Marathon Petroleum (NYSE: MPC) and Valero Energy (NYSE: VLO) have both staged remarkable recoveries. Marathon is up 95.7% over the past year, and Valero has surged 127.8% over the same period. If you watched from the sidelines, it stings. But the more important question is what comes next.

Valuation: Stretched or Still Reasonable?

Marathon trades at a forward P/E of 7x, which is deeply discounted for a company generating this kind of cash. Its PEG ratio is currently 0.934, below the 1.0 that signals the market is not pricing in the earnings growth already on the books. The consensus analyst target is $232.67, nearly in line with the current price of $231.98, meaning Wall Street sees limited near-term upside at current levels. Marathon’s trailing P/E of 18x looks more reasonable when you note that full-year 2025 adjusted EPS came in at $10.70, beating the $9.42 consensus estimate.

Valero’s picture is more nuanced. Its forward P/E of 14x is higher than Marathon’s, and its trailing P/E of 33x reflects the $1.1 billion impairment charge tied to its California refinery closures distorting GAAP earnings. Strip that out and the earnings story looks far better: full-year 2025 adjusted EPS was $10.61. The analyst price target of $234.56 is below Valero’s current price of $239.64, suggesting that the rally has already lapped consensus.

Forward Catalysts: Is There More Fuel in the Tank?

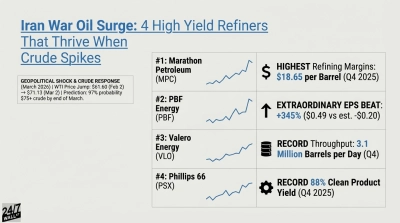

The macro backdrop is arguably the strongest catalyst of all. Benchmark West Texas Intermediate (WTI) crude has surged to $114.01 per barrel as of April 6, 2026, up from $74.58 on March 4. This is a move that typically widens crack spreads and boosts refiner margins. Marathon’s Q4 2025 R&M margin already hit $18.65 per barrel, compared to $12.93 per barrel in Q4 2024. If oil prices hold, Q1 2026 margins could be even stronger.

Beyond oil prices, both companies have concrete project catalysts. Marathon’s El Paso yield improvement is expected in Q2 2026, and the Blackcomb Pipeline (a 2.5 Bcf/d Permian-to-Gulf Coast natural gas line) is targeted for Q4 2026. Marathon also retains a $4.4 billion share repurchase authorization, which provides a floor under the stock. Look for Valero’s St. Charles FCC unit optimization, a $230 million project designed to enhance high-value product yields, to come online in the second half of 2026. Valero also raised its quarterly dividend 6% to $1.20 per share in January 2026, signaling management confidence.

Risk and Entry: What Does Downside Look Like?

The primary risk for both names is the same one that drove the rally: crack spreads. WTI at $114.01 is at the 99.6th percentile of observations over the past 12 months, with a 12-month average of just $66.18. A reversion toward that average would compress margins sharply. Both stocks also pulled back on the most recent trading day (Marathon fell 5.5% and Valero dropped 4.7%) a reminder that volatility runs both ways. Tariff risks on crude imports and California’s regulatory environment add further uncertainty, particularly for Valero’s remaining West Coast assets, which posted a $199 million operating loss in Q4.

Verdict

For retirement-focused investors, Marathon is the more defensible entry at current prices. Its forward multiple remains genuinely cheap, its buyback program is substantial, and MPLX distributions are structured to cover its dividend and standalone capital spending. Valero has already run past its analyst consensus target and carries more valuation risk if crack spreads normalize. The run is real, but for Marathon specifically, the forward earnings picture still justifies the price at current levels, while Valero’s valuation risk increases if crack spreads normalize toward the 12-month average.