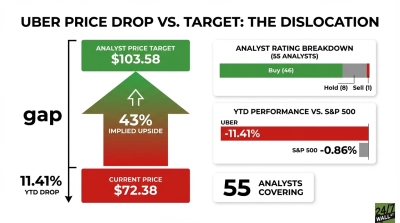

Ride hailing company Uber Technologies (NYSE:UBER | UBER Price Prediction) is trading at $72.34 as of writing, down 11.47% year-to-date and sitting well below its 52-week high of $101.99. Our 24/7 Wall St. Price Target is $125.24, implying upside of approximately 73% over the next 12 months. The 24/7 Wall St. Price Target carries a 90% confidence level.

| Metric | Value |

|---|---|

| Current Price | $72.34 |

| 24/7 Wall St. Price Target | $125.24 |

| Upside | ~73% |

| Confidence Level Basis | Proprietary 247Factor Model |

| Confidence Level | 90% |

Our price target of $125.24 clears the $100 threshold comfortably. Reaching $100 requires roughly 38% appreciation from current levels, a bar our model treats as a base-case milestone. The analyst consensus target of $103.68 corroborates that view.

Testing the YTD Pullback

Uber shares have declined 11.47% year-to-date, touching a recent low of $70.53 in February 2026 after Q4 2025 earnings disappointed on the EPS line. Non-GAAP EPS of $0.71 missed the $0.77 estimate by 8.83%, while a $1.6 billion equity investment revaluation headwind crushed reported net income to $296 million.

The operating business was accelerating beneath those headlines: free cash flow hit a record $2.8 billion in Q4, up 64.6% year-over-year, and revenue of $14.3 billion grew 20.1% year-over-year.

The Case for $125 and Beyond

The bull thesis centers on autonomous vehicles and margin expansion. CEO Dara Khosrowshahi told investors on the Q4 call: “We enter 2026 with a rapidly growing topline, significant cash flow, and a clear path to becoming the largest facilitator of AV trips in the world.” Uber currently has 20-plus autonomous vehicle partners globally and expects to operate in 15 cities by year-end. A deal to invest up to $1.25 billion in Rivian (NASDAQ: RIVN) to launch 50,000 robotaxis has already lifted retail investor sentiment.

The core business is accelerating. Delivery revenue grew 30% year-over-year in Q4 2025 with adjusted EBITDA up 40%. Full-year 2025 free cash flow reached $9.7 billion, up 41.6%. Uber repurchased $6.5 billion of shares in full-year 2025 under a $20 billion authorization.

Of 56 analysts covering the stock, 47 rate it Buy or Strong Buy, just 1 rates it a Sell, with the bull case pointing to $138.55.

What Could Go Wrong

Worker classification regulation remains an unresolved overhang globally, and insurance reserves grew from $2.7 billion to $3.3 billion year-over-year, a cost pressure management says is easing but has not fully resolved. Long-term debt rose from $8.3 billion to $10.5 billion, partly funding AV infrastructure. The Freight segment remains at flat growth and near-breakeven profitability.

Full-year 2025 GAAP EPS of $2.45 missed the $5.37 estimate by a wide margin, though that gap is almost entirely explained by non-cash equity revaluations. The bear scenario prices the stock at $104.04, still above $100, suggesting limited downside to the key threshold even in a pessimistic scenario.

Key Catalysts and Risks to Watch

The Q1 2026 guidance midpoint calls for 37% year-over-year EPS growth, a meaningful catalyst if delivered. Our price target carries a 90% confidence level. The case strengthens if Q1 2026 results confirm EPS growth and AV city deployments stay on schedule; it weakens if insurance costs re-accelerate or the Rivian deal faces regulatory delay.

Uber Price Prediction 2026-2030

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $110.14 |

| 2027 | $125.24 |

| 2028 | $165.00 |

| 2029 | $220.00 |

| 2030 | $322.47 |

Intermediate years assume continued 18-20% revenue growth, expanding EBITDA margins, and meaningful AV monetization beginning in 2028. The 2030 figure reflects the 5-year base case, implying a 34.84% annualized return. Significant upside or downside could result from the pace of autonomous vehicle commercialization and any resolution of global worker classification regulations.

Contact [email protected] for any questions or corrections.