Tech giant Microsoft (NASDAQ:MSFT | MSFT Price Prediction) trades at $370.87 as of writing, down 23.14% year-to-date. Our price target is $488.47, implying roughly 31.71% upside over the next 12 months. Our recommendation is buy, with a 90% confidence level.

| Metric | Value |

|---|---|

| Current Price | $370.87 |

| 24/7 Wall St. Price Target | $488.47 |

| Upside | 31.71% |

| Recommendation | BUY |

| Confidence Level | 90% |

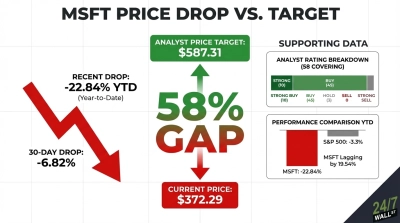

The YTD decline has created an entry point for investors who believe in the Azure AI thesis. 95% of covering analysts are bullish, with a consensus target of $587.31.

Stock Performance vs. Earnings

Microsoft’s stock peaked at $552.24 on a 52-week basis before sliding to current levels. Over the past month, shares fell 8.4%, and the one-year return stands at -2%. The stock trades below both its 50-day moving average of $393.88 and 200-day moving average of $474.17, signaling sustained selling pressure.

Yet earnings tell a different story. In Q2 FY2026, Microsoft posted non-GAAP EPS of $4.14 against a consensus estimate of $3.85, a 7.57% beat. Revenue reached $81.27 billion, up 16.72% year-over-year.

Azure grew 39% YoY, and commercial remaining performance obligation surged 110% to $625 billion. This $625 billion backlog provides multi-year revenue visibility. The next earnings report is scheduled for April 29.

The Bull Case

Azure’s growth of 39-40% YoY, with forward guidance of 37-38% growth next quarter, shows no deceleration. The $625 billion commercial RPO provides multi-year visibility. The OpenAI partnership creates structural advantage: OpenAI is contracted to purchase $250 billion of incremental Azure services, and Microsoft holds a 27% stake valued at approximately $135 billion.

CEO Satya Nadella stated: “We are only at the beginning phases of AI diffusion and already Microsoft has built an AI business that is larger than some of our biggest franchises.” If Copilot adoption accelerates across the enterprise, operating leverage could push the stock toward the analyst consensus target of $587.31. Our bull case scenario targets $601.31 within 12 months.

Risks

CapEx surged 89.04% YoY to $29.88 billion in Q2 FY2026 alone, with full-year FY25 CapEx reaching $64.55 billion. If AI monetization stalls, that spending becomes a liability.

OpenAI’s investment losses totaled $3.1 billion in Q1 FY2026, up from $523 million year-ago. The More Personal Computing segment posted -3% revenue growth, showing legacy hardware headwinds.

Operating income still grew 20.92% YoY in Q2, and operating margins remain near 47.1%, demonstrating profitability is intact. The bear case scenario targets $437.23, still representing upside from current levels.

The Bottom Line

The 24/7 Wall St. price target of $488.47 reflects a business firing on nearly every cylinder, temporarily weighed down by macro pressure and sector rotation. The forward P/E of 19x is reasonable for a company growing revenue at 16-18% annually with a $625 billion contracted backlog. Confidence sits at 90%.

Azure growth holding above 35% through the next two quarters and Copilot monetization appearing in segment margins would support the bull case. Accelerating CapEx without corresponding Azure revenue guidance increases would pressure the bear case scenario.

Microsoft Price Projection 2026-2030

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $488.47 |

| 2027 | $486.44 |

| 2028 | $589.49 |

| 2029 | $668.74 |

| 2030 | $747.58 |

These projections assume Microsoft executes on its Azure AI strategy and Copilot adoption drives enterprise revenue expansion. Significant upside or downside could result from changes in AI monetization, competitive pressure from cloud rivals, or shifts in the OpenAI partnership structure.

Contact [email protected] for any questions or corrections.