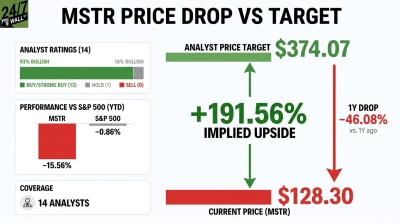

MicroStrategy (NASDAQ:MSTR) carries a consensus Hold rating and median price target of $130. The stock has shed 52% over the past year and sits 71% below its July 2025 peak of $457.22, yet analysts remain overwhelmingly bullish, creating tension worth examining before taking a position.

MicroStrategy operates two distinct businesses. The legacy enterprise analytics software generates roughly $477 million in annual revenue, with subscription services growing 62% as customers migrate to the cloud. But the software business is almost beside the point. MicroStrategy is now primarily a bitcoin treasury vehicle, holding 713,502 BTC acquired at approximately $54.26 billion. With bitcoin currently near $71,040, the company’s bitcoin position is worth meaningfully less than its cost basis, explaining much of the stock’s decline from last year’s highs.

Bitcoin at a Discount: The Case for Buying

The bull argument is straightforward. MicroStrategy’s price-to-book ratio sits at roughly 1x, meaning investors are essentially buying the bitcoin treasury at close to net asset value. The company’s shareholders’ equity stands at $44.12 billion against a market cap near $44.6 billion represents a rare entry point for a company with an unmatched accumulation machine. Prediction markets assign a 99.3% probability that MicroStrategy will hold 800,000 or more BTC by year-end, and a 97.4% probability of another bitcoin purchase in the immediate week ahead.

Wall Street agrees. 14 of 15 analysts rate the stock a Buy or Strong Buy, with a consensus price target of $367.64, implying roughly 180% upside from current levels. The 23% BTC Yield achieved in FY2025 demonstrates that the capital raise strategy is accretive on a per-share bitcoin basis. If bitcoin recovers toward prior highs, fair value accounting means those gains flow directly to the income statement.

Leveraged to a Declining Asset With Dilution Risk

Bitcoin is down nearly 15% year-to-date and around 12% over the past year. MicroStrategy’s Q4 2025 results showed a $17.44 billion unrealized loss on digital assets, producing a net loss of $12.44 billion and an EPS of -$42.93. The company carries $8.2 billion in long-term convertible debt and growing perpetual preferred obligations. Common equity sits below both in the capital structure.

Insider behavior adds caution. The CEO, CFO, and executives conducted coordinated share sales in late March at prices between $137 and $139, just above current levels. Executives have only purchased preferred stock recently, a defensive instrument offering downside protection rather than signaling conviction in common equity.

Waiting for Bitcoin to Decide

The hold case is simple. MicroStrategy’s stock price is almost entirely a function of bitcoin’s next move. With BTC down 19% year-to-date and sitting well below MicroStrategy’s cost basis, the risk-reward on common equity is unclear. The software business provides no meaningful floor given its size relative to the bitcoin position. Liquidation risk is low, with prediction markets placing only a 3.2% probability on any bitcoin sales by mid-year and a 7.5% probability of a margin call in 2026.

The Numbers

MicroStrategy currently trades at $130 against an analyst consensus target of $367.64 from 15 analysts. The 180% implied upside reflects the binary nature of a bitcoin-leveraged vehicle. The stock’s beta of 3.56 means it moves violently in both directions. MSTR is down 15% year-to-date while the S&P 500 has also faced pressure in 2026, though MSTR’s decline is substantially driven by bitcoin weakness. The 52-week range spans $104.17 to $457.22, capturing the risk profile.

Hold Until Bitcoin Shows Its Hand

The bull case requires bitcoin to recover meaningfully. The bear case requires continued BTC weakness and potential credit stress from the preferred stack. The risk-reward remains genuinely balanced today. The 1x book value entry is interesting, and the accumulation engine remains intact with over $37 billion in ATM capacity remaining. But buying common equity here means accepting subordination to $8.2 billion in debt and growing preferred obligations, with no insider conviction at current prices.

Bitcoin’s trajectory will be the key variable to monitor quarter by quarter. A sustained move above $85,000 would shift the risk-reward calculus toward bullish territory. A break below $60,000 would expose the cost basis problem and pressure preferred dividend coverage, tilting the outlook bearish. Until one of those conditions emerges, patience costs less than being wrong on direction in a stock with a beta of 3.56.