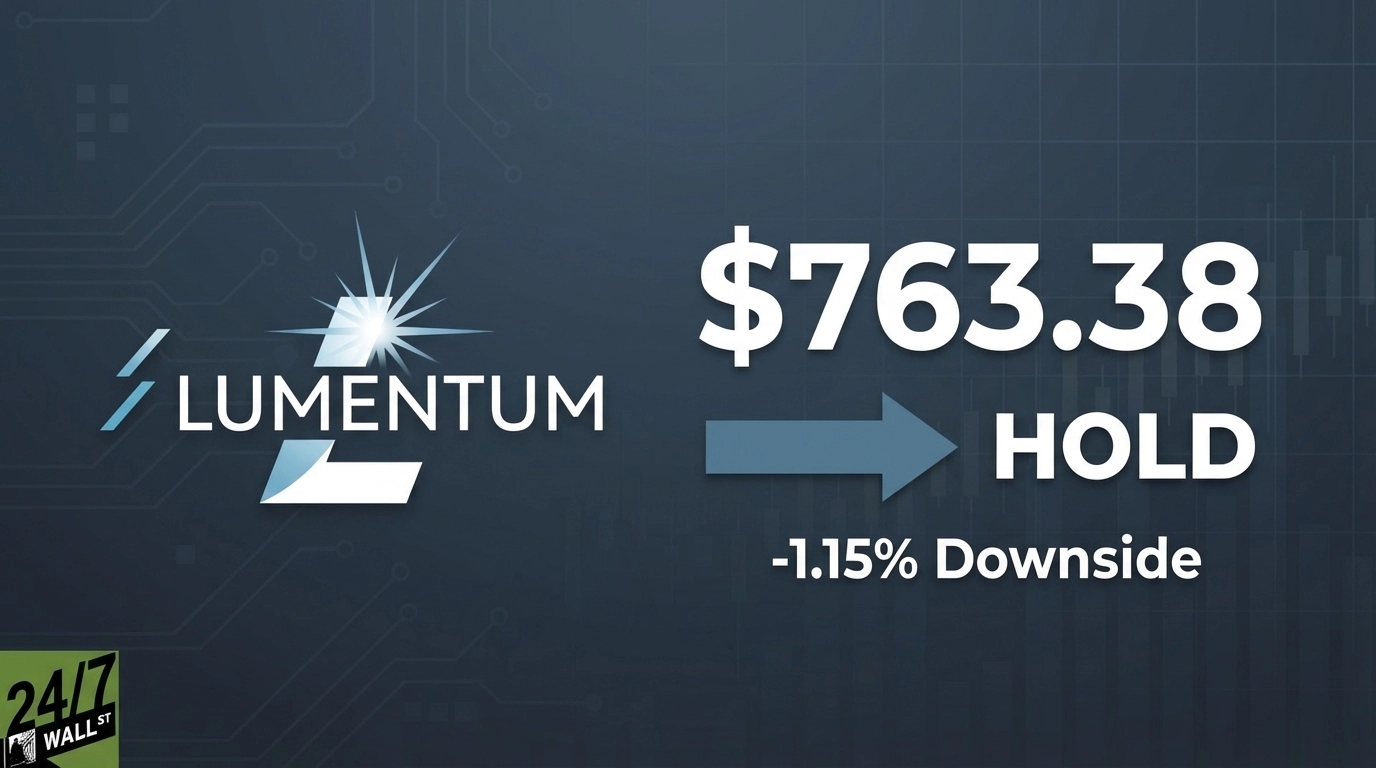

Lumentum Holdings (NASDAQ:LITE) sits at a critical inflection point. Our 24/7 Wall St. Price Target is $763.38, implying modest downside of -1.15% from the current price of $772.28. Our recommendation is HOLD, with a confidence level of 90%.

| Metric | Value |

|---|---|

| Current Price | $772.28 |

| 24/7 Wall St. Price Target | $763.38 |

| Upside/Downside | -1.15% |

| Recommendation | HOLD |

| Confidence Level | 90% |

With the stock trading above our target, the market has already priced in much of the near-term upside. Lumentum’s OCS and CPO pipelines could prove our model conservative, and we outline that bull case below.

