Microsoft (NASDAQ:MSFT | MSFT Price Prediction) stock is sliding approximately 2% to 3% in Tuesday trading, with shares hovering around $374. These are quiet-looking numbers on the surface, but for a company this closely watched, they carry weight.

The decline is unfolding even as Bank of America (NYSE:BAC) reinstated coverage of Microsoft shares with a Buy rating and a $500 price target this morning. That gap between a fresh institutional buy call and a stock that keeps drifting lower tells you something about where investor anxiety is right now.

The broader technology sector is adding pressure. The NASDAQ 100 is down roughly 0.6% today, and software names are getting hit harder than most. Microsoft is drawing the most scrutiny, given its size and its central role in the AI narrative.

OpenAI Dependency Moves to Center Stage

The investor debate circling Microsoft today centers on what comes next, not this quarter’s numbers. Microsoft reported $81.27 billion in revenue for Q2 FY2026, beating estimates by roughly 1.2%, with non-GAAP EPS of $4.14 against a consensus of $3.85. Those are solid results, but the concerns pertain to what comes next and whether the OpenAI relationship is an asset or a liability in disguise.

OpenAI has warned investors about the risks associated with its heavy reliance on Microsoft for financing and computing resources, flagging this as a key business risk in a document resembling an IPO prospectus. The company stated that any alteration or termination of this partnership could negatively impact its business and financial condition. We recently dove in for a deeper read on what that disclosure actually means for Microsoft’s position.

The irony is that the disclosure cuts both ways. OpenAI needs Microsoft, but Microsoft has also built its AI growth story around OpenAI. Microsoft holds approximately a 27% stake in OpenAI, valued at roughly $135 billion, and OpenAI has contracted to purchase an incremental $250 billion of Azure services. That’s a lot of eggs in one basket, and investors are starting to price in the risk that comes with it.

The Capex Question Is Not Going Away

Capital expenditures nearly doubled year-over-year to $29.9 billion in Q2 FY2026. That level of spending is what you do when you believe the AI infrastructure buildout will pay off at scale, but it also compresses near-term free cash flow and raises the stakes on execution. Investors across the sector are asking the same question right now, and Microsoft isn’t alone in fielding it.

Microsoft CEO Satya Nadella framed the opportunity confidently on the earnings call, declaring, “We are only at the beginning phases of AI diffusion and already Microsoft has built an AI business that is larger than some of our biggest franchises.” That’s a compelling vision, and the market is still weighing how long it will take to materialize while capex runs this hot.

Bulls and Bears Are Both Making a Case

The bulls have some stats on their side: Azure grew 39% year-over-year in Q2, and Microsoft guided for 37% to 38% growth next quarter. Furthermore, Microsoft’s commercial remaining performance obligation surged 110% to $625 billion, which is essentially a giant backlog of committed revenue.

The bear case, meanwhile, is about timing and dependency. Microsoft’s OpenAI investment losses hit $3.1 billion in Q1 FY2026, up from $523 million a year earlier. The company’s Q2 GAAP net income looked strong partly because of $7.6 billion in net gains from OpenAI investments, but that kind of accounting benefit does not repeat every quarter. Strip it out and the underlying picture is more complicated.

The Fundamentals Aren’t Broken

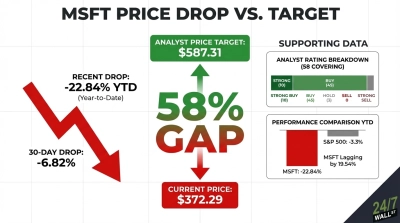

At the moment, MSFT stock is down by roughly 23% year-to-date. This means investors who bought at the highs are sitting on real losses and debating whether to hold or cut.

Prediction markets are pricing in near-certainty that Microsoft stock closes down today, with crowdsourced probability sitting at 99% for a down close. Analyst consensus tells a different story: 54 buy or strong buy ratings, zero sell ratings, and a consensus price target of around $595. That’s a wide gap between what the market is doing today and where analysts think this stock belongs.

All in all, Microsoft’s fundamentals haven’t broken. The AI infrastructure story is intact, Azure is growing fast, and the backlog is enormous.

What has changed is investor patience with the OpenAI dependency and the timeline for converting massive capital spending into earnings that do not rely on one-time investment gains. The key question is whether the OpenAI dependency and capex trajectory will weigh on Microsoft’s earnings quality in the coming quarters.

Contact [email protected] for any questions or corrections.