company lost money on every car sold at the unit level.

- Full-year 2025 free cash flow was negative $3.8 billion, and financing inflows fell roughly 75% year-over-year to $887 million as PIF’s capital injections slowed.

- Prediction market traders on Polymarket currently price a 48% probability of Lucid announcing bankruptcy before the end of 2026, the highest among comparable EV peers.

The PIF’s $10 Billion Bet Faces a Shrinking Runway

Saudi Arabia’s Public Investment Fund remains Lucid’s primary financial lifeline, having expanded its term loan facility to $2.0 billion in late 2025. While pro forma liquidity reached $5.5 billion, total liquidity fell to approximately $4.60 billion by Q4 2025 as cash and equivalents were depleted by a $3.8 billion annual burn rate. PIF’s commitment is tied to Lucid’s Saudi production goals, with full vehicle assembly at the Saudi plant targeted for year-end 2026. Despite financial stress, Lucid won the 2026 World Luxury Car of the Year award for the Gravity, and Citigroup maintains a bullish $17 price target, citing the vehicle’s massive addressable market.

The Q1 earnings call is scheduled for May 5, 2026. That call will test whether management’s credibility holds after the recall period overlapped with CEO commentary praising Gravity’s market performance. Some optimistic analysts model revenue near $9.2 billion and positive earnings by 2028, while more conservative projections put the path to profitability much later in the decade. For now, Lucid remains a high-stakes bet for those willing to ignore the 4% and 5% steady-income shift currently dominating the broader market.