A Year That Redefined the Stock

Lumentum has risen 1,458.27% over the past year, climbing from $49.56 to $772.28. Year-to-date, the stock is up 109.52%, and gained 17.94% in the past week. It sits 15% below its 52-week high of $836.91, after pulling back 6.6% on April 6. Q2 FY26 revenue of $665.5 million exceeding estimates by 2.06%, and non-GAAP EPS of $1.67 exceeding consensus by 18.57%. Non-GAAP operating margin expanded 1,730 basis points year-over-year to 25.2%. Catalysts including S&P 500 index inclusion in March 2026 and a $2 billion Nvidia strategic investment with multi-billion-dollar purchase commitments accelerated institutional attention.

Inside the 24/7 Wall St. Price Target

The target is built on a weighted blend of trailing P/E, forward P/E, and analyst consensus, adjusted by our proprietary 247Factor.

| Component | Value | Weight |

|---|---|---|

| Trailing P/E-Based Price | $772.28 | N/A |

| Forward P/E-Based Price | $545.71 | N/A |

| Analyst Consensus Target | $708.57 | 30% |

| Weighted Base Price | $639.88 | N/A |

| 247Factor Component | Adjustment |

|---|---|

| Base Growth | 1.05 |

| Sector Momentum (Technology) | 1.15x multiplier |

| Analyst Consensus (82% bullish) | +0.049 |

| Earnings Growth (71.1% YoY) | +0.03 |

| Volatility (Beta 1.39) | -0.008 |

| Large-Cap Dampening | 0.7x dampener |

| Total 247Factor | 1.193 |

The 247Factor of 1.193 lifts the weighted base price of $639.88 to the final target of $763.38. The large-cap dampening reflects that at a $55.14 billion market cap, sustaining hypergrowth multiples becomes harder. The trailing P/E of 222x and forward P/E of 86x reflect a stock priced for continued execution.

Why Bulls See a Path to $1,000 and Beyond

CEO Michael Hurlston stated: “Our forward guidance calls for over 85% year-over-year revenue growth, yet we are only at the starting line for two substantial opportunities: optical circuit switches (OCS) and co-packaged optics (CPO).” OCS backlog already exceeds $400 million, and Lumentum received a multi-hundred-million-dollar CPO order deliverable in H1 2027. Q3 FY26 guidance calls for revenue of $780 million to $830 million with non-GAAP operating margin of 30.0% to 31.0%. BNP Paribas set a price target of $1,040. The Nvidia partnership, a 240,000-square-foot facility in Greensboro, North Carolina producing indium phosphide optical devices, and indium phosphide capacity sold out through 2027 all support the bull scenario price of $892.02.

Risks Worth Watching

Lumentum carries $3.24 billion in current long-term debt, a meaningful overhang against $657.7 million in cash. Insider net selling of 65,775 shares worth approximately $38.85 million in Q4 2025 is worth monitoring. The weekly RSI of 72.6 sits in overbought territory, and RSI readings above 88 in late February 2026 indicate the momentum run has already been extreme. Geopolitical exposure, including trade restrictions and export controls, adds further uncertainty. The bear case lands at $547.56. The margin expansion trajectory and Nvidia partnership provide structural offsets to these risks.

What Retail Investors Are Saying

| Metric | Value |

|---|---|

| Activity Score | 12 |

| Total Mentions | 1 |

| Sentiment Score | Not available |

Reddit activity is minimal, with a single mention recorded on r/stocks. This is an institutional story, not a retail momentum trade, which lends credibility to the fundamental thesis.

Valuation at Current Levels

At our price target of $763.38, Lumentum is essentially at fair value. The recommendation is HOLD at a 90% confidence level. A pullback toward the $650-$700 range would place the stock at a more digestible forward P/E with OCS and CPO catalysts intact. Watch Q3 FY26 earnings (due May 5, 2026) against the $780-$830 million revenue guidance and whether margin expansion holds above 30%. The Nvidia partnership and AI optical infrastructure buildout are durable, but at 222x trailing earnings, the stock demands flawless execution.

Lumentum Price Prediction 2026-2030

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $763.38 |

| 2027 | $850.00 |

| 2028 | $920.00 |

| 2029 | $990.00 |

| 2030 | $858.72 (base) / $1,155.33 (bull) |

These projections assume continued execution on the OCS and CPO roadmap and elevated AI data center demand. The Greensboro facility reaching full production capacity by mid-2028 represents a major upside inflection point that could push results toward the bull scenario.