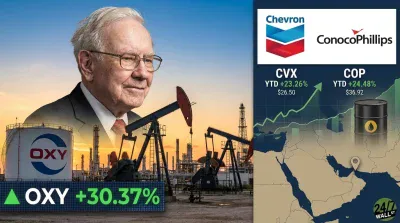

Chevron (NYSE:CVX | CVX Price Prediction) and ConocoPhillips (NYSE:COP) closed 2025 with results that expose a fundamental divide in how two oil giants handle commodity downturns. One relies on a diversified, integrated model. The other bets on pure-play discipline and shale inventory. The dividend question cuts to the heart of that difference.

Integrated Buffer vs. Pure-Play Pressure

Chevron’s fourth quarter results showed what an integrated model looks like under stress. Revenue came in at $46.87B, beating estimates by 0.3%, while EPS of $1.52 beat the $1.44 estimate by 5.56%.

That outperformance came despite average Brent crude of $64/BBL versus $75/BBL a year earlier. The downstream refining segment absorbed upstream pain. U.S. refinery throughput hit its highest level in 20 years, and the Hess acquisition contributed 261 MBOED in 2025.

ConocoPhillips had a rougher Q4. EPS of $1.02 missed the $1.09 estimate by 6.42%, and net income fell 37.3% year-over-year. The core problem was pricing: average realized price dropped to $42.46/BOE, down 19% from $52.37 a year prior.

Without refining operations, every dollar of price weakness hits the income statement directly. Production grew with Q4 output reaching 2,320 MBOED, up 137 MBOED year-over-year, but volume gains could not offset the price collapse.

| Business Driver | Chevron | ConocoPhillips |

|---|---|---|

| Q4 EPS vs. Estimate | Beat +5.56% | Missed -6.42% |

| Downstream Buffer | Yes (refining, chemicals, renewable diesel) | No (pure-play E&P) |

| FY2025 Operating Cash Flow | $33.94B (record) | $19.80B |

| Dividend Coverage (FCF basis) | 2.66x | 4.20x |

39 Years of Raises vs. a Younger Streak

Chevron’s dividend story rests on longevity. The quarterly dividend rose 4% to $1.78/share, marking the 39th consecutive annual increase. The historical record validates that streak: even during the 2020 pandemic, when net income turned negative at $5.6B, operating cash flow still covered the dividend at 1.09x.

Chevron did not cut during downturns. It raised. The current dividend yield sits at 3.59%, backed by $12.75B in dividend payouts covered 2.66x by operating cash flow in 2025.

ConocoPhillips uses a different structure: a base dividend of $0.78/quarter was established in Q4 2024, with variable supplemental payments when cash flow allows. Q4 2025 and Q1 2026 each included a $0.06 supplemental component, bringing the total to $0.84/quarter.

On a free cash flow coverage basis, COP looks stronger: FCF covered dividends 4.20x in 2025. The risk is that the variable component disappears when oil softens, and the streak lacks the institutional weight of Chevron’s four-decade run.

| Dividend Lens | Chevron | ConocoPhillips |

|---|---|---|

| Quarterly Dividend | $1.78 | $0.84 |

| Consecutive Annual Increases | 39 years | Top-quartile S&P growth rate |

| Dividend Structure | Fixed quarterly raises | Base + variable supplemental |

| 2020 Stress Test Coverage | 1.09x (maintained, no cut) | 2.62x (maintained) |

Oil at $114 Changes the Math

The earnings were reported against weak crude. WTI closed 2025 near $57/BBL before staging a sharp recovery. By April 6, 2026, WTI reached $114.01/BBL, roughly double the Q4 2025 baseline. That tailwind improves dividend coverage for both companies.

Watch whether Chevron converts oil price recovery into accelerated cost reductions, given its $3-4B structural cost reduction target by end of 2026. For ConocoPhillips, the question is whether the Willow project in Alaska stays on budget. Capital estimates for Willow have risen to $8.5-9B, and further escalation would pressure free cash flow ahead.

Why Chevron Wins for Dividend Permanence

Both dividends look safe at current oil prices. But “forever” demands a different standard. Chevron’s 39-year consecutive increase streak, its integrated model that cushions commodity swings, and its unbroken dividend coverage even through the 2020 net loss year make it the more defensible choice for income investors prioritizing durability.

ConocoPhillips’ base-plus-variable structure is honest about cyclicality, and the 8% recent dividend increase is impressive. But the variable component introduces uncertainty. For a forever-hold investor, Chevron’s 39-year raise streak and institutional commitment offer greater confidence.